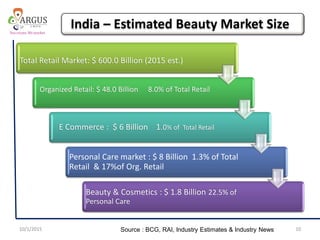

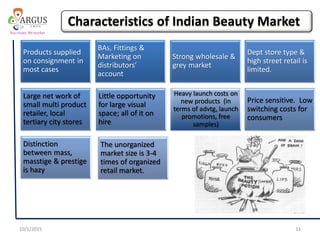

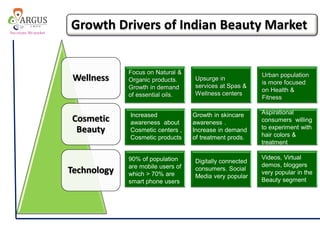

The document provides an overview of India's beauty and personal care market, highlighting its demographics, market segmentation, growth drivers, and regulatory requirements for market entry. It emphasizes the increasing demand for wellness and natural products, the evolving consumer preferences influenced by mobile connectivity, and the significant potential for growth in both urban and tier II/III cities. Additionally, it outlines the investment opportunities and operational guidelines for entering the Indian beauty market.