Mission Statement

The JapanAirlines Group, as an

overall air transport enterprise,

will act as a bridge to bring peoples,

their cultures and their hearts closer together and thus contribute to

world peace and prosperity. The Japan Airlines Group, a transport

enterprise with a global reach, will expand its worldwide network as

a key industry supporting travel, tourism and transport in the 21st

century, "an era of exchange.”

We will not only transport people and goods to their respective

destinations safely and on time, but will also bring peoples, their

cultures and their hearts closer together as our contribution to world

peace and prosperity.

Business Acumen Defined

• Quickness of perception

• Keen insight

• Mental acuteness

~Wayne Gretzky~

“The Great One”

When asked by a reporter,

“What makes you so great?”

Wayne responded by saying;

“I don’t skate to where the puck is.”

“I skate to where the puck… is going to

be.”

5.

Business

Acumen?

• Quickness

of

perception

• Keen

insight

• Mental

acuteness

The image cannot be displayed. Your computer may not have enough memory to open the image, or the image may have been corrupted. Restart your computer, and then open the file again. If the red x still appears, you may have to

delete the image and then insert it again.

Business

Acumen

101

5

Learning Objectives…

ü Listand describe what key measures are important

to ISD and to Tom Kirchmaier.

ü List and describe the five business drivers all successful

businesses must focus on.

ü Teach specific components of the financial statements.

ü Explain how I can have an impact on growth.

ü Create a personal action plan that can positively

impact our results.

7

8.

Participant Guide Book

Write name & phone number

on the inside cover.

Write name & department

on the name tent.

8

9.

Welcome

ü Participationis encouraged

ü Please turn off phones, tablets, computers, and/

or any other devices that may distract during the

class.

ü Be sure to sign the roster for class recognition

and post class follow-up.

10.

Pop Quiz (GDor ISD numbers) (Page 35)

2011

1- What was our Free Cash Flow?

2- What was our DSO, actual or target?

3- What was Cash from Operating Activities?

4- What was Operating Earnings/Program Profit (EBIT $) ?

5- What was Operating Earnings margin (EBIT %)?

6- What was our Profit Margin (%) ?

7- What was Revenue?

8- What was Revenue Per Employee?

9- How much did Revenues grow?

10-How much did Operating Earning (EBIT) grow?

11- How much did Net Earning growth?

Given all the above, how do we stack up against our competitors?

10

11.

Business can betough!

Ø Only 5-10% of business start-ups survive past 5 years.

Ø 16% of CEOs lose their job every year.

Booz Allen Hamilton 5th annual Study

Ø 70% of merger and acquisition activity do not live

up to expectation. Wall Street Journal 2007

So why do businesses fail?

12.

Business Acumen

“Whenit comes to running a business

successfully, the street vendor and the

CEOs of some of the world’s largest

and most successful companies talk

and think very much alike.” Ram Charan

5-Step Approach per Driver:

• Define the driver.

• Know why it is important.

• Know how we measure it.

• Discover our numbers (& comp).

• Create an Action Plan.

13.

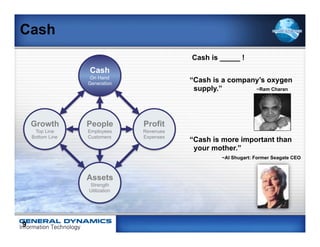

Cash

Cash is _____ !

Cash

On Hand

Generation

“Cash is a company’s oxygen

supply.” ~Ram Charan

Growth People Profit

Top Line Employees Revenues

Bottom Line Customers Expenses

“Cash is more important than

your mother.”

~Al Shugart: Former Seagate CEO

Assets

Strength

Utilization

9

14.

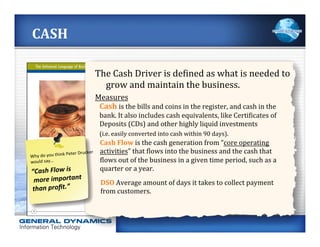

CASH

The

Cash

Driver

is

de;ined

as

what

is

needed

to

grow

and

maintain

the

business.

Measures

Cash

is

the

bills

and

coins

in

the

register,

and

cash

in

the

bank.

It

also

includes

cash

equivalents,

like

Certi;icates

of

Deposits

(CDs)

and

other

highly

liquid

investments

(i.e.

easily

converted

into

cash

within

90

days).

Cash

Flow

is

the

cash

generation

from

“core

operating

Peter

Drucker

activities”

that

;lows

into

the

business

and

the

cash

that

Why

do

you

think

would

say…

;lows

out

of

the

business

in

a

given

time

period,

such

as

a

“Cash

Flow

is

quarter

or

a

year.

more

important

DSO

Average

amount

of

days

it

takes

to

collect

payment

than

profit.”

from

customers.

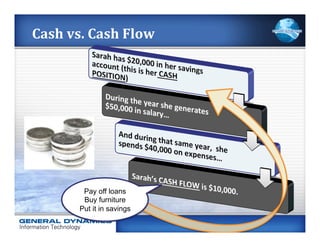

15.

Cash

vs.

Cash

Flow

Pay off loans

Buy furniture

Put it in savings

16.

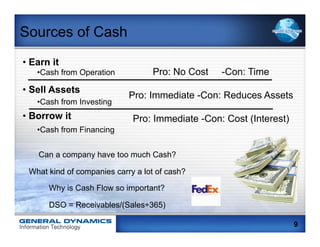

Sources of Cash

• Earn it

• Cash from Operation Pro: No Cost -Con: Time

• Sell Assets

Pro: Immediate -Con: Reduces Assets

• Cash from Investing

• Borrow it Pro: Immediate -Con: Cost (Interest)

• Cash from Financing

Can a company have too much Cash?

What kind of companies carry a lot of cash?

Why is Cash Flow so important?

DSO = Receivables/(Sales÷365)

9

17.

How Much Cash?

A company should have sufficient cash to

cover…

• their interest

• current expenses

• capital expenditures

• plus a little for emergencies

~ Investopedia

9

18.

Top 5 Usesof Cash

Top 5 Uses of Cash

Dividend Pay-Outs Research and Development

(R&D)

Stock Buy-Back Capital Expenditures

(CAPEX)

Mergers and Acquisitions

(M&A)

9

19.

