Chapter 12 discusses the fundamentals of interest rate futures, outlining their definition as marketable forward contracts trading on organized exchanges like the CBOT and CME. It covers various aspects including contract specifications, trading procedures, and different types of futures contracts, such as T-bills and Eurodollars, emphasizing their respective trading structures and cash settlement mechanisms. Additionally, the chapter highlights the roles of clearinghouses, alliances among exchanges, and the use of forward rate agreements (FRAs) for managing interest rate risks.

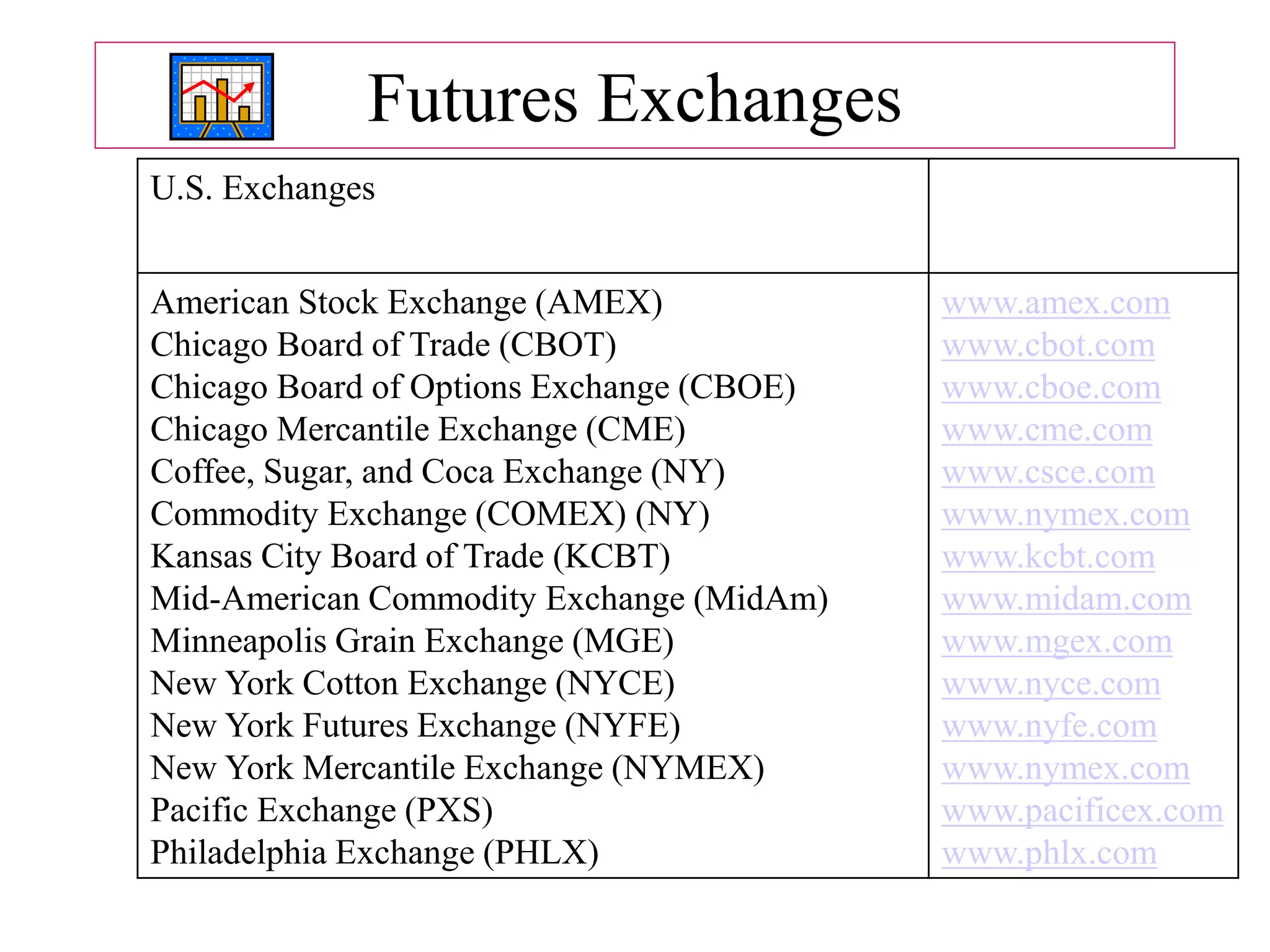

![Margins

• Example: If the initial margin requirement is 5%,

then Speculators A and B in our example would be

required to deposit $49,375 in cash or cash

equivalents in their commodity accounts as good

faith money on their September futures contracts:

m[Contract Value] = .05[$987,500] = $49,375](https://image.slidesharecdn.com/3600854-221125093925-8e99733a/75/Interest-Rate-Futures-58-2048.jpg)