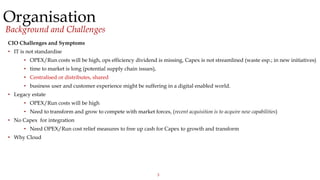

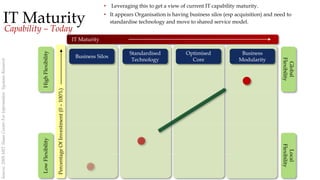

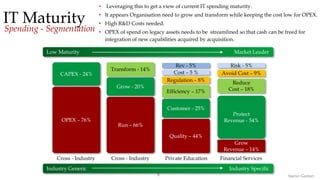

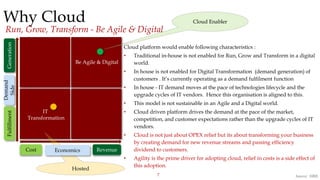

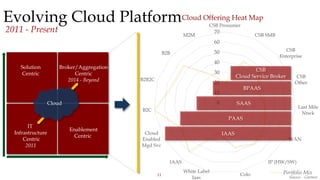

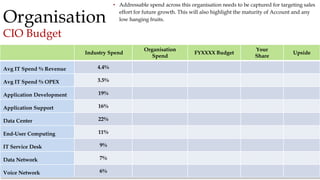

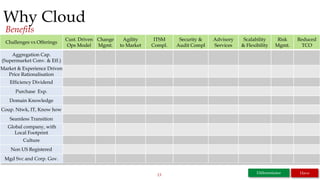

This document discusses moving an organization's IT infrastructure to the cloud. It provides background on the organization's current challenges, including lack of standardization, high operating costs, and inability to quickly transform or grow. The document analyzes the organization's current IT maturity and spending. It argues that cloud adoption would help the organization run, grow, and transform its business in a more agile and digital way. The document outlines cloud offerings and benefits, as well as challenges to address in a cloud sales pitch.