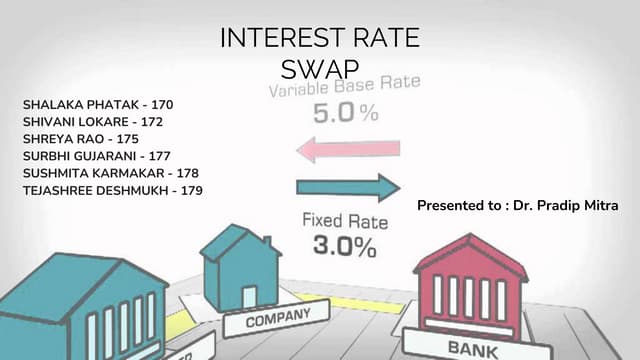

This document explains the concept of interest rate swaps between two companies, detailing their borrowing choices and potential savings. Company A prefers a fixed rate due to expectations of rising rates, while Company B opts for a floating rate anticipating a decline. The document also discusses risks and reasons financial institutions engage in such swaps, including hedging against losses and managing credit risk.