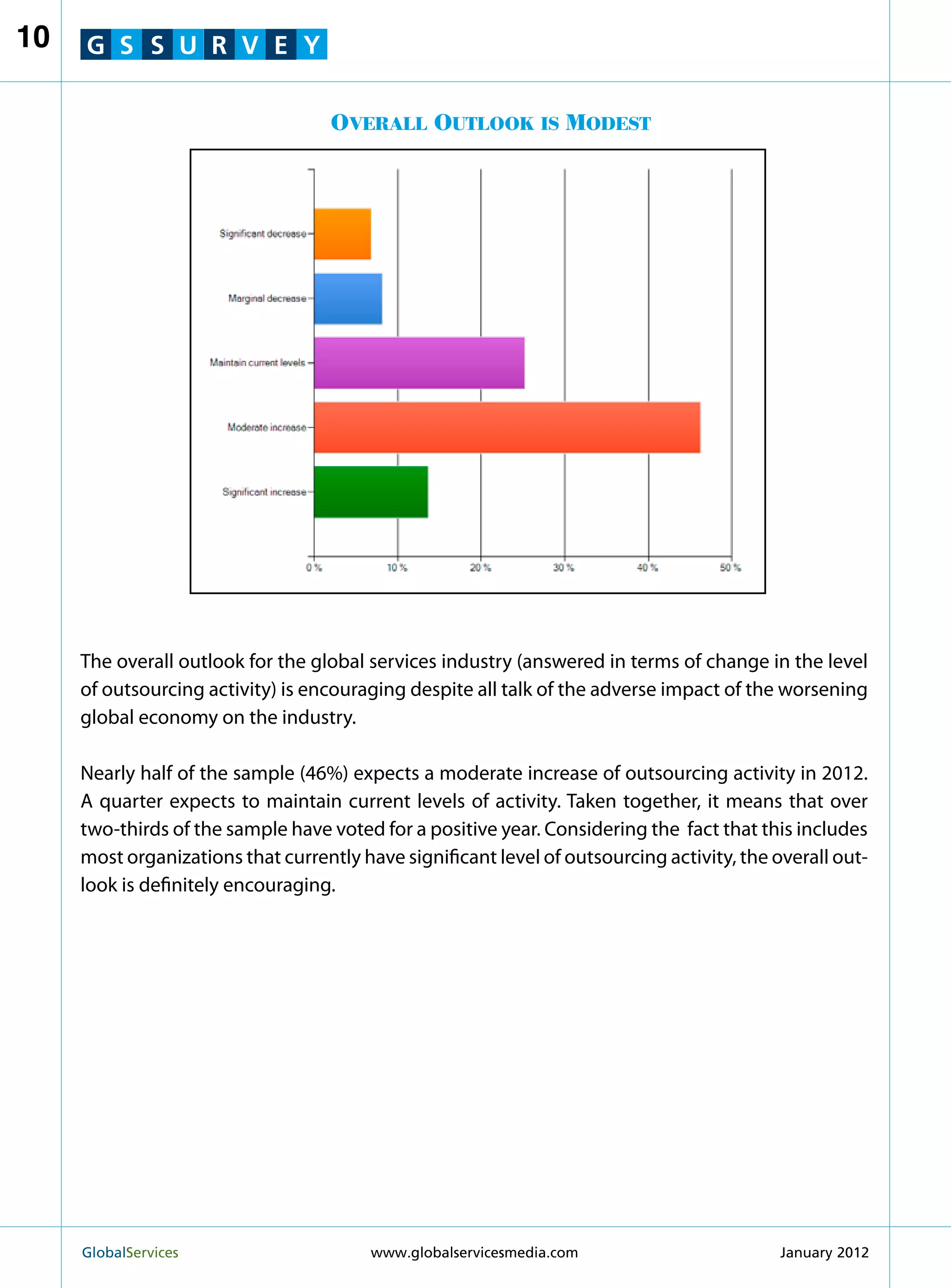

The document summarizes the results of a survey on the 2012 global services industry outlook. Key findings include:

- Nearly half of respondents expect a moderate increase in outsourcing activity in 2022, while a quarter expect current levels to be maintained, indicating an overall positive outlook.

