The document provides an overview of Pine bank including:

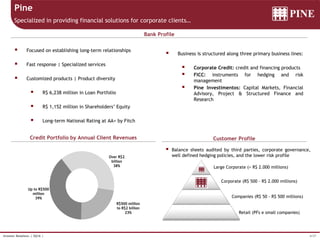

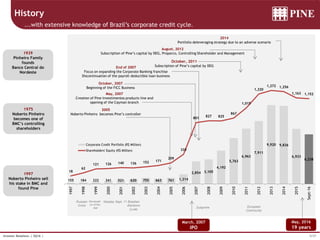

- Its history and focus on corporate clients since 1997

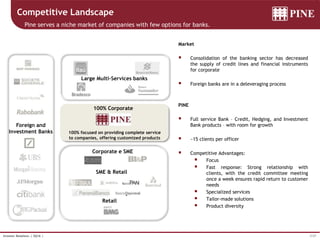

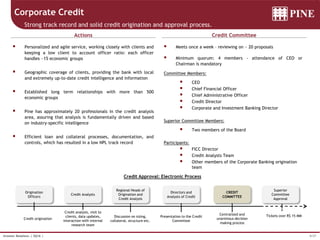

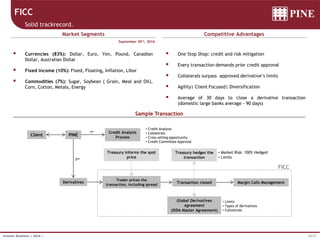

- Business lines in corporate credit, FICC (hedging instruments), and investment banking

- Strong credit approval process and long-term client relationships

- Strategic partnerships with DEG and PROPARCO which provide long-term financing

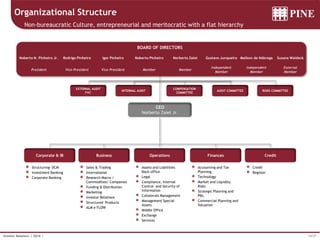

- Corporate governance structure with an entrepreneurial culture