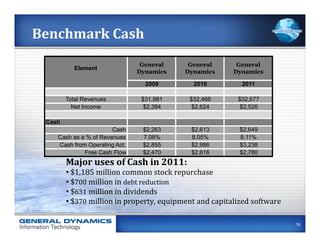

Benchmark

Cash

General General General

Element

Dynamics Dynamics Dynamics

2009 2010 2011

Total Revenues $31,981 $32,466 $32,677

Net Income $2,394 $2,624 $2,526

Cash

Cash $2,263 $2,613 $2,649

Cash as a % of Revenues 7.08% 8.05% 8.11%

Cash from Operating Act. $2,855 $2,986 $3,238

Free Cash Flow $2,470 $2,616 $2,780

Major

uses

of

Cash

in

2011:

•

$1,185

million

common

stock

repurchase

•

$700

million

in

debt

reduction

•

$631

million

in

dividends

•

$370

million

in

property,

equipment

and

capitalized

software

19

20.

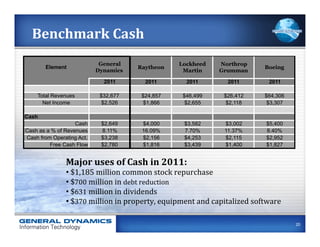

Benchmark

Cash

General Lockheed Northrop

Element Raytheon Boeing

Dynamics Martin Grumman

2011 2011 2011 2011 2011

Total Revenues $32,677 $24,857 $46,499 $26,412 $64,306

Net Income $2,526 $1,866 $2,655 $2,118 $3,307

Cash

Cash $2,649 $4,000 $3,582 $3,002 $5,400

Cash as a % of Revenues 8.11% 16.09% 7.70% 11.37% 8.40%

Cash from Operating Act. $3,238 $2,156 $4,253 $2,115 $2,952

Free Cash Flow $2,780 $1,816 $3,439 $1,400 $1,827

Major

uses

of

Cash

in

2011:

•

$1,185

million

common

stock

repurchase

•

$700

million

in

debt

reduction

•

$631

million

in

dividends

•

$370

million

in

property,

equipment

and

capitalized

software

20

21.

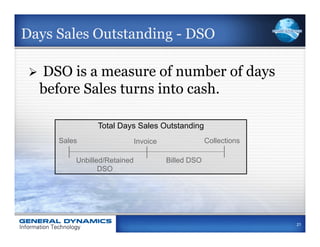

Days Sales Outstanding- DSO

Ø DSO is a measure of number of days

before Sales turns into cash.

Total Days Sales Outstanding

Sales Invoice Collections

Unbilled/Retained Billed DSO

DSO

21

22.

How PMs impactcash/cash flow

ü Manage billing milestones – efficiently execute completion milestones

ü Minimize time from task completion to payment (Days Sales Outstanding – DSO)

ü Ensure timecard compliance

§ Timely – DAILY input / accurate entry of time worked

§ Establishment and communication of proper charge numbers

§ Pre-emptive discussion on how to charge in weather calamities, training, etc.

ü Timely review/approval of subcontractor and consultant invoices

ü Focus on timely submittal of invoices and hours by subcontractors

ü Fully participate and understand monthly financial reviews

ü Maximize profitability

ü Update and post CESRs (Certificate of Engineering Services Rendered) within 5

business days

ü Excellent contract performance

§ Equates to happy customer who doesn’t protest invoices or delay payments due

to dissatisfaction

22

23.

Impacting the CashDriver

Late Timecard Submissions

Negatively Impact Our Bottom Line

The annual cost impact to GDIT when people submit their timecards late is in excess

of $600K in administrative and compensation costs.

This comes in the form of the Payroll organization working Saturdays to process

these late cards as well as in the form of administrative personnel across the

company chasing delinquent employees.

In addition, if a timecard is submitted late, costing and invoice generation is

understated, all of which negatively impacts company cash flow.

So PLEASE make sure to submit your timecard and have all your people submit

their timecards each Friday by the close of business.

23

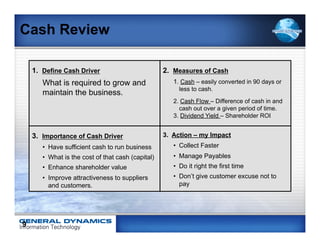

Cash Review

1. Define Cash Driver 2. Measures of Cash

What is required to grow and 1. Cash – easily converted in 90 days or

less to cash.

maintain the business.

2. Cash Flow – Difference of cash in and

cash out over a given period of time.

3. Dividend Yield – Shareholder ROI

3. Importance of Cash Driver 3. Action – my Impact

• Have sufficient cash to run business • Collect Faster

• What is the cost of that cash (capital) • Manage Payables

• Enhance shareholder value • Do it right the first time

• Improve attractiveness to suppliers • Don’t give customer excuse not to

and customers. pay

9

26.

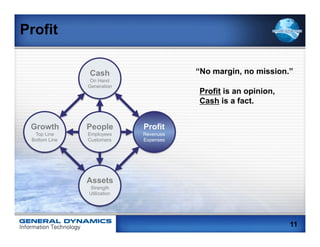

Profit

Cash “No margin, no mission.”

On Hand

Generation

Profit is an opinion,

Cash is a fact.

Growth People Profit

Top Line Employees Revenues

Bottom Line Customers Expenses

Assets

Strength

Utilization

11

27.

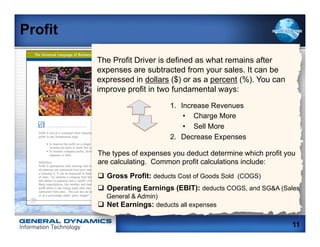

Profit

The Profit Driver is defined as what remains after

expenses are subtracted from your sales. It can be

expressed in dollars ($) or as a percent (%). You can

improve profit in two fundamental ways:

1. Increase Revenues

• Charge More

• Sell More

2. Decrease Expenses

The types of expenses you deduct determine which profit you

are calculating. Common profit calculations include:

q Gross Profit: deducts Cost of Goods Sold (COGS)

q Operating Earnings (EBIT): deducts COGS, and SG&A (Sales

General & Admin)

q Net Earnings: deducts all expenses

11

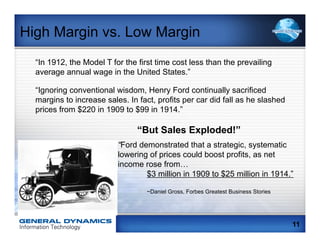

High Margin vs.Low Margin

“In 1912, the Model T for the first time cost less than the prevailing

average annual wage in the United States.”

