The document provides information about the Kangra Central Cooperative Bank Ltd. It discusses the bank's history, leadership, financial position, functions, vision, mission, and SWOT analysis. Some key points:

- The bank was established in 1920 and has expanded to over 50 branches across 3 districts of Himachal Pradesh.

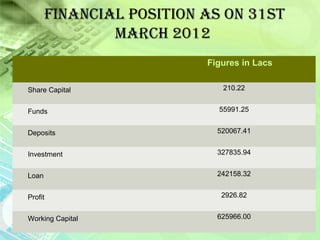

- As of 2012, the bank had over Rs. 500 crore in deposits and Rs. 300 crore in investments.

- The bank's vision is to be a top-class financial institution and its mission is sustained growth, fulfilling social obligations, and using new technologies.

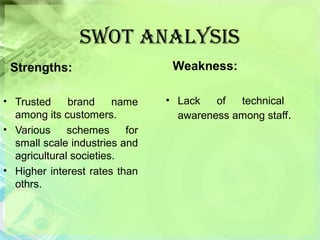

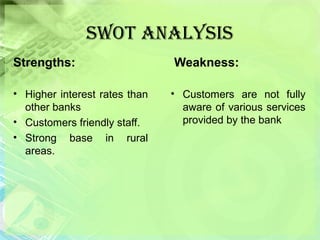

- A SWOT analysis finds strengths in trusted brand name and customer-friendly staff while weaknesses include

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)