Download to read offline

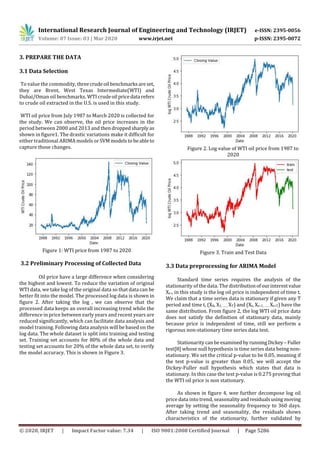

1) The document examines using an ARIMA model to forecast crude oil prices based on WTI crude oil price data from 1987 to 2020. 2) It finds the WTI oil price data is non-stationary and takes the log of the prices and removes trends and seasonality to make the data stationary. 3) It then identifies the best fitting ARIMA model as ARIMA(0,1,4) and applies it to forecast future oil prices, finding a mean squared error of 1.606 on test data.