“Ignoring conventional wisdom, Henry Ford continually sacrificed

margins to increase sales. In fact, profits per car did fall as he slashed

prices from $220 in 1909 to $99 in 1914.”

“But Sales Exploded!”

“Ford demonstrated that a strategic, systematic

lowering of prices could boost profits, as net

income rose from…

$3 million in 1909 to $25 million in 1914.”

~Daniel Gross, Forbes Greatest Business Stories

11

30.

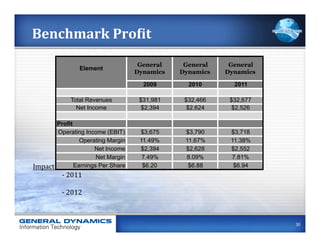

Benchmark

ProCit

General General General

Element

Dynamics Dynamics Dynamics

2009 2010 2011

Total Revenues $31,981 $32,466 $32,677

Net Income $2,394 $2,624 $2,526

Profit

Operating Income (EBIT) $3,675 $3,790 $3,718

Operating Margin 11.49% 11.67% 11.38%

Net Income $2,394 $2,628 $2,552

Net Margin 7.49% 8.09% 7.81%

Impact

to

Pro;it:

Reduce

Share and

drive

operational

excellence

$6.94

Earnings Per costs

$6.20 $6.88

-‐

2011

-‐

2012

30

31.

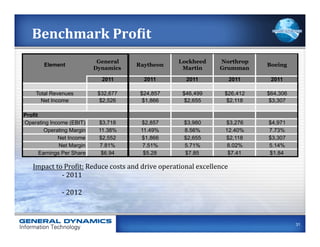

Benchmark

ProCit

General Lockheed Northrop

Element Raytheon Boeing

Dynamics Martin Grumman

2011 2011 2011 2011 2011

Total Revenues $32,677 $24,857 $46,499 $26,412 $64,306

Net Income $2,526 $1,866 $2,655 $2,118 $3,307

Profit

Operating Income (EBIT) $3,718 $2,857 $3,980 $3,276 $4,971

Operating Margin 11.38% 11.49% 8.56% 12.40% 7.73%

Net Income $2,552 $1,866 $2,655 $2,118 $3,307

Net Margin 7.81% 7.51% 5.71% 8.02% 5.14%

Earnings Per Share $6.94 $5.28 $7.85 $7.41 $1.84

Impact

to

Pro;it:

Reduce

costs

and

drive

operational

excellence

-‐

2011

-‐

2012

31

32.

Profit in Action

GeneralMills: Hot’n Spicy Chex Mix:

“We had 14 different pretzel shapes.

By getting rid of some of them,

we save $1 million a year.”

Yoplait: Ditched multicolored lids, saving $2 million a year:

Airlines: Baggage Fees grew airline revenues by $3.8B

11

33.

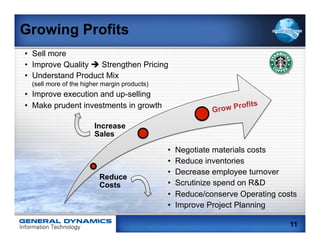

Growing Profits

• Sellmore

• Improve Quality è Strengthen Pricing

• Understand Product Mix

(sell more of the higher margin products)

• Improve execution and up-selling

• Make prudent investments in growth fits

Gr ow Pro

Increase

Sales

• Negotiate materials costs

• Reduce inventories

• Decrease employee turnover

Reduce

Costs • Scrutinize spend on R&D

• Reduce/conserve Operating costs

• Improve Project Planning

11

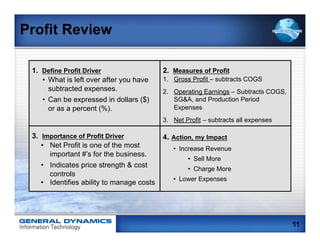

Profit Review

1.Define Profit Driver 2. Measures of Profit

• What is left over after you have 1. Gross Profit – subtracts COGS

subtracted expenses. 2. Operating Earnings – Subtracts COGS,

• Can be expressed in dollars ($) SG&A, and Production Period

or as a percent (%). Expenses

3. Net Profit – subtracts all expenses

3. Importance of Profit Driver 4. Action, my Impact

• Net Profit is one of the most • Increase Revenue

important #’s for the business.

• Sell More

• Indicates price strength & cost • Charge More

controls

• Lower Expenses

• Identifies ability to manage costs

11

36.

High

Margin

vs.

Low

Margin

High

Margins

Low

Margins

33.6%

7.9%

30.0%

3.9%

21.5%

1.4%

WHY?

WHY?

They

offer

something

Unique!

They

sell

commodities.

“If

you’re

not

unique,

you

better

be

cheap!”

To

drive

ProCit($)

you

need

either:

High

Margin

(%)

or

High

Velocity

(Volume)

36

37.

How do PMsimpact profit?

• Watch expenses;

– Manage cost budgets, approve only costs that have relevance and a business need

– Approve only training that satisfies business needs

• Set training expectations with employee – what you expect them to do with the

knowledge when they return to work

• Limit travel expenses for training, when possible

• Staffing with qualified, but less expensive personnel

– Create a staffing model to bring in junior, less expensive talent as senior employees move

into next career position

• Learn to effectively use management reserve

• Effective program execution

• Continuous process improvement – minimize waste, and reduce costs

• High Customer satisfaction – award fees

37

38.

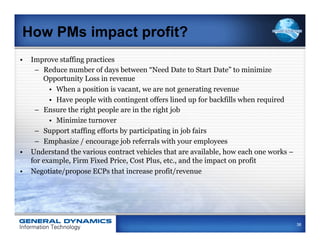

How PMs impactprofit?

