Ratio and ItsImportance

Ratio analysis express the relationship among selected items of Financial

statement data. A ratio expresses the mathematical relationship between one

quantity and another. The relationship is expressed in terms of percentage, rate or

proportion.

It is an important tool for analyzing the company's financial performance. The

following are the important advantages of the accounting ratios.

1. Analyzing Financial Statements

Ratio analysis is an important technique of financial statement analysis.

Accounting ratios are useful for understanding the financial position of the

company. Different users such as investors, management. bankers and

creditors use the ratio to analyze the financial situation of the company for

their decision making purpose.

2. Judging Efficiency

Accounting ratios are important for judging the company's efficiency in terms

of its operations and management. They help judge how well the company

has been able to utilize its assets and earn profits.

3.

Ratio and ItsImportance

3. Locating Weakness

Accounting ratios can also be used in locating weakness of the

company's operations even though its overall performance may be

quite good. Management can then pay attention to the weakness

and take remedial measures to overcome them.

4. Formulating Plans

Although accounting ratios are used to analyze the company's past

financial performance, they can also be used to establish future

trends of its financial performance. As a result, they help formulate

the company's future plans.

5. Comparing Performance

It is essential for a company to know how well it is performing over

the years and as compared to the other firms of the similar nature.

Besides, it is also important to know how well its different divisions

are performing among themselves in different years. Ratio analysis

facilitates such comparison.

4.

Ratios for FinancialStatement Analysis

Liquidity Ratio

Profitability Ratio

Capital Market Ratio

Other Ratio

5.

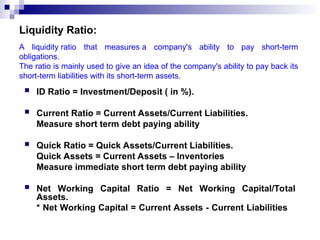

Liquidity Ratio:

IDRatio = Investment/Deposit ( in %).

Current Ratio = Current Assets/Current Liabilities.

Measure short term debt paying ability

Quick Ratio = Quick Assets/Current Liabilities.

Quick Assets = Current Assets – Inventories

Measure immediate short term debt paying ability

Net Working Capital Ratio = Net Working Capital/Total

Assets.

* Net Working Capital = Current Assets - Current Liabilities

A liquidity ratio that measures a company's ability to pay short-term

obligations.

The ratio is mainly used to give an idea of the company's ability to pay back its

short-term liabilities with its short-term assets.

6.

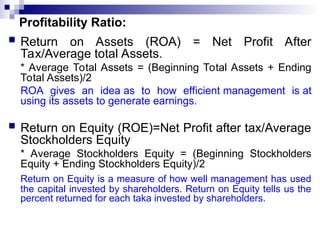

Profitability Ratio:

Returnon Assets (ROA) = Net Profit After

Tax/Average total Assets.

* Average Total Assets = (Beginning Total Assets + Ending

Total Assets)/2

ROA gives an idea as to how efficient management is at

using its assets to generate earnings.

Return on Equity (ROE)=Net Profit after tax/Average

Stockholders Equity

* Average Stockholders Equity = (Beginning Stockholders

Equity + Ending Stockholders Equity)/2

Return on Equity is a measure of how well management has used

the capital invested by shareholders. Return on Equity tells us the

percent returned for each taka invested by shareholders.

7.

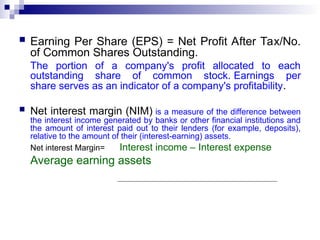

Earning PerShare (EPS) = Net Profit After Tax/No.

of Common Shares Outstanding.

The portion of a company's profit allocated to each

outstanding share of common stock. Earnings per

share serves as an indicator of a company's profitability.

Net interest margin (NIM) is a measure of the difference between

the interest income generated by banks or other financial institutions and

the amount of interest paid out to their lenders (for example, deposits),

relative to the amount of their (interest-earning) assets.

Net interest Margin= Interest income – Interest expense

Average earning assets

8.

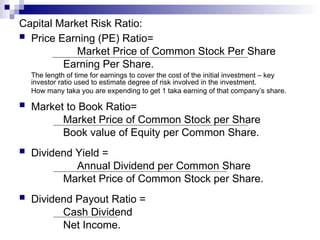

Capital Market RiskRatio:

Price Earning (PE) Ratio=

Market Price of Common Stock Per Share

Earning Per Share.

The length of time for earnings to cover the cost of the initial investment – key

investor ratio used to estimate degree of risk involved in the investment.

How many taka you are expending to get 1 taka earning of that company’s share.

Market to Book Ratio=

Market Price of Common Stock per Share

Book value of Equity per Common Share.

Dividend Yield =

Annual Dividend per Common Share

Market Price of Common Stock per Share.

Dividend Payout Ratio =

Cash Dividend

Net Income.

9.

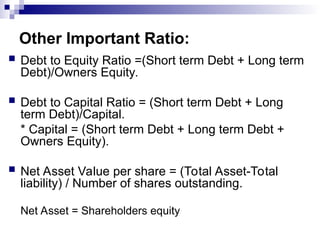

Other Important Ratio:

Debt to Equity Ratio =(Short term Debt + Long term

Debt)/Owners Equity.

Debt to Capital Ratio = (Short term Debt + Long

term Debt)/Capital.

* Capital = (Short term Debt + Long term Debt +

Owners Equity).

Net Asset Value per share = (Total Asset-Total

liability) / Number of shares outstanding.

Net Asset = Shareholders equity

10.

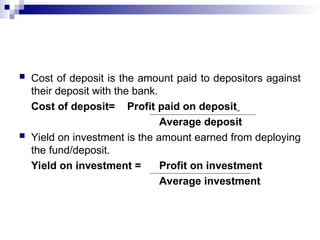

Cost ofdeposit is the amount paid to depositors against

their deposit with the bank.

Cost of deposit= Profit paid on deposit

Average deposit

Yield on investment is the amount earned from deploying

the fund/deposit.

Yield on investment = Profit on investment

Average investment

11.

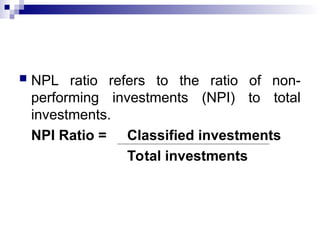

NPL ratiorefers to the ratio of non-

performing investments (NPI) to total

investments.

NPI Ratio = Classified investments

Total investments