Download to read offline

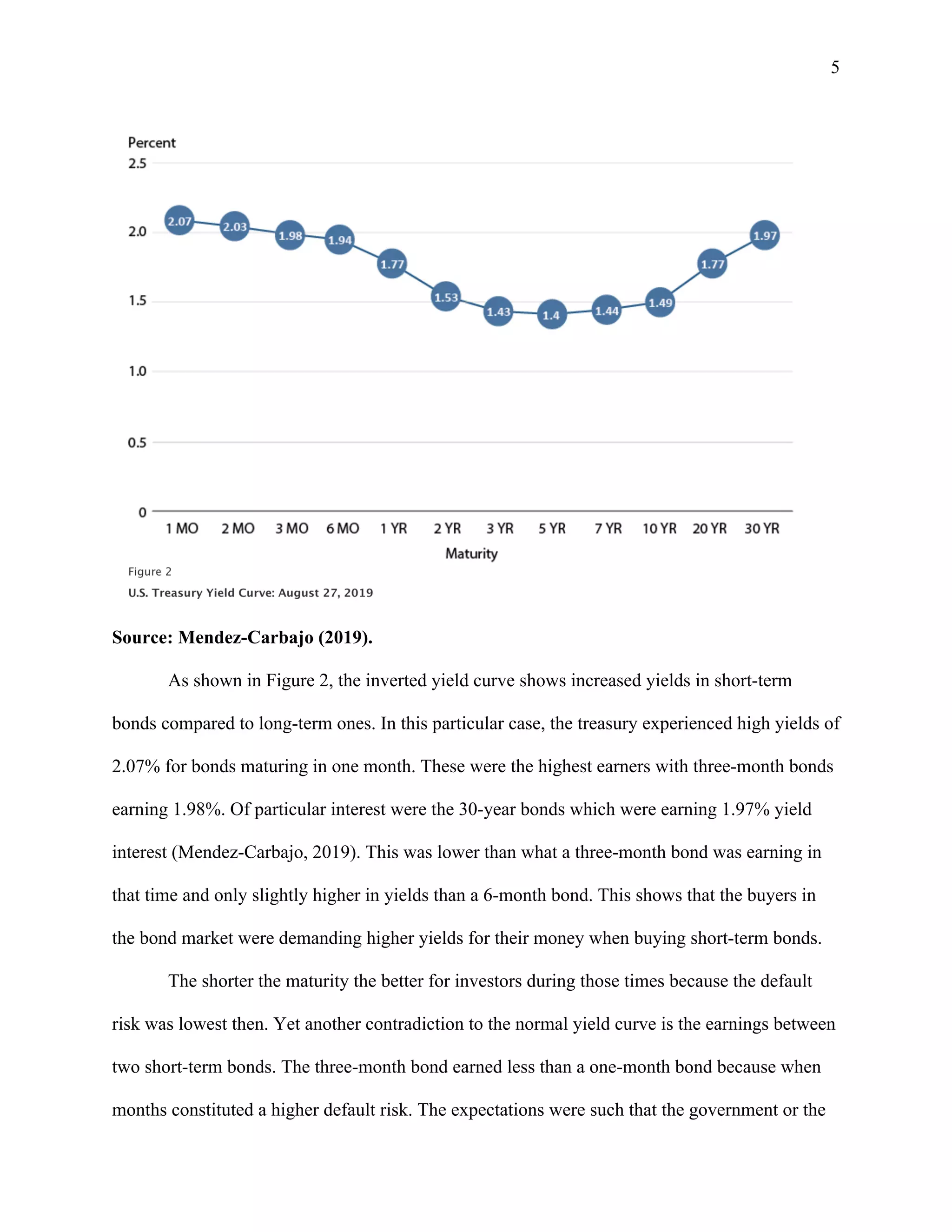

The document explains the concept of an inverted yield curve, which indicates poor economic performance and is often a precursor to recession. It describes how long-term bonds typically yield higher returns than short-term bonds due to default risk, but during an inverted yield curve, this trend reverses, leading to higher short-term yields as investors anticipate economic downturns. Various factors, including historical precedents like the 2007 housing bubble, influence these changing perceptions among investors.