• Improve staffing practices

– Reduce number of days between “Need Date to Start Date” to minimize

Opportunity Loss in revenue

• When a position is vacant, we are not generating revenue

• Have people with contingent offers lined up for backfills when required

– Ensure the right people are in the right job

• Minimize turnover

– Support staffing efforts by participating in job fairs

– Emphasize / encourage job referrals with your employees

• Understand the various contract vehicles that are available, how each one works –

for example, Firm Fixed Price, Cost Plus, etc., and the impact on profit

• Negotiate/propose ECPs that increase profit/revenue

38

39.

Assets

Cash Anything we own or control

On Hand

Generation

which has value

What we have, and how well

Growth People Profit we use what we have.

Top Line Employees Revenues

Bottom Line Customers Expenses

Assets

Strength

Utilization

People are our biggest asset!

13

40.

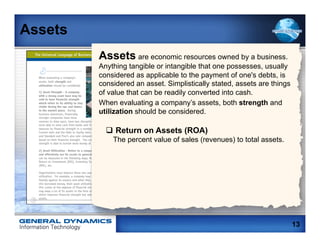

Assets

Assets are economic resources owned by a business.

Anything tangible or intangible that one possesses, usually

considered as applicable to the payment of one's debts, is

considered an asset. Simplistically stated, assets are things

of value that can be readily converted into cash.

When evaluating a company’s assets, both strength and

utilization should be considered.

q Return on Assets (ROA)

The percent value of sales (revenues) to total assets.

13

41.

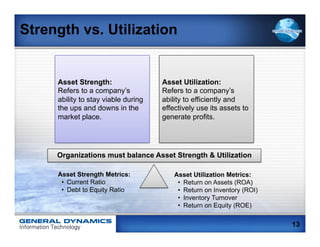

Strength vs. Utilization

Asset Strength: Asset Utilization:

Refers to a company’s Refers to a company’s

ability to stay viable during ability to efficiently and

the ups and downs in the effectively use its assets to

market place. generate profits.

Organizations must balance Asset Strength & Utilization

Asset Strength Metrics: Asset Utilization Metrics:

• Current Ratio • Return on Assets (ROA)

• Debt to Equity Ratio • Return on Inventory (ROI)

• Inventory Turnover

• Return on Equity (ROE)

13

42.

Assets in Action

The modern charcoal briquette was invented by

automaker Henry Ford. Ford operated a

sawmill in the forests around Iron Mountain,

Michigan, in the years prior to 1920 to make

wooden parts for his Model T. As the piles of

wood scraps began to grow, so did Ford's

eagerness to find an efficient way of using

them. He learned of a process developed and

patented by Orin F. Stafford. The process

involved chipping wood into small pieces,

converting it into charcoal, grinding the charcoal

into powder, adding a binder and compressing

the mix into the now-familiar, pillow-shaped

briquette. By 1921, a charcoal-making plant

was in full operation.

13

43.

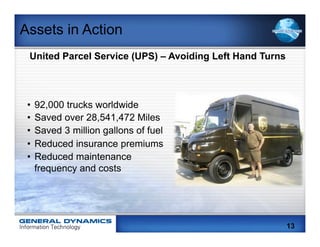

Assets in Action

United Parcel Service (UPS) – Avoiding Left Hand Turns

• 92,000 trucks worldwide

• Saved over 28,541,472 Miles

• Saved 3 million gallons of fuel

• Reduced insurance premiums

• Reduced maintenance

frequency and costs

13

44.

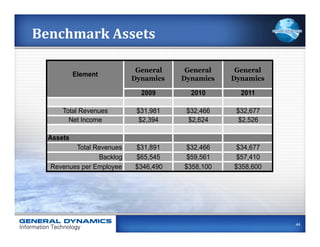

Benchmark

Assets

General General General

Element

Dynamics Dynamics Dynamics

2009 2010 2011

Total Revenues $31,981 $32,466 $32,677

Net Income $2,394 $2,624 $2,526

Assets

Total Revenues $31,891 $32,466 $34,677

Backlog $65,545 $59,561 $57,410

Revenues per Employee $346,490 $358,100 $358,600

44

45.

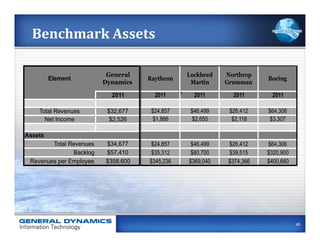

Benchmark

Assets

General Lockheed Northrop

Element Raytheon Boeing

Dynamics Martin Grumman

2011 2011 2011 2011 2011

Total Revenues $32,677 $24,857 $46,499 $26,412 $64,306

Net Income $2,526 $1,866 $2,655 $2,118 $3,307

Assets

Total Revenues $34,677 $24,857 $46,499 $26,412 $64,306

Backlog $57,410 $35,312 $80,700 $39,515 $320,900

Revenues per Employee $358,600 $345,236 $369,040 $374,366 $400,660

45

Asset Review

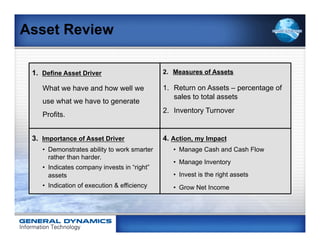

1.Define Asset Driver 2. Measures of Assets

What we have and how well we 1. Return on Assets – percentage of

sales to total assets

use what we have to generate

2. Inventory Turnover

Profits.

3. Importance of Asset Driver 4. Action, my Impact

• Demonstrates ability to work smarter • Manage Cash and Cash Flow

rather than harder.

• Manage Inventory

• Indicates company invests in “right”

assets • Invest is the right assets

• Indication of execution & efficiency • Grow Net Income

48.

How PMs impactAssets/People?

• Remember ASSETS are employees:

• Communicate with your people

– 2-way communications

– Goal setting and performance expectations

• Take care of problems early and quickly

• Build / encourage loyalty to GDIT

– Lead by example

• Provide career development opportunities

– Train your employees to add value

– Encourage degrees, certificates, clearances to make people more valuable

48

49.

Individual Activity (Page 15)

Write down one action you are committed to take

to positively impact People.

