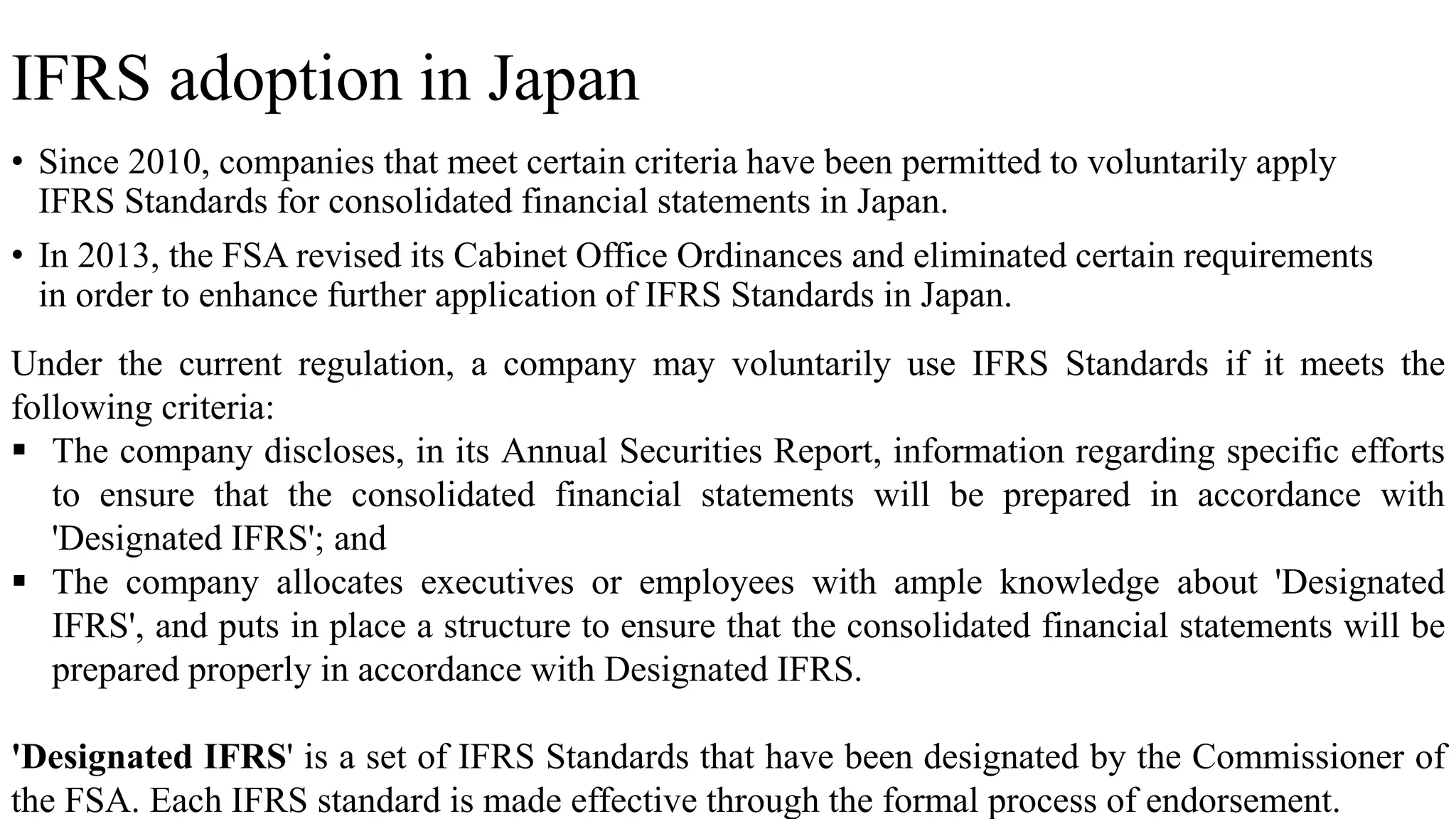

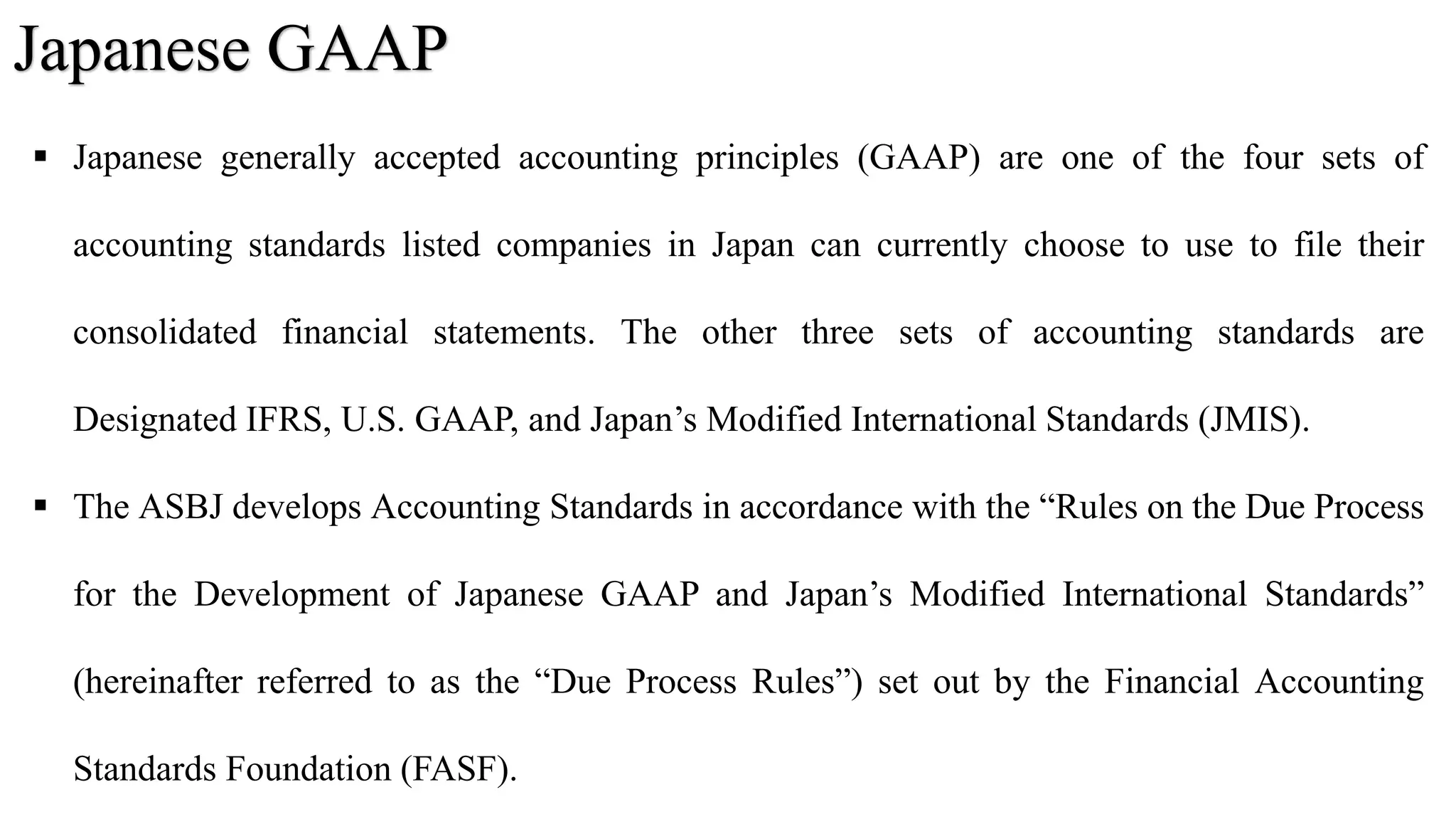

Japan, a constitutional monarchy and the third largest economy globally, has a complex framework for financial reporting governed by the Accounting Standards Board of Japan (ASBJ). Companies can choose from four accounting standards for consolidated financial statements: Japanese GAAP, designated IFRS, US GAAP, and Japan’s modified international standards (JMIS). The ASBJ develops these standards, with designated IFRS allowing voluntary adoption under specific criteria to promote international accounting practices.