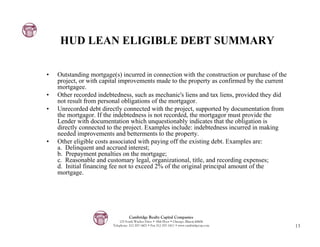

Cambridge Realty Capital Companies provides an overview of HUD 232 Lean Financing, emphasizing its role in senior housing and assisted living financing. The document details Cambridge's history, highlights its financing solutions, recently closed transactions, and the operational benefits of the new lean processing system that streamlines approval times. It also outlines financing terms, underwriting standards, and the focus on efficiency inspired by lean management principles.

![Document About [Accounting Applications]](https://cdn.slidesharecdn.com/ss_thumbnails/documentaboutaccountingapplications-091209031115-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)