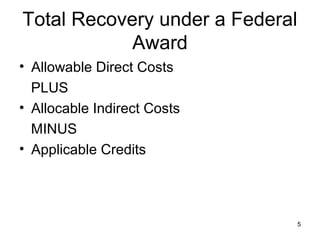

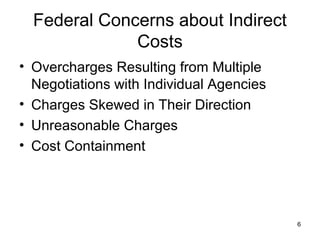

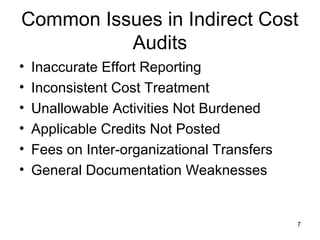

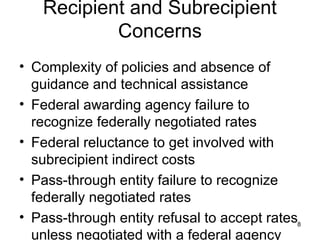

The document discusses the complexities of indirect cost negotiation for grants, outlining the definitions and implications of direct and indirect costs, as well as various federal guidelines and regulations affecting cost recovery. It highlights federal concerns about overcharges, audits, and the need for recognizing federally negotiated rates, along with the importance of accurate budgeting, documentation, and compliance with federal policies. Key changes in cost principles and structures are also addressed, including guidance for developing indirect cost allocation plans and the negotiation processes involved.