22-1

Prepared by

Prepared by

CobyHarmon

Coby Harmon

University of California, Santa Barbara

University of California, Santa Barbara

Intermediat

Intermediat

e

e

Accounting

Accounting

Intermediat

Intermediat

e

e

Accounting

Accounting

Prepared by

Prepared by

Coby Harmon

Coby Harmon

University of California, Santa Barbara

University of California, Santa Barbara

Westmont College

Westmont College

INTERMEDIATE

ACCOUNTING

F I F T E E N T H E D I T I O N

Prepared by

Coby Harmon

University of California, Santa Barbara

Westmont College

ki

kie

eso

so

w

we

eygandt

ygandt

warfi

warfie

eld

ld

team for success

team for success

2.

22-2

PREVIEW OF CHAPTER

PREVIEWOF CHAPTER

Intermediate Accounting

15th Edition

Kieso Weygandt Warfield

22

22

Changes in

accounting

principle

Changes in

accounting

estimate

Change in

reporting entity

Correction of

errors

Accounting Literature:

APB Opinion 20

FAS 154 (2005, Current GAAP)

(Now listed as ASC Topic 250)

Definition

-

Limited

Coverage

Extended

3.

22-3

5. Describe theaccounting for changes in

estimates.

6. Identify changes in a reporting entity.

7. Describe the accounting for correction of

errors.

8. Identify economic motives for changing

accounting methods.

9. Analyze the effect of errors.

After studying this chapter, you should be able to:

LEARNING OBJECTIVES

LEARNING OBJECTIVES

1. Identify the types of accounting changes.

2. Describe the accounting for changes in

accounting principles.

3. Understand how to account for

retrospective accounting changes.

4. Understand how to account for

impracticable changes.

Accounting Changes

Accounting Changes

and Error Analysis

and Error Analysis

22

22

4.

22-4

Types of AccountingChanges:

1. Change in Accounting Principle (Policy).

2. Changes in Accounting Estimate.

3. Change in Reporting Entity.

Correction of errors are not considered an accounting change.

Accounting Alternatives:

Diminish the comparability and consistency of financial

information.

Obscure useful historical trend data and financial ratios.

Accounting Changes

LO 1

5.

22-5

5. Describe theaccounting for changes in

estimates.

6. Identify changes in a reporting entity.

7. Describe the accounting for correction of

errors.

8. Identify economic motives for changing

accounting methods.

9. Analyze the effect of errors.

After studying this chapter, you should be able to:

LEARNING OBJECTIVES

LEARNING OBJECTIVES

1. Identify the types of accounting changes.

2. Describe the accounting for changes in

accounting principles.

3. Understand how to account for

retrospective accounting changes.

4. Understand how to account for

impracticable changes.

Accounting Changes

Accounting Changes

and Error Analysis

and Error Analysis

22

22

6.

22-6

Average costto FIFO.

Completed-contract to percentage-of-completion method.

Change from one accepted accounting policy to another.

Examples include:

Changes in Accounting Principle

Adoption of a new principle in recognition of events that have

occurred for the first time or that were previously immaterial is not

an accounting change.

Example: implementing a credit sales policy when one had not

previously existed.

LO 2

7.

22-7

Three possible approachesfor reporting changes:

1) Currently (affecting this year’s income only).

2) Retrospectively (affecting RE directly and restating prior

years’ financials).

3) Prospectively (affecting this year and future years).

FASB requires use of the retrospective approach for a change in principle.

Rationale - Users can then better compare results from one period to the next.

LO 2

Changes in Accounting Principle

Retrospectively

8.

22-8

5. Describe theaccounting for changes in

estimates.

6. Identify changes in a reporting entity.

7. Describe the accounting for correction of

errors.

8. Identify economic motives for changing

accounting methods.

9. Analyze the effect of errors.

After studying this chapter, you should be able to:

LEARNING OBJECTIVES

LEARNING OBJECTIVES

1. Identify the types of accounting changes.

2. Describe the accounting for changes in

accounting principles.