• Remember ASSETS are employees:

• Communicate with your people

– 2-way communications

– Goal setting and performance expectations

• Take care of problems early and quickly

• Build / encourage loyalty to GDIT

– Lead by example

• Provide career development opportunities

– Train your employees to add value

– Encourage degrees, certificates,

clearances to make people more valuable

49

50.

Growth

Why is Growth so

Cash important to business?

On Hand

Generation

Growth People Profit

Top Line Employees Revenues

Bottom Line Customers Expenses

Assets

Strength

Utilization

15

51.

Growth

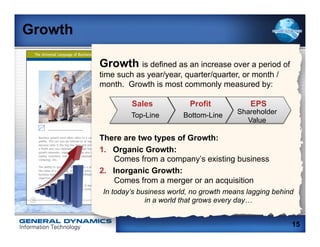

Growth is defined as an increase over a period of

time such as year/year, quarter/quarter, or month /

month. Growth is most commonly measured by:

Sales Profit EPS

Top-Line Bottom-Line Shareholder

Value

There are two types of Growth:

1. Organic Growth:

Comes from a company’s existing business

2. Inorganic Growth:

Comes from a merger or an acquisition

In today’s business world, no growth means lagging behind

in a world that grows every day…

15

52.

Growth

Intoday’s business world, no growth means

lagging behind in a world that grows every

day…

• Investors expect it.

• Employees are more energized by it.

• Customers are generally attracted to it.

• Executives are measured by it.

53.

Business Development isthe Life Blood of

an Organization/Company

ü Why?

• Programs end

• GD expects growth in both EBIT and Revenue

dollars

ü There are three ways to obtain growth

• Acquisition of a company

• Organic - grow your existing program by adding

revenue through a change order or ECP or winning

a task order

• New Business - winning a new contract

54.

There are threetypes of growth

Acquisition, Organic or New Business

In Organic Growth

54

55.

How do Iimpact Organic Growth?

• Listen to your customers

– What keeps your customer up at night

– How can we improve the mission

– Will innovation improve the process or output

• Performance leads to organic growth and

demonstrates capability to perform new

business through past/present performance

Listen and Deliver

55

56.

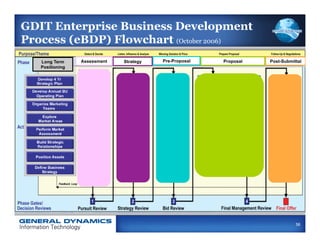

GDIT Enterprise BusinessDevelopment

Process (eBDP) Flowchart (October 2006)

Long Term Assessment Strategy Pre-Proposal Proposal Post-Submittal

Positioning

56

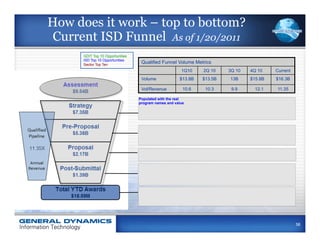

How does itwork – top to bottom?

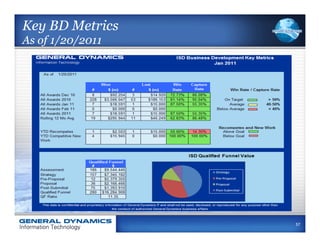

Current ISD Funnel As of 1/20/2011

GDIT Top 10 Opportunities

ISD Top 10 Opportunities

Sector Top Ten

Qualified Funnel Volume Metrics

1Q10 2Q 10 3Q 10 4Q 10 Current

Volume $13.8B $13.5B 13B $15.8B $16.3B

Vol/Revenue 10.6 10.3 9.9 12.1 11.35

Populated with the real

program names and value

58

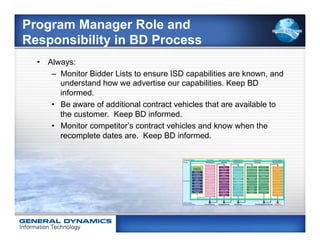

Program Manager Roleand

Responsibility in BD Process

• Always:

– Monitor Bidder Lists to ensure ISD capabilities are known, and

understand how we advertise our capabilities. Keep BD

informed.

• Be aware of additional contract vehicles that are available to

the customer. Keep BD informed.

• Monitor competitor’s contract vehicles and know when the

recomplete dates are. Keep BD informed.

61.

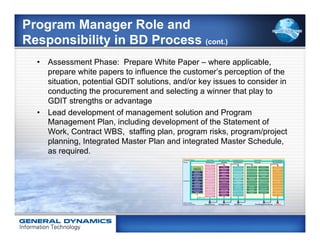

Program Manager Roleand

Responsibility in BD Process (cont.)

• Assessment Phase: Prepare White Paper – where applicable,

prepare white papers to influence the customer’s perception of the

situation, potential GDIT solutions, and/or key issues to consider in

conducting the procurement and selecting a winner that play to

GDIT strengths or advantage

• Lead development of management solution and Program

Management Plan, including development of the Statement of

Work, Contract WBS, staffing plan, program risks, program/project

planning, Integrated Master Plan and integrated Master Schedule,

as required.

62.

Program Manager Roleand

Responsibility in BD Process (cont.)

• Supports the Capture and Proposal Managers in understanding

customer requirements and designing a winning management

solution, driven by the win strategy

• Lead all Key Personnel in the development, rehearsal and delivery

of required Oral Proposal Presentations

• Post Submittal Phase:

Transition to Startup

Manages the program once it is won.

63.

Decline vs. Growth

Business in Business in

Rapid Decline Growth Mode

• Best & brightest leave first • Attracts/Retains the best & brightest!

• Productivity goes down • Productivity goes up = more profit =

• Morale goes down more cash = more ability to grow!

• Costs are cut, which limits ability to grow, • Morale is typically higher.

and the company becomes less • You have the ability to grow in your

profitable. career!

15

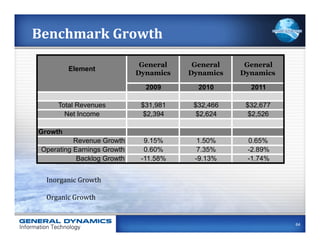

64.

Benchmark

Growth

General General General

Element

Dynamics Dynamics Dynamics

2009 2010 2011

Total Revenues $31,981 $32,466 $32,677

How do we compare?

