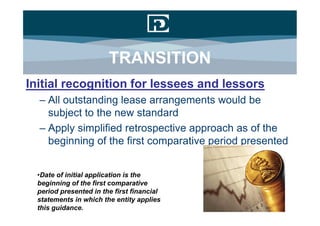

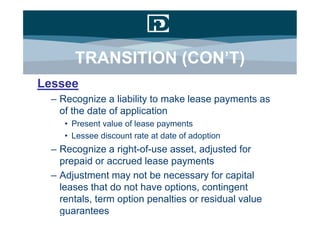

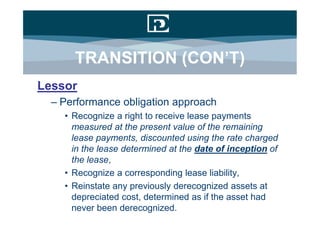

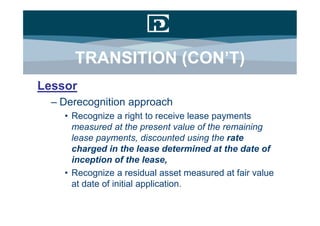

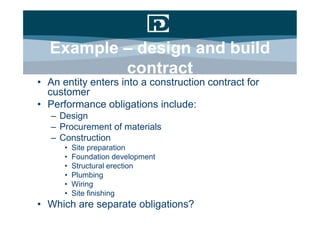

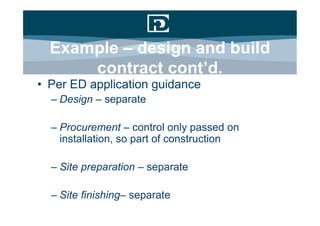

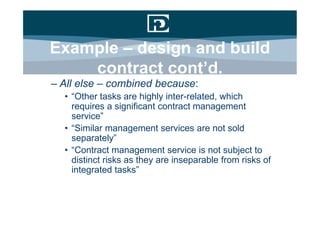

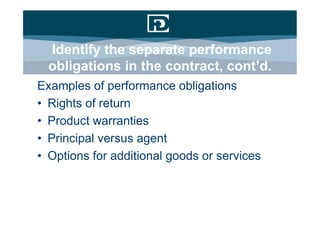

The document outlines the changes in lease accounting under a new model that aims to enhance consistency, comparability, and transparency by introducing a right-of-use model and reducing the complexity in accounting for leases. It discusses the transition to this new accounting standard, the specific accounting treatments for lessees and lessors, as well as key issues related to the adoption and implementation of convergence accounting. Additionally, it addresses the evaluation of current IT systems to align with the new requirements and emphasizes the importance of managing the transition process effectively.

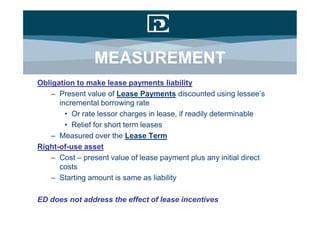

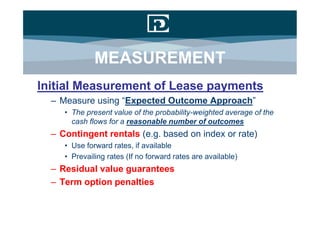

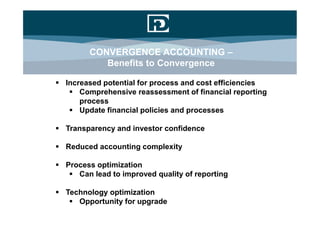

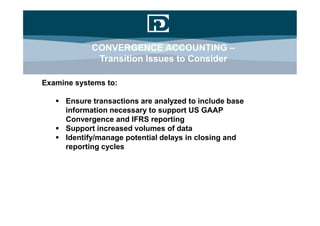

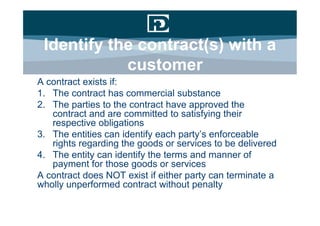

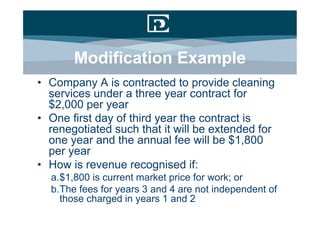

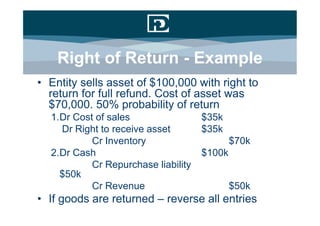

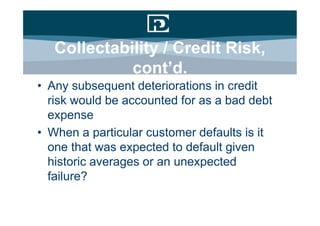

![MEASUREMENT

How do you determine present value of

payment stream (Expected Outcomes

Approach)?