3. Understand how to account for

retrospective accounting changes.

4. Understand how to account for

impracticable changes.

Accounting Changes

Accounting Changes

and Error Analysis

and Error Analysis

22

22

9.

22-9

Retrospective Accounting ChangeApproach

Two requirements:

1) Prior years’ financials are restated

Financial statements are adjusted for each prior period

presented to the same basis as the new accounting

principle.

2) RE and other balance sheet account(s) are adjusted

Journal entry adjusts the opening balance of retained

earnings plus carrying amounts of effected assets and

liabilities as of the beginning of the first year presented.

Changes in Accounting Principle

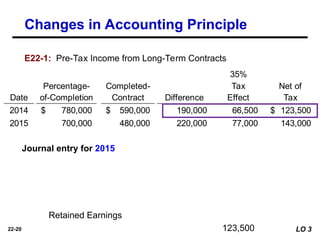

LO 3

10.

22-10

Illustration: Denson Companyhas accounted for its income from

long-term construction contracts using the completed-contract

method. On January 1, 2012, the company changed to the

percentage-of-completion method. Management believes this

approach provides a more appropriate measure of the income

earned. For tax purposes, the company uses the completed-

contract method and plans to continue doing so in the future.

(Assume a 40 percent enacted tax rate.)

LO 3 Understand how to account for retrospective accounting changes.

Retrospective Accounting Change: Long-Term Contracts

Changes in Accounting Principle

11.

22-11 LO 3Understand how to account for retrospective accounting changes.

Income statements for 2010–2012 under each method:

Last Slide

Viewed

Changes in Accounting Principle

(Old Method)

(New Method)

Historically

Historically

reported

reported

Restated

Restated

Calculate

Calculate

cumulative

cumulative

effect of

effect of

change on

change on

prior years

prior years

12.

22-12

Data for RetrospectiveChange

Illustration 22-2

Construction in Process (pre-tax) 220,000

Deferred Tax Liability

88,000

Retained Earnings (after tax)

132,000

LO 3 Understand how to account for retrospective accounting changes.

Journal entry

beginning of

2012

Last Slide

Viewed

Changes in Accounting Principle

(2010)

13.

22-13

Disclosing a Changein Principle in the Notes (example

on next slide):

LO 3 Understand how to account for retrospective accounting changes.

1. Nature of the change in accounting policy;

2. The method of applying the change, and:

a. A description of the prior period information that has been

retrospectively adjusted, if any.

b. The effect of the change on income from continuing operations,

net income (or other appropriate captions of changes in net assets

or performance indicators), any other affected line item.

c. The cumulative effect of the change on retained earnings or other

components of equity or net assets in the balance sheet as of the

beginning of the earliest period presented.

Changes in Accounting Principle

22-15

Adjustment on theRetained Earnings Statement

(Depends on how many years you present;

first let’s consider two years: 2012 and one prior year):

LO 3 Understand how to account for retrospective accounting changes.

Before Change

Go to

Slide

22-12

Go to

Slide

22-11

Back into this number

(if change was not made)

(see Slide 22-12)

(if old method was used)

(if old method was used)

1

1

2

2

3

3

Changes in Accounting Principle

Assume a Retained earnings balance of $1,360,000 at the beginning of 2010.

16.

22-16

LO 3 Understandhow to account for retrospective accounting changes.

Illustration 22-5

After Change

Adjustment on the Retained Earnings Statement (showing

two years, adjustment on the earliest year presented):

Go to

Slide

22-11

(if showing two years

in RE statement)

Changes in Accounting Principle

17.

22-17

LO 3 Understandhow to account for retrospective accounting changes.

Illustration 22-5

Adjustment on the Retained Earnings Statement (showing

one year, adjusting the beginning balance of RE):

Go to

Slide

22-11

(if showing one year

in RE statement)

Changes in Accounting Principle

$1,696,000

(old method: CC)

(old method: CC)

132,000

18.

