Downloaded 1,065 times

![Thank You [email_address]](https://image.slidesharecdn.com/ipmproject-090225092844-phpapp01/75/IP-Valuation-48-2048.jpg)

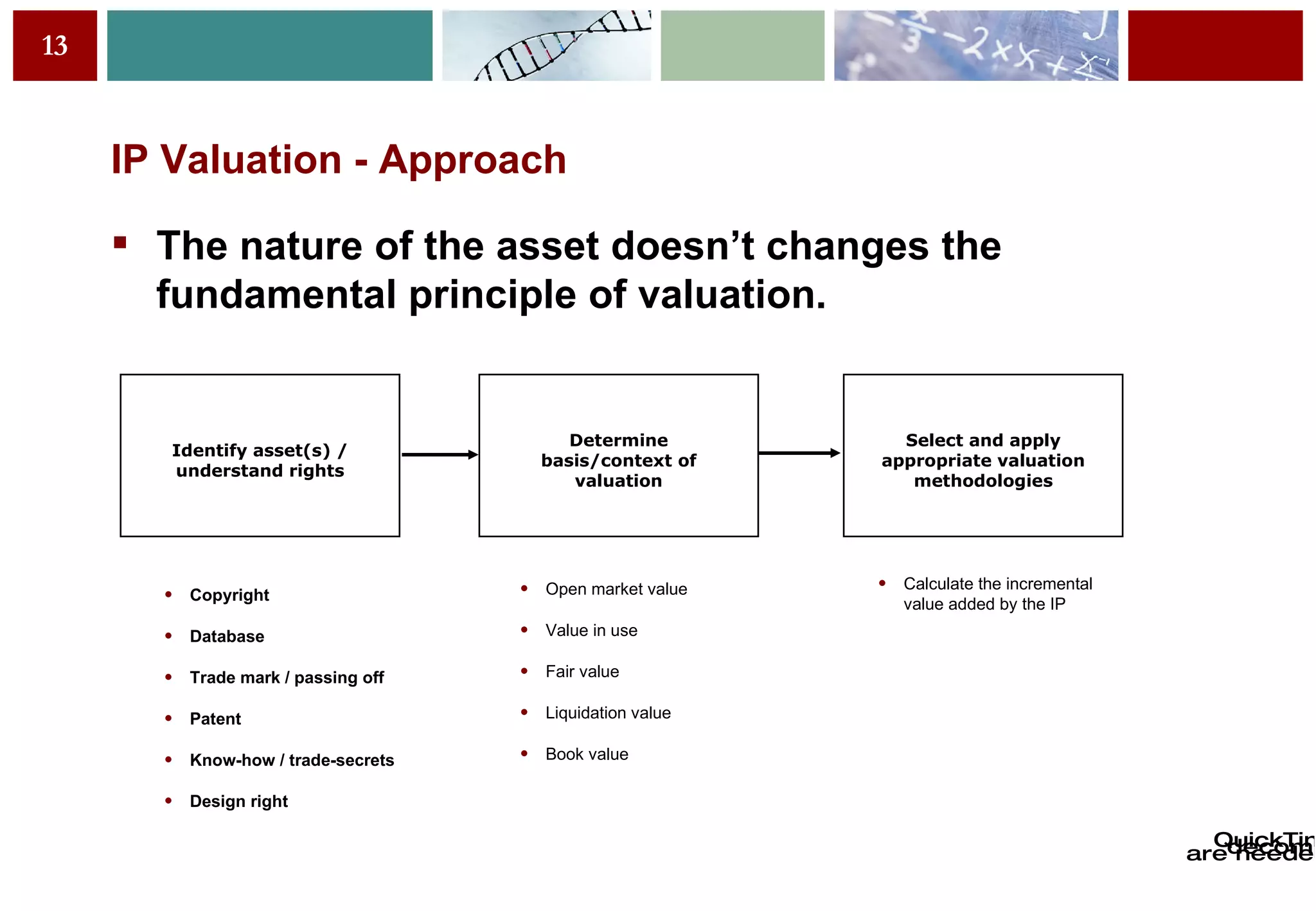

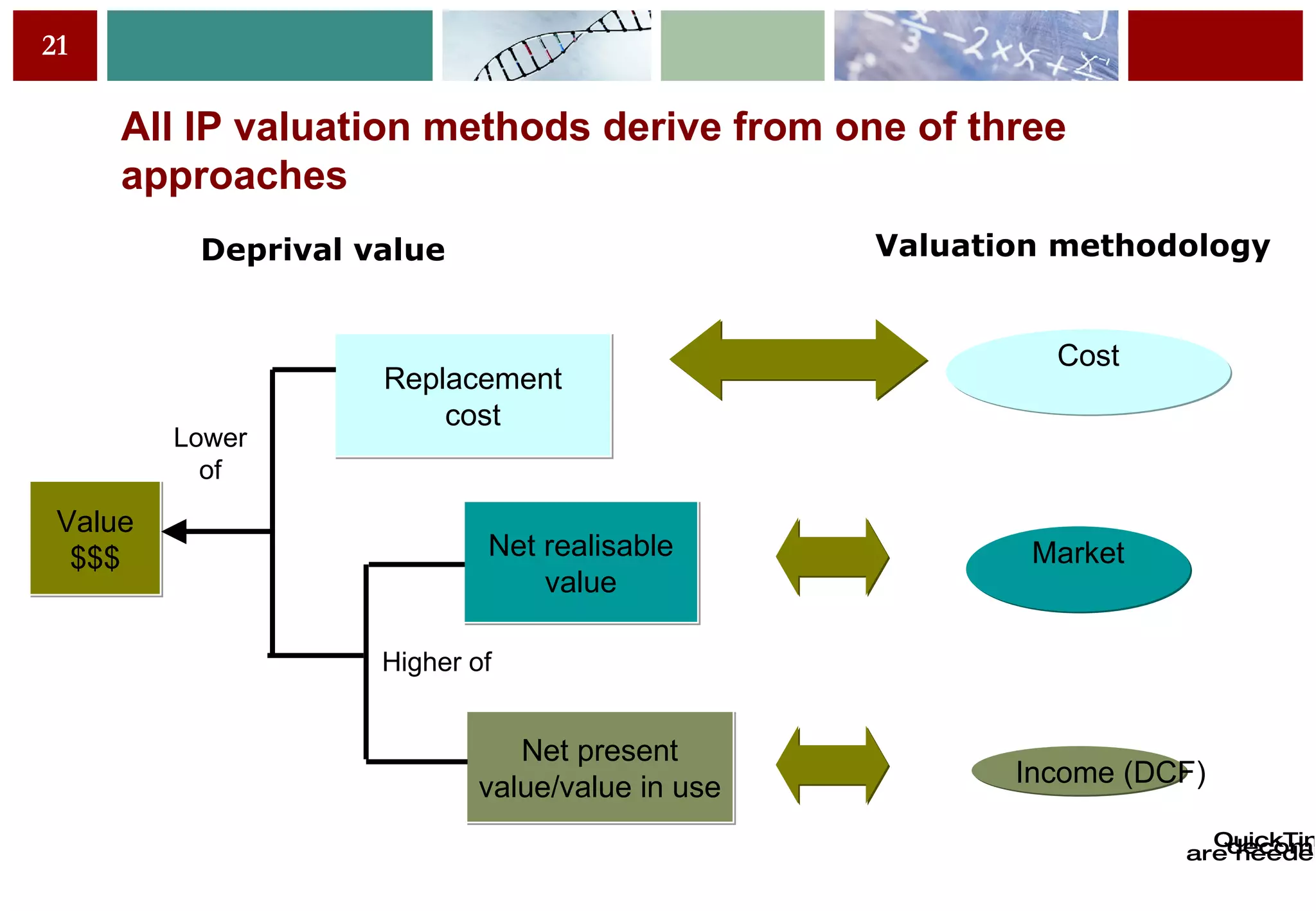

