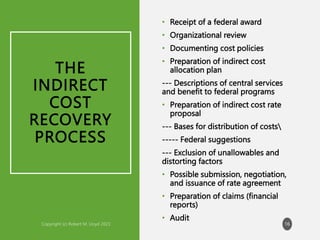

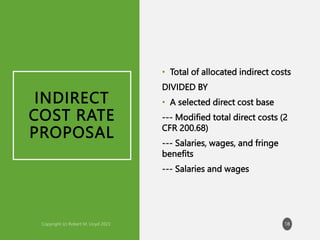

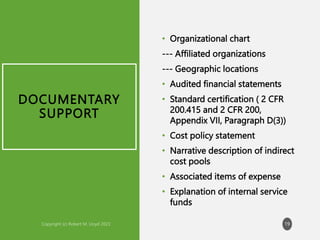

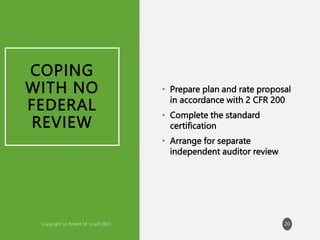

The document discusses indirect cost recovery in the context of economic development funding, highlighting common misconceptions and the definitions of direct and indirect costs. It presents tools like the indirect cost allocation plan and how to determine the applicable indirect cost rate for federal awards under revised policies. Additionally, it outlines the gradual changes and challenges organizations face in the process of recovering indirect costs, including compliance with federal guidelines.