22-18

E22-1 (Change inPrinciple—Long-Term Contracts): Pam Erickson

Construction Company changed from the completed-contract to the

percentage-of-completion method of accounting for long-term

construction contracts during 2015. For tax purposes, the company

employs the completed-contract method and will continue this

approach in the future. (Hint: Adjust all tax consequences through the

Deferred Tax Liability account.)

Changes in Accounting Principle

LO 3

19.

22-19

Instructions: (assume atax rate of 35%)

(b) What entry(ies) are necessary to adjust the accounting

records for the change in accounting principle?

(a) What is the amount of net income and retained earnings that

would be reported in 2015? Assume beginning retained earnings for

2014 to be $100,000.

Changes in Accounting Principle

LO 3

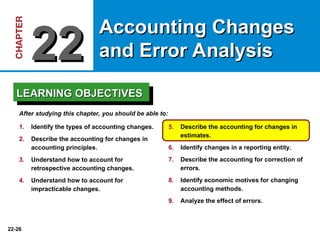

E22-1 (Change in Principle—Long-Term Contracts):

20.

22-20

35%

Percentage- Completed- TaxNet of

Date of-Completion Contract Difference Effect Tax

2014 780,000

$ 590,000

$ 190,000 66,500 123,500

$

2015 700,000 480,000 220,000 77,000 143,000

E22-1: Pre-Tax Income from Long-Term Contracts

Changes in Accounting Principle

LO 3

Journal entry for 2015

Construction in Process 190,000

Deferred Tax Liability

66,500

Retained Earnings

123,500

21.

22-21

Restated Previous

2015 20142014

Pre-tax income 700,000

$ 780,000

$ 590,000

$

Income tax (35%) 245,000 273,000 206,500

Net income 455,000

$ 507,000

$ 383,500

$

Beg. Retained earnings 483,500

$ 100,000

$ 100,000

$

Accounting change 123,500

Beg. R/Es restated 607,000

$ 100,000 100,000

Net income 455,000 507,000 383,500

End. Retained earnings 1,062,000

$ 607,000

$ 483,500

$

Income

Statement

Statement

of Retained

Earnings

E22-1: Comparative Statements for two years:

Changes in Accounting Principle

LO 3

22.

22-22

Direct Effects- FASB takes the position that

companies should retrospectively apply the direct

effects of a change in accounting principle.

Example: Change from LIFO to FIFO directly affects

inventory and deferred taxes

Indirect Effect is any change to current or future cash

flows of a company that result from making a change in

accounting principle that is applied retrospectively.

Example: Executive bonus based on net income

Direct and Indirect Effects of Changes

Changes in Accounting Principle

LO 3

23.

22-23

5. Describe theaccounting for changes in

estimates.

6. Identify changes in a reporting entity.

7. Describe the accounting for correction of

errors.

8. Identify economic motives for changing

accounting methods.

9. Analyze the effect of errors.

After studying this chapter, you should be able to:

LEARNING OBJECTIVES

LEARNING OBJECTIVES

1. Identify the types of accounting changes.

2. Describe the accounting for changes in

accounting principles.

3. Understand how to account for

retrospective accounting changes.

4. Understand how to account for

impracticable changes.

Accounting Changes

Accounting Changes

and Error Analysis

and Error Analysis

22

22

24.

22-24

Impracticability

Companies should notuse retrospective application if one of the

following conditions exists:

1. Company cannot determine the effects of the retrospective

application.

2. Retrospective application requires assumptions about

management’s intent in a prior period (hindsight).

3. Retrospective application requires significant estimates that

the company cannot develop.

If any of the above conditions exists, the company prospectively applies the

new accounting principle.

Changes in Accounting Principle

LO 4

25.

22-25 LO 4Understand how to account for impracticable changes.

Example: A change from the FIFO inventory valuation

method to the LIFO inventory valuation method. It is

virtually impossible reconstruct the old LIFO layers of

inventory over an extended period of time and thus, to

calculate the cumulative effect of the change in principle

LIFO procedures are applied prospectively from the earliest date

practicable (date of the change in this example)

No adjustment of RE is made

It is impracticable to restate prior financials

Changes in Accounting Principle

Impracticability

26.

