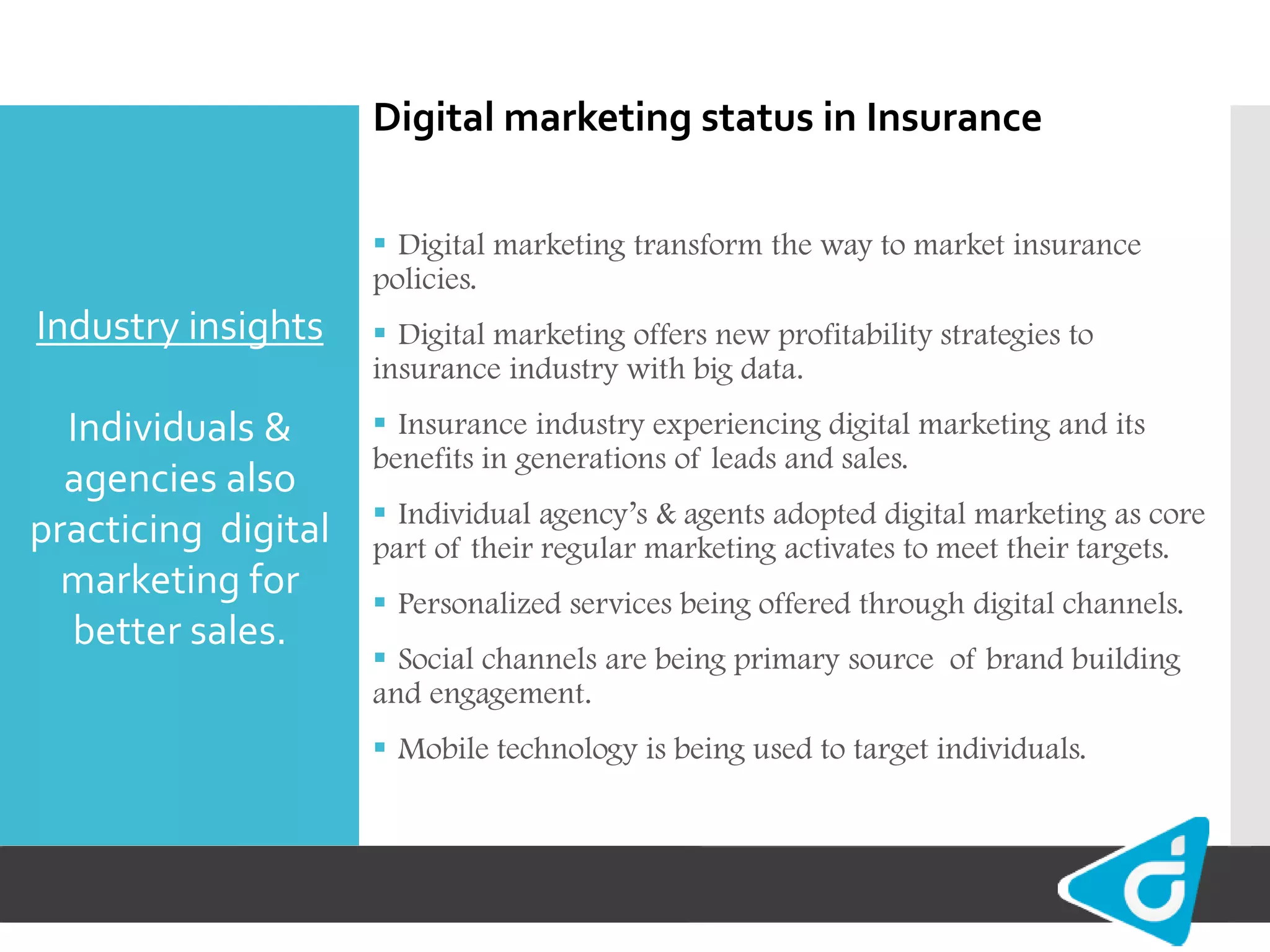

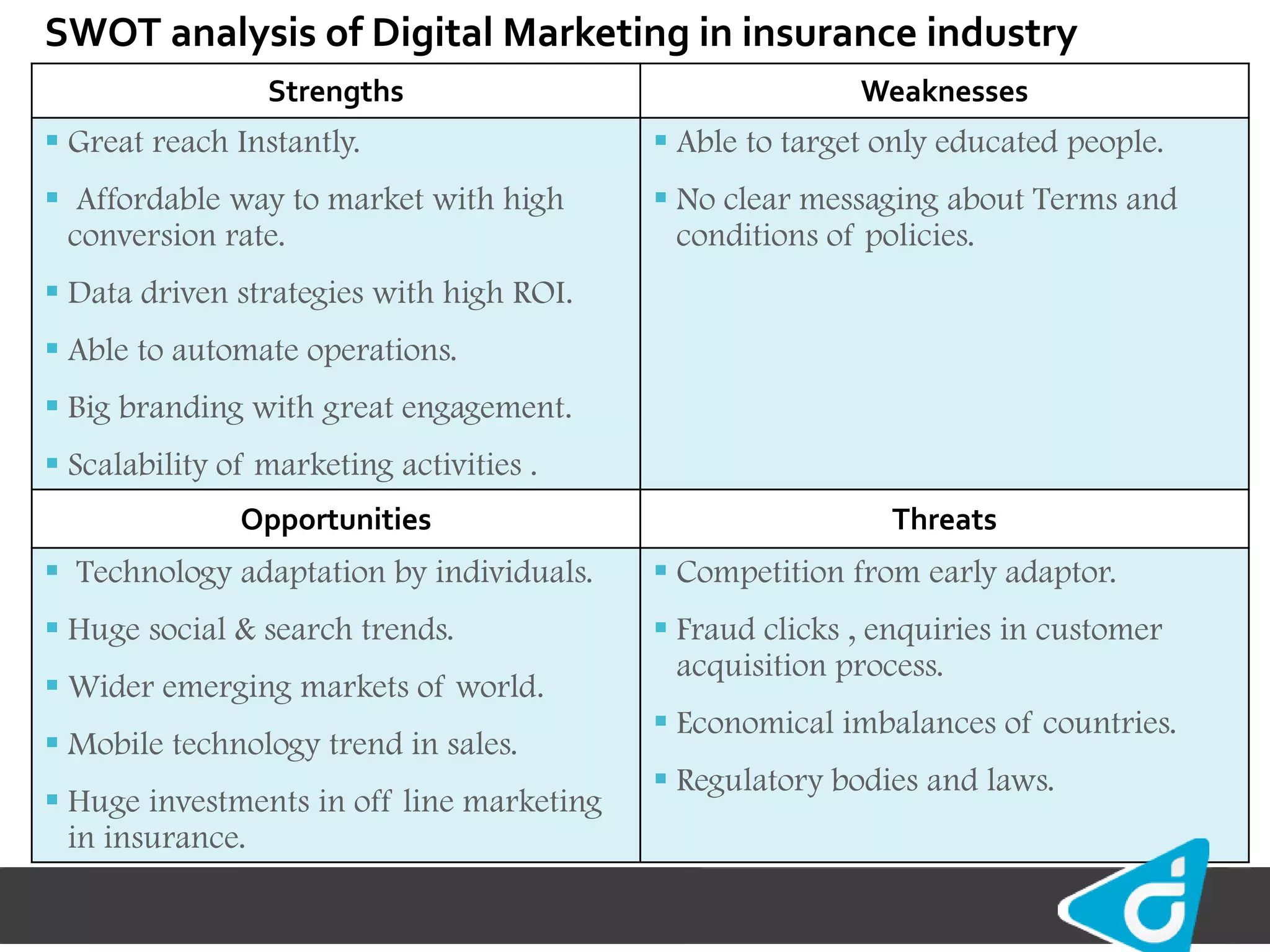

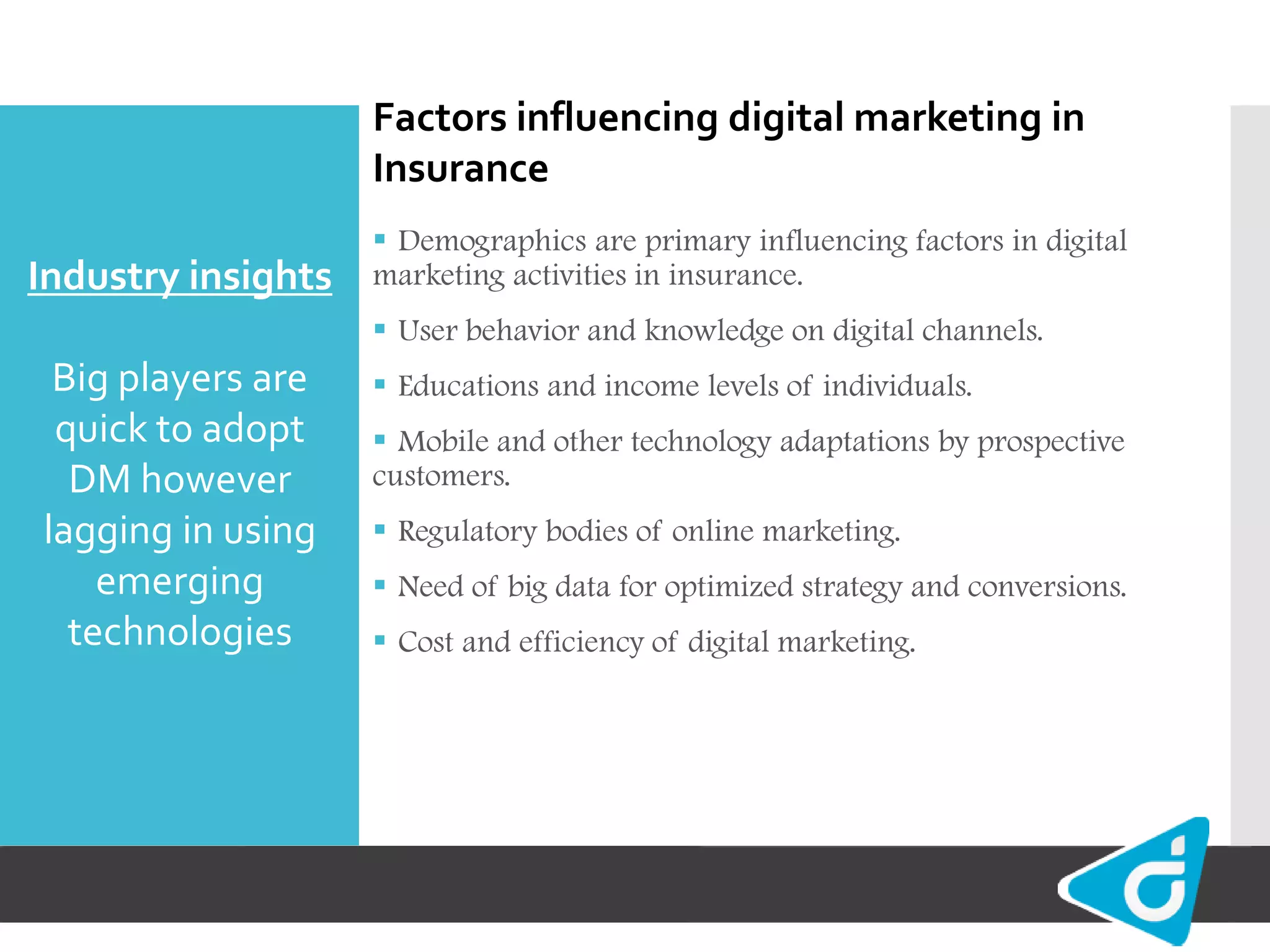

The global insurance industry is rapidly expanding, particularly in life and vehicle insurance, with an annual growth rate of 5% to 10%. Emerging markets, especially in developing countries like India, show significant growth potential, with India's insurance market experiencing up to 34% annual growth. Digital marketing is transforming the industry by enhancing user engagement and targeting, while also offering opportunities through customized services and data-driven strategies.