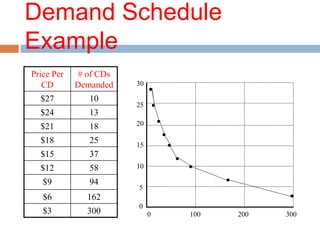

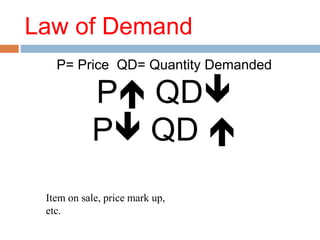

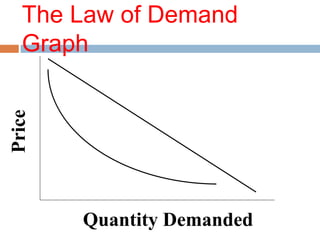

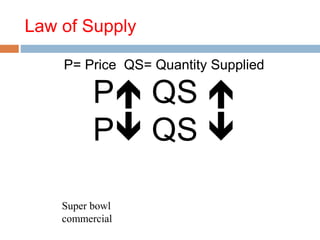

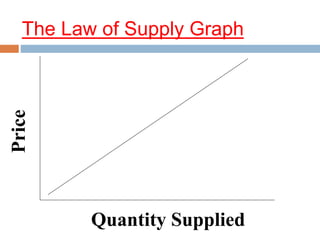

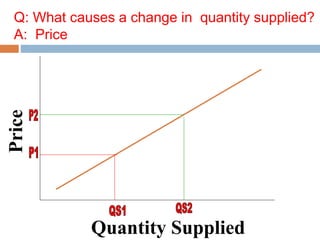

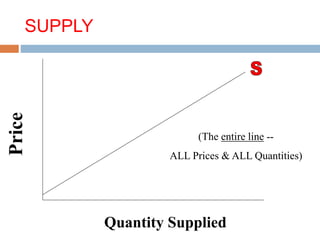

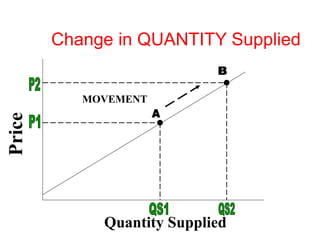

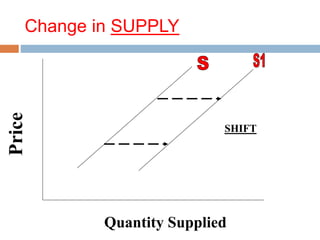

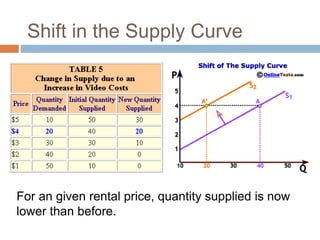

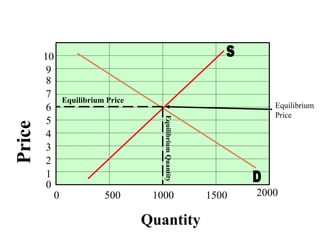

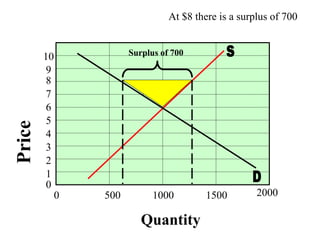

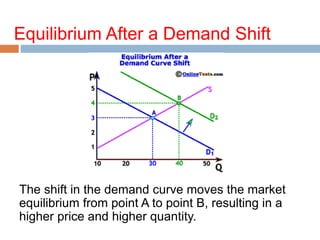

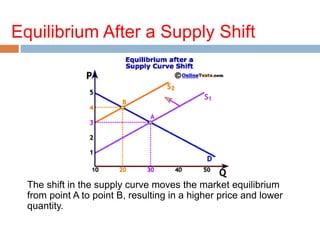

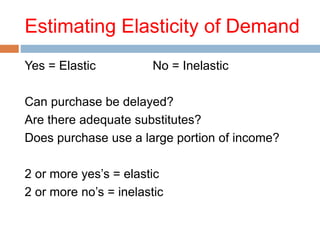

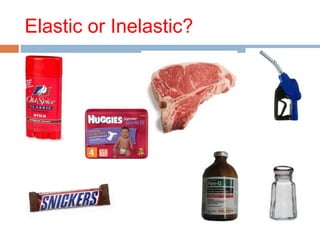

The document discusses supply and demand in economics. It defines demand as the desire, ability, and willingness to buy a product, and supply as the desire, ability, and willingness to offer products for sale. It describes the laws of supply and demand - as price increases, quantity demanded decreases and quantity supplied increases. Non-price factors can cause shifts in supply and demand curves. The goal of markets is to reach equilibrium where quantity supplied equals quantity demanded. Surpluses and shortages occur when supply and demand are not equal. Demand elasticity refers to how responsive quantity demanded is to price changes.