22-26

5. Describe theaccounting for changes in

estimates.

6. Identify changes in a reporting entity.

7. Describe the accounting for correction of

errors.

8. Identify economic motives for changing

accounting methods.

9. Analyze the effect of errors.

After studying this chapter, you should be able to:

LEARNING OBJECTIVES

LEARNING OBJECTIVES

1. Identify the types of accounting changes.

2. Describe the accounting for changes in

accounting principles.

3. Understand how to account for

retrospective accounting changes.

4. Understand how to account for

impracticable changes.

Accounting Changes

Accounting Changes

and Error Analysis

and Error Analysis

22

22

27.

22-27

Changes in AccountingEstimate

Examples of Estimates

1. Uncollectible receivables (bad debts).

2. Inventory obsolescence.

3. Useful lives and salvage values of assets.

4. Liabilities for warranty costs.

5. Change in depreciation methods.

LO 5

28.

22-28

Prospective Reporting

Changes inaccounting estimates are reported

prospectively. Account for changes in estimates in

1. The period of change if the change affects that period

only, or

2. The period of change and future periods if the change

affects both.

FASB views changes in estimates as normal recurring

corrections and adjustments and prohibits retrospective

treatment.

Changes in Accounting Estimate

LO 5

29.

22-29

Illustration: Arcadia HighSchool purchased equipment for

$510,000 which was estimated to have a useful life of 10 years

with a salvage value of $10,000 at the end of that time.

Depreciation has been recorded for 7 years on a straight-line

basis. In 2014 (year 8), it is determined that the total estimated life

should be 15 years with a salvage value of $5,000 at the end of

that time.

Required:

What is the journal entry to correct

prior years’ depreciation expense?

Calculate depreciation expense for 2014.

Prospective

Method;

No Entry

Required

Changes in Accounting Estimate

LO 5

30.

22-30

Equipment $510,000

Fixed Assets:

Accumulateddepreciation 350,000

Net book value (NBV) $160,000

Balance Sheet (Dec. 31, 2013)

After 7

years

Equipment cost $510,000

Salvage value - 10,000

Depreciable base 500,000

Useful life (original) 10 years

Annual depreciation $ 50,000 x 7 years = $350,000

First, establish NBV

at date of change in

estimate.

Changes in Accounting Estimate

LO 5

31.

22-31

Net book value$160,000

Salvage value (if any) 5,000

Depreciable base 155,000

Useful life 8 years

Annual depreciation $ 19,375

Second, calculate

Second, calculate

depreciation expense

depreciation expense

for 2014.

for 2014.

Depreciation expense 19,375

Accumulated depreciation

19,375

Journal entry for 2014

Changes in Accounting Estimate

LO 5

Advance slide in presentation

mode to reveal answers.

32.

22-32

Disclosures

Companies need notdisclose changes in accounting estimate

made as part of normal operations, such as bad debt

allowances or inventory obsolescence, unless such changes are

material.

However, for a change in estimate that affects several periods

(such as a change in the service lives of depreciable assets),

companies should disclose the effect on income from continuing

operations and related per-share amounts of the current period.

Changes in Accounting Estimate

LO 5

33.

22-33

5. Describe theaccounting for changes in

estimates.

6. Identify changes in a reporting entity.

7. Describe the accounting for correction of

errors.

8. Identify economic motives for changing

accounting methods.

9. Analyze the effect of errors.

After studying this chapter, you should be able to:

LEARNING OBJECTIVES

LEARNING OBJECTIVES

1. Identify the types of accounting changes.

2. Describe the accounting for changes in

accounting principles.

3. Understand how to account for

retrospective accounting changes.

4. Understand how to account for

impracticable changes.

Accounting Changes

Accounting Changes

and Error Analysis

and Error Analysis

22

22

34.

22-34

Change in ReportingEntity

Examples of a change in reporting entity are:

1. Presenting consolidated statements in place of statements of

individual companies.

