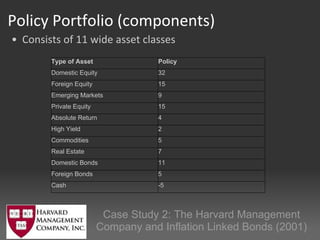

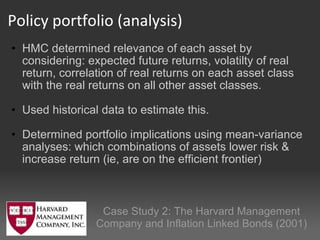

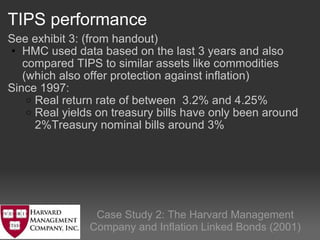

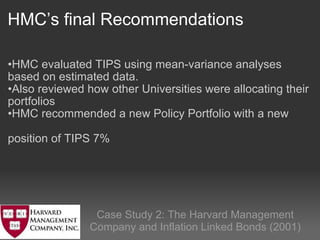

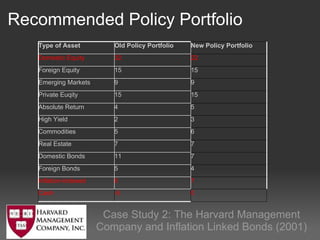

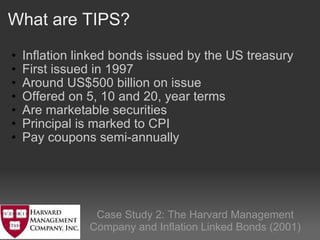

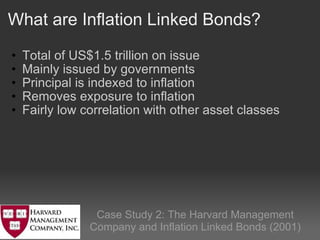

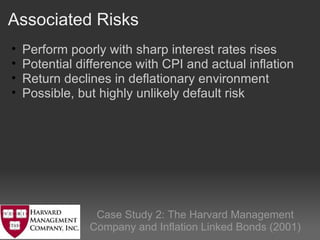

The document discusses Harvard Management Company's (HMC) consideration and adoption of inflation-linked bonds (TIPS) into its investment portfolio. It provides background on HMC and its goal of achieving a 6-7% average annual real return. It then explains what TIPS are and how they work, and analyzes their potential performance in different inflation scenarios. HMC ultimately recommended including a 7% allocation to TIPS in its portfolio to help hedge against inflation risk and improve risk-adjusted returns.