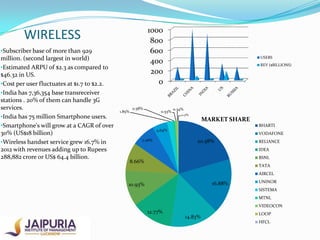

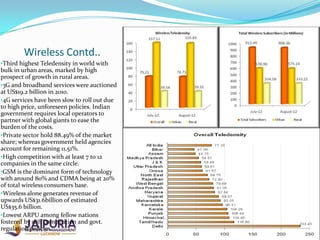

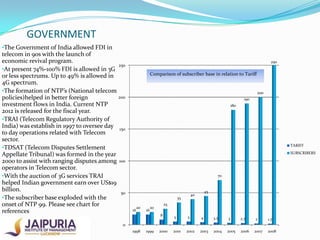

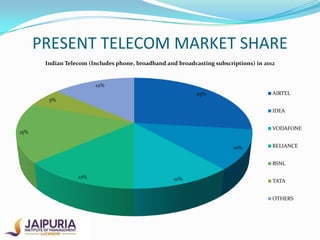

The document provides an overview of the telecommunications industry in India. It discusses that India has the second largest telecom network in the world, with over 929 million wireless subscribers as of 2012. The key areas covered include fixed telephone lines, wireless services, broadband, and broadcasting. It also outlines the major players in the industry such as Bharti Airtel, Reliance, Vodafone and BSNL, as well as the role of the Indian government in regulating the sector through policies and agencies like TRAI.