2. Changing specific subsidiaries that constitute the group of

companies for which the entity presents consolidated financial

statements.

3. Changing the companies included in combined financial

statements.

4. Changing the cost, equity, or consolidation method of

accounting for subsidiaries and investments.

Reported by changing the financial statements of all prior periods

presented (retrospective method).

LO 6

35.

22-35

5. Describe theaccounting for changes in

estimates.

6. Identify changes in a reporting entity.

7. Describe the accounting for correction of

errors.

8. Identify economic motives for changing

accounting methods.

9. Analyze the effect of errors.

After studying this chapter, you should be able to:

LEARNING OBJECTIVES

LEARNING OBJECTIVES

1. Identify the types of accounting changes.

2. Describe the accounting for changes in

accounting principles.

3. Understand how to account for

retrospective accounting changes.

4. Understand how to account for

impracticable changes.

Accounting Changes

Accounting Changes

and Error Analysis

and Error Analysis

22

22

36.

22-36

Accounting Errors

Types ofAccounting Errors:

1. A change from an accounting principle that is not generally

accepted to an accounting policy that is acceptable.

2. Mathematical mistakes.

3. Changes in estimates that occur because a company did

not prepare the estimates in good faith.

4. Failure to accrue or defer certain expenses or revenues.

5. Misuse of facts.

6. Incorrect classification of a cost as an expense instead of

an asset, and vice versa.

LO 7

37.

22-37

All materialerrors must be corrected.

Record corrections of errors from prior periods as an

adjustment to the beginning balance of retained earnings

in the current period.

Such corrections are called prior period adjustments.

For comparative statements, a company should restate the

prior statements affected, to correct for the error

(restatement method).

LO 7

Accounting Errors

38.

22-38

Illustration: In 2015the bookkeeper for Selectro Company

discovered an error. In 2014 the company failed to record

$20,000 of depreciation expense on a newly constructed building.

This building is the only depreciable asset Selectro owns. The

company correctly included the depreciation expense in its tax

return and correctly reported its income taxes payable.

LO 7

Example of Error Correction

This bookkeeper will be looking for a new job soon!

39.

22-39

Selectro’s income statementfor 2014 with and without the error.

Illustration 22-19

LO 7

Example of Error Correction

What are the entries that Selectro should have made and did make

for recording depreciation expense and income taxes?

40.

22-40

Entries that Selectroshould have made and did make for recording

depreciation expense and income taxes.

Illustration 22-20

Example of Error Correction

Illustration 22-19

22-43

Retained Earnings 12,000

Correcting

Entryin

2015

Reversal

LO 7

Example of Error Correction

Prepare the proper correcting entry in 2015, that should be made

by Selectro.

Illustration 22-20

Deferred Tax Liability 8,000

44.

22-44

Retained Earnings 12,000

Correcting

Entryin

2015

LO 7

Example of Error Correction

Prepare the proper correcting entry in 2015, that should be made

by Selectro.

Illustration 22-20

Accumulated Depreciation—Buildings

20,000

Deferred Tax Liability 8,000

45.

22-45

Illustration: Selectro Companyhas a beginning retained earnings

balance at January 1, 2015, of $350,000. The company reports net

income of $400,000 in 2015.

Illustration 22-21

LO 7

Example of Error Correction

Single-Period Statements

46.

22-46

Comparative Statements

Company should

1.Make adjustments to correct the amounts for all affected

accounts reported in the statements for all periods

reported.

2. Restate the data to the correct basis for each year

presented.

3. Show any catch-up adjustment as a prior period

adjustment to retained earnings for the earliest period it

reported.

LO 7

Accounting Errors

47.

22-47

Woods, Inc.