Net Income $2,394 $2,624 $2,526

Growth

Revenue Growth 9.15% 1.50% 0.65%

Operating Earnings Growth 0.60% 7.35% -2.89%

Backlog Growth -11.58% -9.13% -1.74%

Inorganic

Growth

Organic

Growth

64

65.

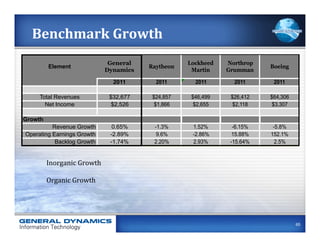

Benchmark

Growth

General Lockheed Northrop

Element Raytheon Boeing

Dynamics Martin Grumman

2011 2011 2011 2011 2011

Total Revenues $32,677 $24,857 $46,499 $26,412 $64,306

Net Income $2,526 $1,866 $2,655 $2,118 $3,307

How do we compare?

Growth

Revenue Growth 0.65% -1.3% 1.52% -6.15% -5.8%

Operating Earnings Growth -2.89% 9.6% -2.86% 15.88% 152.1%

Backlog Growth -1.74% 2.20% 2.93% -15.64% 2.5%

Inorganic

Growth

Organic

Growth

65

66.

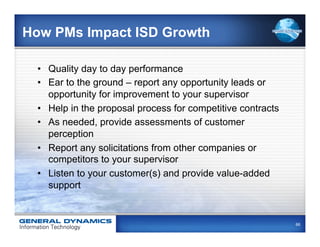

How PMs ImpactISD Growth

• Quality day to day performance

• Ear to the ground – report any opportunity leads or

opportunity for improvement to your supervisor

• Help in the proposal process for competitive contracts

• As needed, provide assessments of customer

perception

• Report any solicitations from other companies or

competitors to your supervisor

• Listen to your customer(s) and provide value-added

support

66

67.

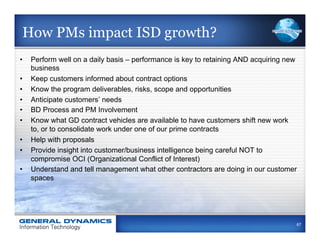

How PMs impactISD growth?

• Perform well on a daily basis – performance is key to retaining AND acquiring new

business

• Keep customers informed about contract options

• Know the program deliverables, risks, scope and opportunities

• Anticipate customers’ needs

• BD Process and PM Involvement

• Know what GD contract vehicles are available to have customers shift new work

to, or to consolidate work under one of our prime contracts

• Help with proposals

• Provide insight into customer/business intelligence being careful NOT to

compromise OCI (Organizational Conflict of Interest)

• Understand and tell management what other contractors are doing in our customer

spaces

67

Growth Review

1.Define Growth Driver 2. Measures of Growth

The ability to increase year 1. Revenue Growth

over year, quarter over quarter, 2. Net Income Growth

and/or month over month.

3. Customer Growth

3. Importance of Growth Driver 4. Action, my Impact

“Investors expect it, employees are • Grow revenue

energized by it, customers are • Bundle products/services

generally attracted to it and

executives are measured by it.” • Understand client objectives

• Solutions based

15

70.

People/Customers

Customers and employees are

Cash the key to driving profitable

On Hand

Generation

& sustainable growth.

Growth People Profit

Top Line Customers Revenues

Bottom Line Employees Expenses

Assets

Strength

Utilization

17

71.

People

People are the external customers, internal

customers, as well as in-direct influences such as

affiliates, vendors, partners, and suppliers.

Without People…then what happens?

17

72.

People

“Culture eats strategy for breakfast!”

~Peter Drucker

17

73.

Internal People

A’shire A+’s and B’s hire C’s

What is the #1 reason a person

will leave a company?

17

74.

Internal/External Customers

Listening to our Customers:

External Customers:

• Have a formal process for listening to your customers

• Anticipating customer needs is critical!

• We must understand their business, and the customers they serve.

Internal Customers:

• Meet with them monthly and ask:

• “Are there any gaps in my performance?

• Have my priorities changed?”

17

75.

External People

“If Iwould have asked

my customers what

they wanted, they

would have told me a

faster horse!”

Henry Ford

17

76.

Anticipating External People

What companies have failed to anticipate customer

expectations? What were the results?

What limits companies from anticipating their

customers’ wants and needs?

17

77.

Listen to yourcustomers!

The #1 reason for rework or

losing an opportunity is

not listening to your customer.

BD Process and Program Manager Involvement

January 2011

77

78.

People Review

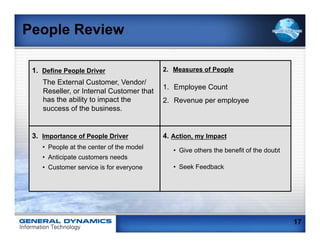

1.Define People Driver 2. Measures of People

The External Customer, Vendor/

1. Employee Count

Reseller, or Internal Customer that

has the ability to impact the 2. Revenue per employee

success of the business.

3. Importance of People Driver 4. Action, my Impact

• People at the center of the model • Give others the benefit of the doubt

• Anticipate customers needs

• Customer service is for everyone • Seek Feedback

17

79.

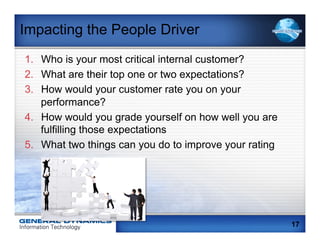

Impacting the PeopleDriver

1. Who is your most critical internal customer?

2. What are their top one or two expectations?

3. How would your customer rate you on your

performance?

4. How would you grade yourself on how well you are

fulfilling those expectations

5. What two things can you do to improve your rating

17

80.

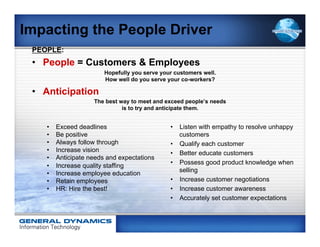

Impacting the PeopleDriver

PEOPLE:

• People = Customers & Employees

Hopefully you serve your customers well.

How well do you serve your co-workers?

• Anticipation

The best way to meet and exceed people’s needs

is to try and anticipate them.