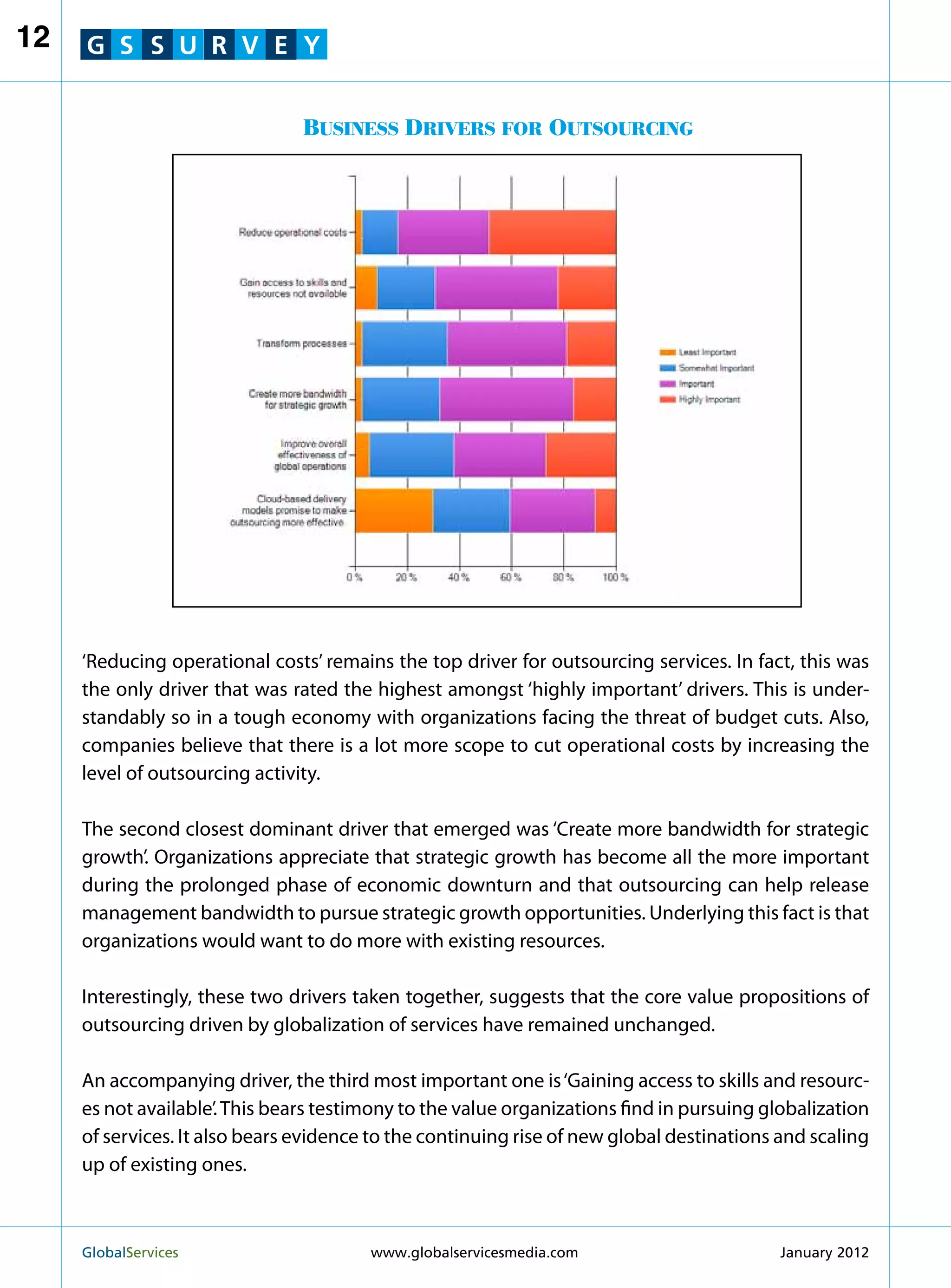

- Reducing operational costs remains the top driver for outsourcing. Creating bandwidth for strategic growth is also an important driver.

- The overall outlook is modest but positive, as reducing costs remains important but organizations also see outsourcing as a way to free up resources for strategic priorities.

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)