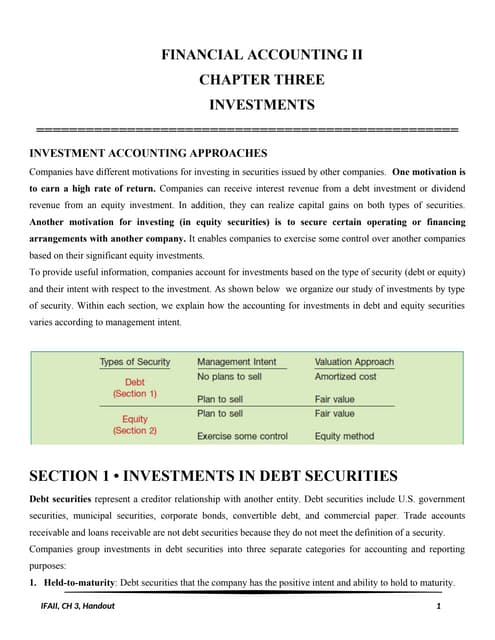

The document explores the accounting treatment of different types of investments in debt and equity securities, including classifications like held-to-maturity, available-for-sale, and trading securities. It details the accounting methods for each category, emphasizing the importance of intent and the need for fair value assessments for certain securities. The document also discusses the implications of ownership percentages on the accounting methods applied, such as the equity method for significant influence investments.