• Exceed deadlines • Listen with empathy to resolve unhappy

• Be positive customers

• Always follow through • Qualify each customer

• Increase vision • Better educate customers

• Anticipate needs and expectations

• Possess good product knowledge when

• Increase quality staffing

selling

• Increase employee education

• Retain employees • Increase customer negotiations

• HR: Hire the best! • Increase customer awareness

• Accurately set customer expectations

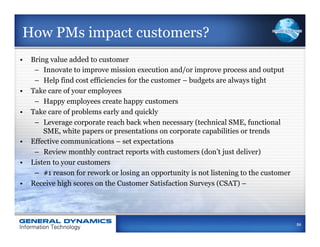

How PMs impactcustomers?

• Bring value added to customer

– Innovate to improve mission execution and/or improve process and output

– Help find cost efficiencies for the customer – budgets are always tight

• Take care of your employees

– Happy employees create happy customers

• Take care of problems early and quickly

– Leverage corporate reach back when necessary (technical SME, functional

SME, white papers or presentations on corporate capabilities or trends

• Effective communications – set expectations

– Review monthly contract reports with customers (don’t just deliver)

• Listen to your customers

– #1 reason for rework or losing an opportunity is not listening to the customer

• Receive high scores on the Customer Satisfaction Surveys (CSAT) –

84

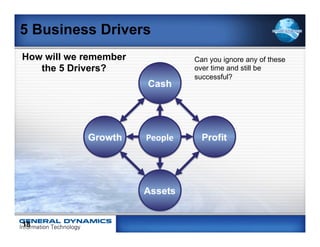

5 Business Drivers

Howwill we remember Can you ignore any of these

the 5 Drivers? over time and still be

successful?

18

87.

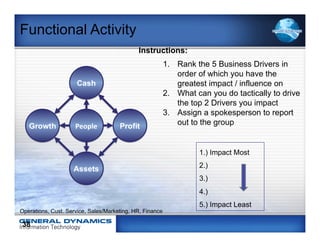

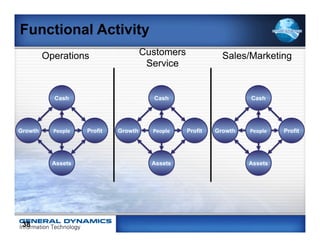

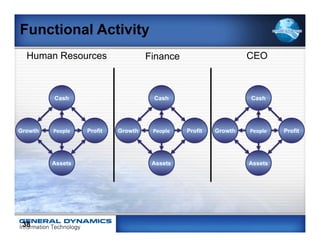

Functional Activity

Instructions:

1. Rank the 5 Business Drivers in

order of which you have the

greatest impact / influence on

2. What can you do tactically to drive

the top 2 Drivers you impact

3. Assign a spokesperson to report

out to the group

1.) Impact Most

2.)

3.)

4.)

5.) Impact Least

Operations, Cust. Service, Sales/Marketing, HR, Finance

38

Preparation for Tomorrow

1. Come ready to teach one of the 5 Drivers to your

group

2. Come ready to learn and teach all three financial

statements

3. We will be doing analysis on one of the

competitor/benchmark entities….choose which

one you would like to analyze (Boeing, Raytheon,

Northrop Grumman, Lockheed Martin)

Day 1 Quiz

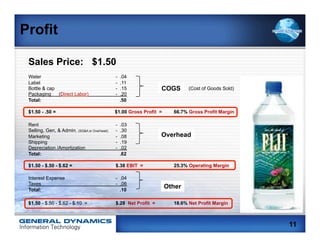

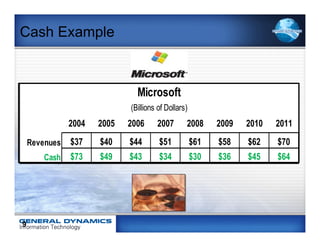

Cash Example

Microsoft CEO defends cash 'problem'

Steve Ballmer says… “the company

would rather have too much cash on

hand rather than return it to

shareholders”.

May 31, 2008 CNN Money

9

95.

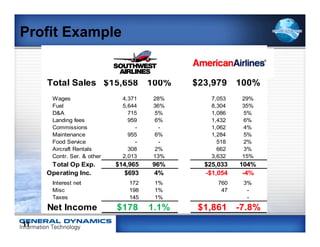

Profit Example

Company A Company B

2011 2011

Total Sales $15,658 100% $23,979 100%

Wages 4,371 28% 7,053 29%

Fuel 5,644 36% 8,304 35%

D&A 715 5% 1,086 5%

Landing fees 959 6% 1,432 6%

Commissions - - 1,062 4%

Maintenance 955 6% 1,284 5%

Food Service - - 518 2%

Aircraft Rentals 308 2% 662 3%

Contr. Ser. & other 2,013 13% 3,632 15%

Total Op Exp. $14,965 96% $25,033 104%

Operating Inc. $693 4% -$1,054 -4%

Interest net 172 1% 760 3%

Misc 198 1% 47 -

Taxes 145 1% -

Net Income $178 1.1% $1,861 -7.8%

11

96.

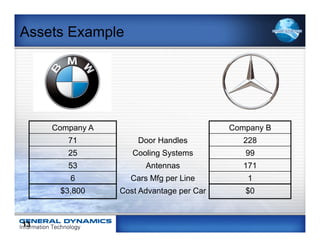

Assets Example

Company A Company B

71 Door Handles 228

25 Cooling Systems 99

53 Antennas 171

6 Cars Mfg per Line 1

$3,800 Cost Advantage per Car $0

13

People Example

When you think of a

company with

great customer service,

who comes to mind?

17

99.

Review and Teach

For your assigned Driver: (Study Notes 4-5 minutes)

1. Define & give examples. How is it measured?

2. Importance & relationship to other Drivers?

3. How did we do in 2011? Future goals or targets?

4. How you plan to influence this driver?

Be sure to explain:

CASH: Cash & Cash Flow—Both Cash and Cash Flow are important for different

reasons

PROFIT: How to calculate? Gross Margin, Operating Margin, and Net Profit

ASSETS: Strength & Utilization—balance is critical here

GROWTH: Organic & Inorganic—where have we grown?

