Downloaded 19 times

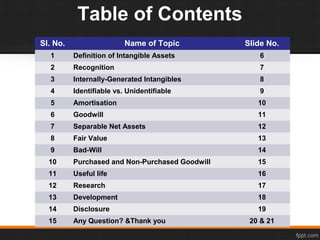

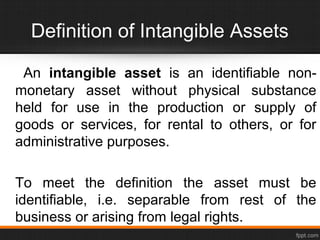

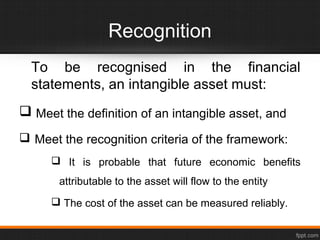

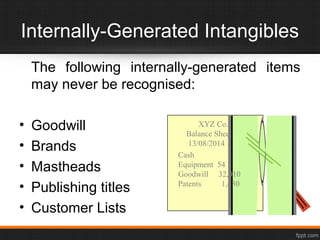

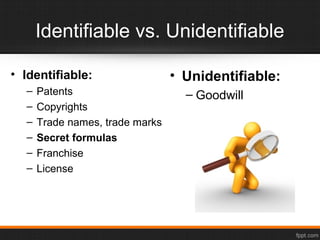

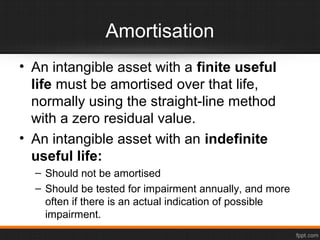

This document provides an overview of intangible assets for a presentation. It defines intangible assets and outlines the criteria for recognition, including that they must be identifiable and provide probable future economic benefits. Internally generated goodwill, brands, and customer lists cannot be recognized. Identifiable assets include patents and trademarks. Goodwill arises from business acquisitions and is the difference between the business value and fair value of separable net assets. Useful life is the period assets are expected to be used, and assets with finite lives must be amortized. Research involves new knowledge, while development applies research to new products. Disclosures include amortization methods and carrying amounts.

![Brennan, Niamh and Connell, Brenda [2000] Intellectual Capital: Current Issue...](https://cdn.slidesharecdn.com/ss_thumbnails/0410brennanconnellintellectualcapitalcurrentissuesandpolicyimplications-121116102513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)