Statement ofRetained Earnings

For the Year Ended December 31, 2014

Balance, January 1 1,050,000

$

Net income 360,000

Dividends (300,000)

Balance, December 31 1,110,000

$

Before issuing the report for the year ended December 31, 2014, you discover

a $62,500 error that caused the 2013 inventory to be overstated (overstated

inventory caused COGS to be lower and thus net income to be higher in

2013). Would this discovery have any impact on the reporting of the

Statement of Retained Earnings for 2014? Assume a 20% tax rate.

LO 7

Accounting Error Illustration

48.

22-48 LO 7

AccountingError Illustration

Woods, Inc.

Statement of Retained Earnings

For the Year Ended December 31, 2014

Balance, January 1 1,050,000

$

Prior period adjustment, net of tax (50,000)

Balance, January 1, as restated 1,000,000

Net income 360,000

Dividends (300,000)

Balance, December 31 1,060,000

$

Advance slide in presentation

mode to reveal answers.

Entry at December 31, 2014 (assuming books have not been closed for 2014):

Retained Earnings 50,000

Deferred Tax Liability 12,500

Inventory 62,500

49.

22-49

Illustration 22-23

LO 7

Summaryof Changes and Errors

Changes in accounting principle are appropriate only when a company

demonstrates that the newly adopted generally accepted accounting

principle is preferable to the existing one. (“Preferable” means the change

constitutes an improvement in financial reporting, not on the basis of

the income tax effect alone).

22-51 LO 7Describe the accounting for correction of errors.

1. Change from FIFO to average cost inventory

method.

2. Change due to overstatement of inventory.

3. Change from sum-of-the-years'-digits to straight-

line method of depreciation.

4. Change from presenting unconsolidated to

consolidated financial statements.

5. Change from LIFO to FIFO inventory method.

6. Change in the rate used to compute warranty costs.

7. Change from an unacceptable accounting principle

to an acceptable accounting principle.

8. Change in a patent's amortization period.

9. Change from completed-contract to percentage-of-

completion method on construction contracts.

10. Change in a plant asset's salvage value.

E22-8 How would these changes be accounted for?

Retrospectively

Retrospectively

Restatement

Restatement

Prospectively

Prospectively

Retrospectively

Retrospectively

Retrospectively

Retrospectively

Prospectively

Prospectively

Restatement

Restatement

Prospectively

Prospectively

Retrospectively

Retrospectively

Prospectively

Prospectively

Summary of Changes and Errors

52.

22-52 LO 7Describe the accounting for correction of errors.

E22-2 Change in Principle: Inventory Methods

Whitman Company began operations on January 1, 2010, and uses the

average cost method of pricing inventory. Management is contemplating a

change in inventory methods for 2013. The following information is

available for the years 2010–2012.

Net Income Computed Using

Net Income Computed Using

Average Cost Method

Average Cost Method FIFO Method

FIFO Method LIFO Method

LIFO Method

2010

2010 $16,000

$16,000 $19,000

$19,000 $12,000

$12,000

2011

2011 18,000

18,000 21,000

21,000 14,000

14,000

2012

2012 20,000

20,000 25,000

25,000 17,000

17,000

Summary of Changes and Errors

53.

22-53 LO 7Describe the accounting for correction of errors.

E22-2 Change in Principle: Inventory Methods

(a) Prepare the journal entry necessary to record a change from

the average cost method to the FIFO method in 2013.

Net Income Computed Using

Net Income Computed Using

Average Cost Method

Average Cost Method FIFO Method

FIFO Method LIFO Method

LIFO Method

2010

2010 $16,000

$16,000 $19,000

$19,000 $12,000

$12,000

2011

2011 18,000

18,000 21,000

21,000 14,000

14,000

2012

2012 20,000

20,000 25,000

25,000 17,000

17,000

Inventory 11,000*

Retained Earnings 11,000

*($19,000 + $21,000 + $25,000) – ($16,000 + $18,000 + $20,000)

Summary of Changes and Errors

54.

22-54 LO 7Describe the accounting for correction of errors.