1. Develop reasonably possible outcomes over

the [calculated] life of the lease

2. Estimate amount and timing of cash flows for

each outcome

3. Calculate the present value of the cash flows

4. Probability-weigh each outcome](https://image.slidesharecdn.com/january2011aaupdateboaconfcenter-110209190650-phpapp01/85/January-2011-A-A-update-from-Frazier-Deeter-LLC-16-320.jpg)

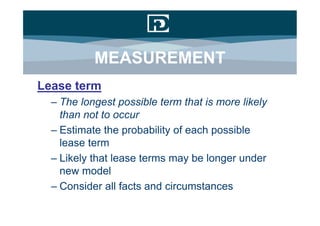

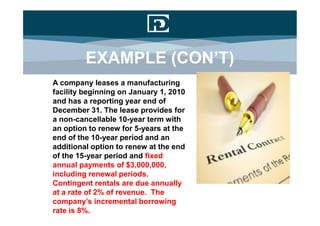

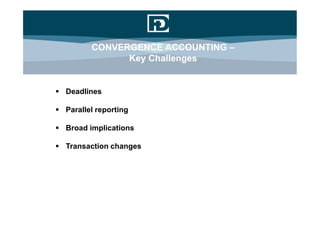

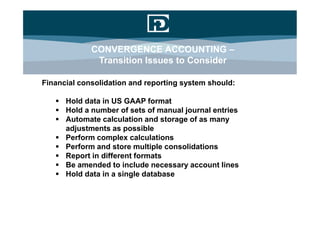

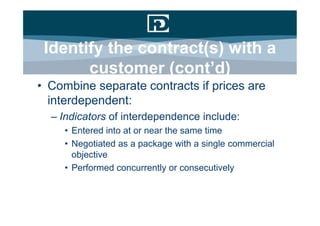

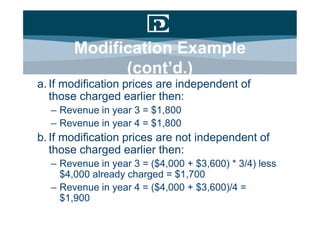

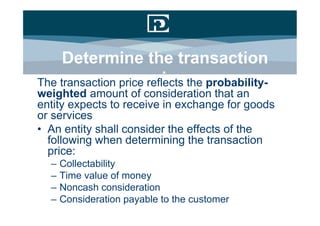

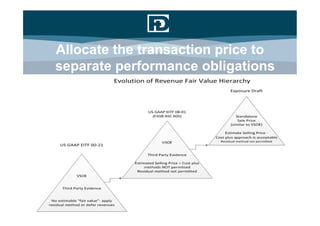

![MEASUREMENT

Subsequent measurement and reassessment

– Reassessment

• If facts or circumstances indicate that there would be a

significant change in the liability since the previous

reporting period

– Remeasurement

• Change in lease term would provide for a

corresponding adjustment to the right-of-use asset

• Changes in estimated payment stream

– Recognized in income to extent [adjustment] changes

related to prior or current periods

– Adjust right-of-use asset for [adjustment] changes related

to future periods](https://image.slidesharecdn.com/january2011aaupdateboaconfcenter-110209190650-phpapp01/85/January-2011-A-A-update-from-Frazier-Deeter-LLC-21-320.jpg)

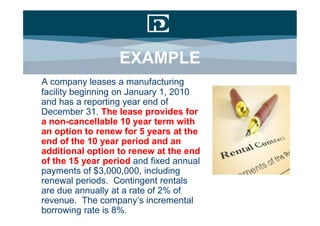

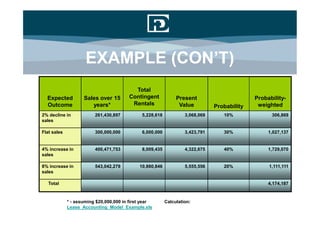

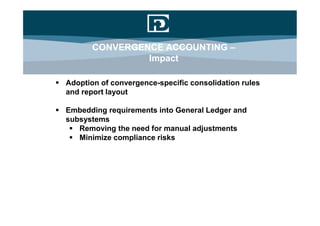

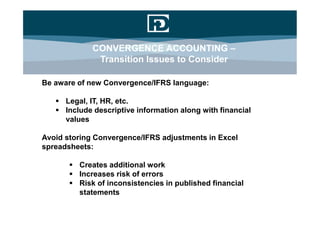

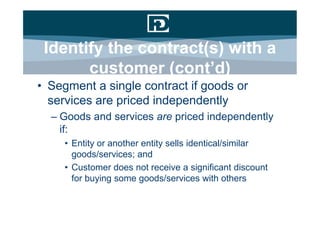

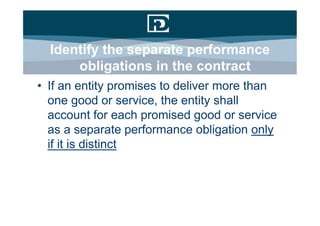

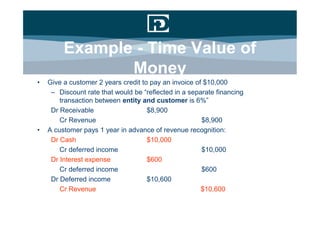

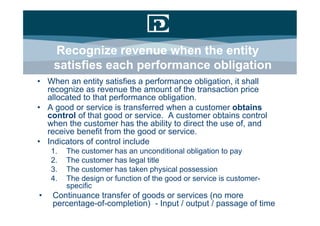

![PERFORMANCE OBLIGATION

Recognition

– Performance

obligation liability

• permit the lessee to

use the asset

• Measure at rate

charged by lessor

– Asset [receivable]

• the right to receive

lease payments](https://image.slidesharecdn.com/january2011aaupdateboaconfcenter-110209190650-phpapp01/85/January-2011-A-A-update-from-Frazier-Deeter-LLC-24-320.jpg)

![[Podcast] Time to prepare... for lease accounting changes](https://cdn.slidesharecdn.com/ss_thumbnails/leaseaccountingchangeswebinar1-130610170134-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)