Download to read offline

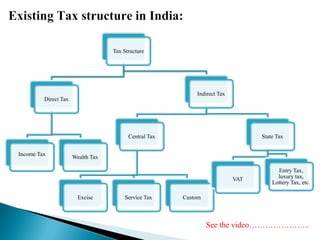

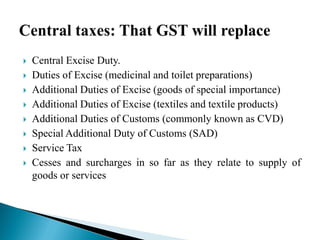

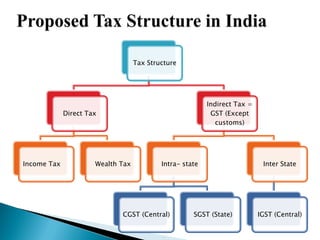

The document provides an overview of the Goods and Services Tax (GST) system implemented in India in July 2017. It discusses how GST unifies several central and state taxes into a single tax system. GST is levied on the final consumption of goods and services, with credits provided for taxes paid at previous stages. A GST Council was established to make recommendations on tax rates and policies. The implementation involved passing legislation at both the central and state government levels.