Download to read offline

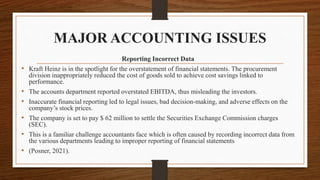

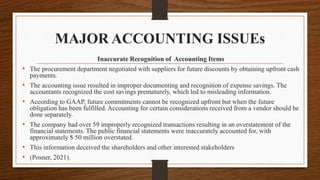

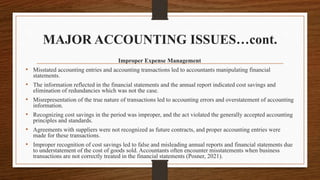

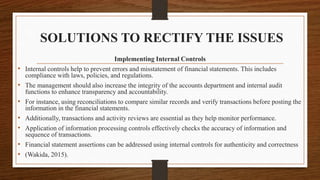

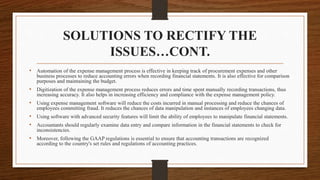

Kraft Heinz experienced major accounting issues after its merger, including reporting incorrect data from departments, improperly recognizing accounting items, and improper expense management. This led to overstated financial statements and misleading investors. To address these issues, Kraft Heinz implemented internal controls, automated expense management processes, and ensured compliance with GAAP to accurately report financial information.