E22-2 Change in Principle: Inventory Methods

(b) Determine net income to be reported for 2010, 2011, and

2012, after giving effect to the change in accounting principle

Net Income Computed Using

Net Income Computed Using

Average Cost Method

Average Cost Method FIFO Method

FIFO Method LIFO Method

LIFO Method

2010

2010 $16,000

$16,000 $19,000

$19,000 $12,000

$12,000

2011

2011 18,000

18,000 21,000

21,000 14,000

14,000

2012

2012 20,000

20,000 25,000

25,000 17,000

17,000

Net Income (FIFO) 2010 $19,000

2011 21,000

2012 25,000

Summary of Changes and Errors

55.

22-55 LO 7Describe the accounting for correction of errors.

E22-2 Change in Principle: Inventory Methods

(c) Assume Whitman Company used the LIFO method instead

of the average cost method during the years 2010–2012. In

2013, Whitman changed to the FIFO method. Prepare the journal

entry necessary to record the change in principle

Net Income Computed Using

Net Income Computed Using

Average Cost Method

Average Cost Method FIFO Method

FIFO Method LIFO Method

LIFO Method

2010

2010 $16,000

$16,000 $19,000

$19,000 $12,000

$12,000

2011

2011 18,000

18,000 21,000

21,000 14,000

14,000

2012

2012 20,000

20,000 25,000

25,000 17,000

17,000

Inventory 22,000*

Retained Earnings 22,000

*($19,000 + $21,000 + $25,000) – ($12,000 + $14,000 + $17,000)

Summary of Changes and Errors

56.

22-56

5. Describe theaccounting for changes in

estimates.

6. Identify changes in a reporting entity.

7. Describe the accounting for correction of

errors.

8. Identify economic motives for changing

accounting methods.

9. Analyze the effect of errors.

After studying this chapter, you should be able to:

LEARNING OBJECTIVES

LEARNING OBJECTIVES

1. Identify the types of accounting changes.

2. Describe the accounting for changes in

accounting principles.

3. Understand how to account for

retrospective accounting changes.

4. Understand how to account for

impracticable changes.

Accounting Changes

Accounting Changes

and Error Analysis

and Error Analysis

22

22

57.

22-57

LO 10 Makethe computations and prepare the entries necessary to

record a change from or to the equity method of accounting.

Change From The Equity Method

Not covered on the Final Exam

APPENDIX

APPENDIX 22A CHANGING FROM OR TO THE EQUITY METHOD

58.

22-58

RELEVANT FACTS -Similarities

The accounting for changes in estimates is similar between GAAP and

IFRS.

Under GAAP and IFRS, if determining the effect of a change in

accounting policy is considered impracticable, then a company should

report the effect of the change in the period in which it believes it

practicable to do so, which may be the current period. (But…see next

slide for differences.)

LO 11 Compare the procedures for accounting changes

and error analysis under GAAP and IFRS.

59.

22-59

RELEVANT FACTS -Differences

Under IFRS, the impracticality exception applies both to changes in

accounting principles and to the correction of errors. Under GAAP, this

exception applies only to changes in accounting principle.

IFRS (IAS 8) does not specifically address the accounting and reporting

for indirect effects of changes in accounting principles. GAAP has

detailed guidance on the accounting and reporting of indirect effects.

A change to or from LIFO would not occur under IFRS because LIFO is

not a permissible inventory valuation method under IFRS.

LO 11

60.

22-60

Which of thefollowing is not classified as an accounting change by

IFRS?

a. Change in accounting policy.

b. Change in accounting estimate.

c. Errors in financial statements.

d. None of the above.

IFRS SELF-TEST QUESTION

LO 11

61.

22-61

IFRS requires companiesto use which method for reporting changes

in accounting policies?

a. Cumulative effect approach.

b. Retrospective approach.

c. Prospective approach.

d. Averaging approach.

IFRS SELF-TEST QUESTION

LO 11

62.

22-62

Under IFRS, theimpracticality exception applies to

a. Changes involving LIFO.

b. Changes in accounting policy only.

c. Corrections of errors only.

d. Both changes in accounting policy and correction of errors.

IFRS SELF-TEST QUESTION

LO 11