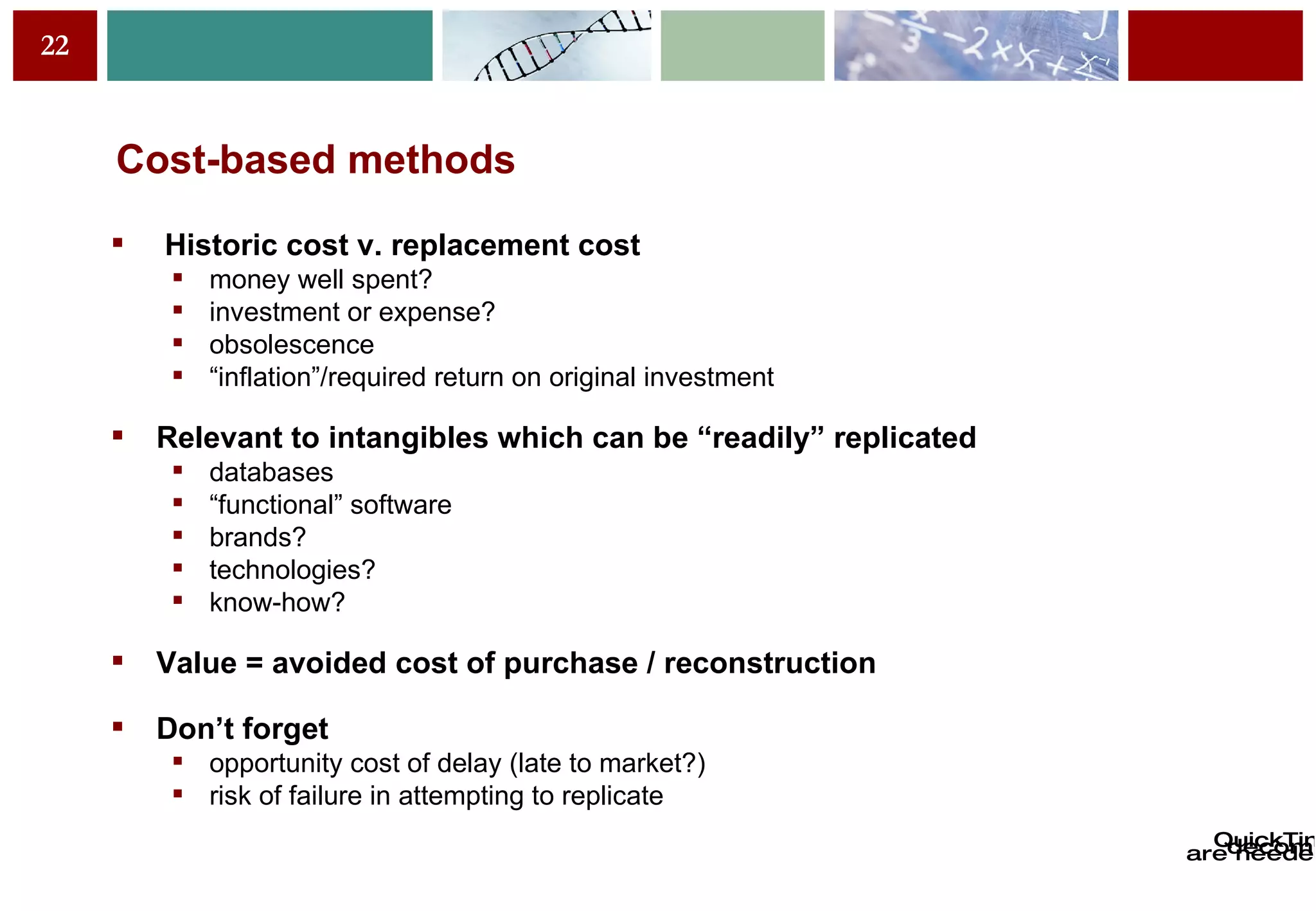

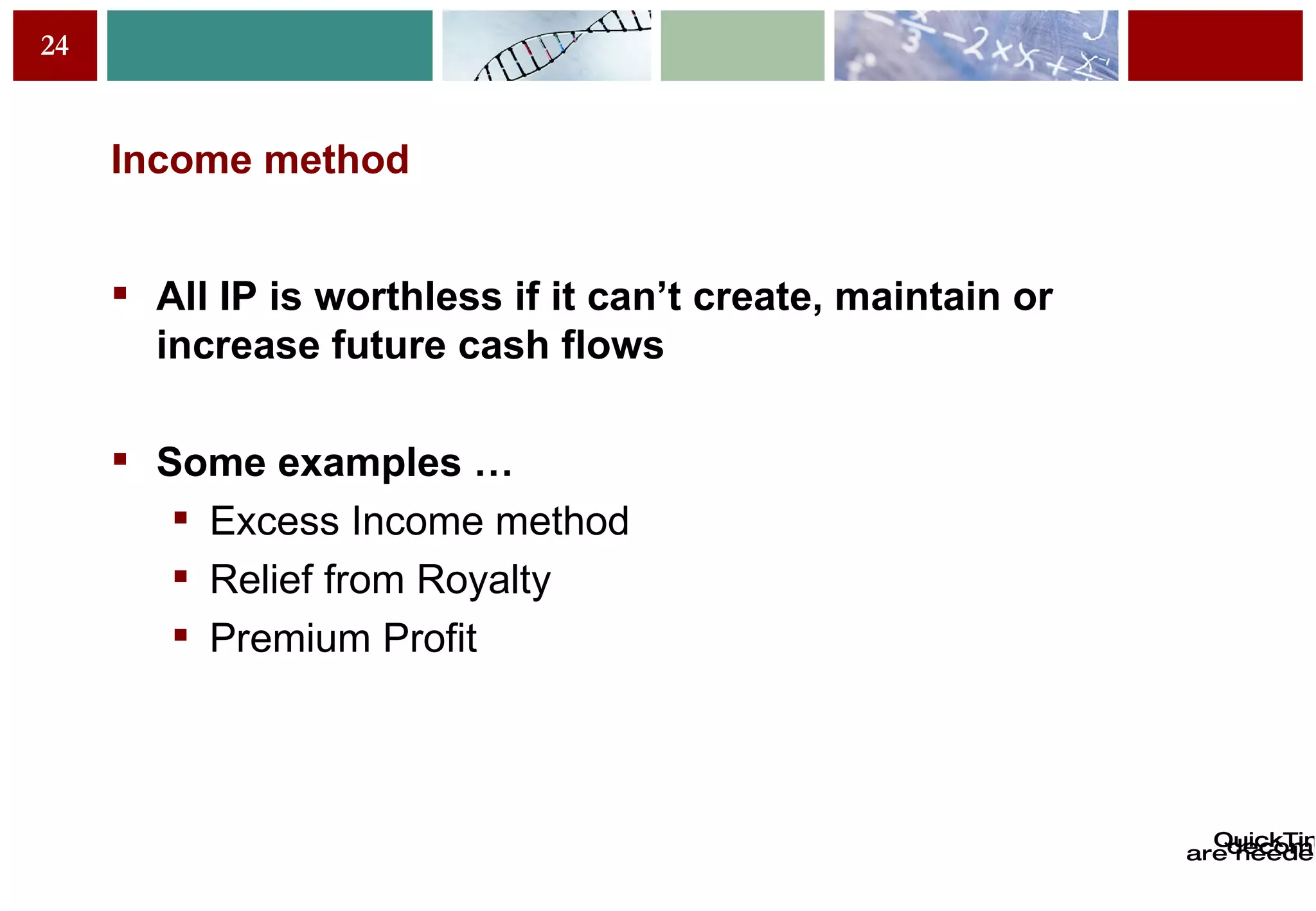

The document discusses intellectual property valuation, assessment, and auditing. It outlines the nine main reasons for valuing IP, including exploitation, taxation purposes, financing, damage assessments, and more. It then describes the three main approaches to valuing IP: cost, market, and income. Challenges in valuing IP include its intangible nature, incomplete information availability, and variability depending on circumstances. Specific methods for valuing patents, trademarks, and assessing IP risks and damage in cases of infringement are also covered. The document concludes by outlining the goals and benefits of conducting an IP audit.