PEOPLE: Internal & external Customers; meeting, exceeding & anticipating

needs & expectations

30

100.

Demystifying the AnnualReport

What is the Purpose of the Annual Report?

ü General Communication

GENERAL DYNAMICS Ø Shareholders, existing/potential investors

(others?)

Annual Report 2011

Ø Important, numbers, decision and strategy

Ø Where we have been and where we are

going

ü Marketing

Ø The what, who and how

Ø Name, Image & Branding

Ø Colors

ü Compliance

Ø GAAP

Ø SEC

36

101.

Executive Communication

• FinancialHi-lights

• To Our Shareholders GENERAL DYNAMICS

Annual Report 2011

• Strategic Overview

• Financial Statement

• Income Statement

• Balance Sheet

• Statement of Cash Flows

• Notes to the Financial Section

36 22

102.

Executive Communication

• What are the top 2 Drivers

getting focus from the

Executives right now?

• What are the key messages?

• What are the initiatives or

strategies for 2012?

• How do we plan to execute on

those strategies?

48

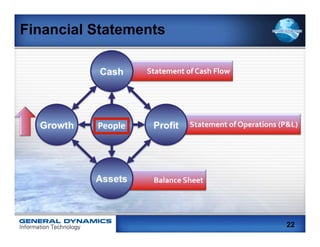

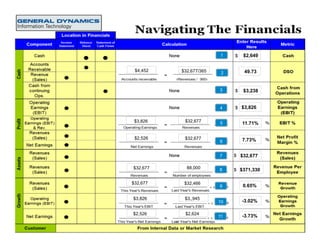

Financial Statements

Statement

of

Cash

Flow

Statement

of

Operations

(P&L)

Balance

Sheet

22

105.

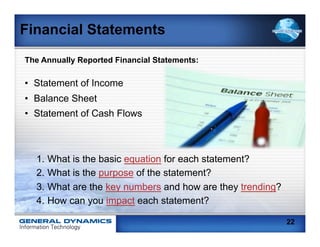

Financial Statements

The AnnuallyReported Financial Statements:

• Statement of Income

• Balance Sheet

• Statement of Cash Flows

1. What is the basic equation for each statement?

2. What is the purpose of the statement?

3. What are the key numbers and how are they trending?

4. How can you impact each statement?

22

106.

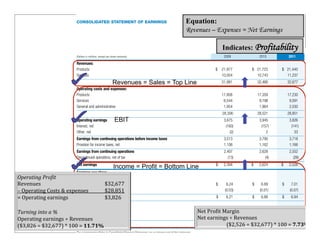

ITEM 8. FINANCIALSTATEMENTS AND SUPPLEMENTARY DATA

CONSOLIDATED STATEMENT OF EARNINGS Equation:

Revenues – Expenses = Net Earnings

Income

Statement

Indicates: Profitability

Y e ar E nd e d D ec e m b e r 3 1

(Dollars in millions, except per-share amounts) 2009 2010 2011

Revenues:

Products $ 21,977 $ 21,723 $ 21,440

Services 10,004 10,743 11,237

Revenues = Sales = Top Line 31,981 32,466 32,677

Operating costs and expenses:

Products 17,808 17,359 17,230

Services 8,544 9,198 9,591

General and administrative 1,954 1,964 2,030

28,306 28,521 28,851

Operating earnings EBIT 3,675 3,945 3,826

Interest, net (160) (157) (141)

Other, net (2) 2 33

Earnings from continuing operations before income taxes 3,513 3,790 3,718

Provision for income taxes, net 1,106 1,162 1,166

Earnings from continuing operations 2,407 2,628 2,552

Discontinued operations, net of tax (13) (4) (26)

Net earnings $ 2,394 $ 2,624 $ 2,526

Income = Profit = Bottom Line

Earnings per share

Operating

Pro:it

Basic:

Revenues

operations

Continuing

$32,677

$ 6.24 $ 6.89 $ 7.01

–

Operating

Costs

&

expenses Discontinued operations

$28,851

(0.03) (0.01) (0.07)

=

Operating

earnings

Net

earnings

$3,826

$ 6.21 $ 6.88 $ 6.94

Diluted:

Turning

into

a

%

Continuing operations Net

Pro;it

M6.20

$ argin

$ 6.82 $ 6.94

Discontinued operations (0.03)Revenues

(0.01)

Net

earnings

÷

(0.07)

Operating

earnings

÷

Revenues

Net earnings

($3,826

÷

$32,677)

*

100

=

11.71%

$

6.17

($2,526

÷

$32,677)

*

100

=6.87

$ 6.81 $

7.73%

106

The accompanying Notes to Consolidated Financial Statements are an integral part of this statement.

107.

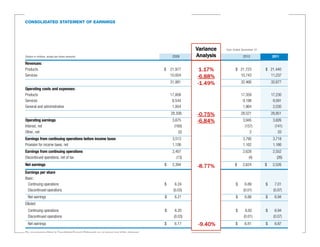

ITEM 8. FINANCIALSTATEMENTS AND SUPPLEMENTARY DATA

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

CONSOLIDATED STATEMENT OF EARNINGS OF EARNINGS

CONSOLIDATED STATEMENT

Variance

Year Ended December 31 Year Ended December 31

(Dollars in millions, except per-share amounts)

(Dollars in millions, except per-share amounts) 2009 Analysis

2009

2010 2011

2010 2011

Revenues: Revenues:

Products Products $ 21,977 1.17%

$$ 21,977

21,723 $ 21,440

$ 21,723 $ 21,440

Services Services 10,004 10,004

10,743

-6.88% 11,237

10,743 11,237

31,981 31,981

32,466

-1.49% 32,677

32,466 32,677

Operating costs and expenses: costs and expenses:

Operating

Products Products 17,808 17,808

17,359 17,230

17,359 17,230

Services Services 8,544 8,544

9,198 9,591

9,198 9,591

General and administrative

General and administrative 1,954 1,954

1,964 2,030

1,964 2,030

28,306 -0.75%6

28,30

28,521 28,851

28,521 28,851

Operating earnings Operating earnings 3,675 -6.84%

3,675

3,945 3,826

3,945 3,826

Interest, net Interest, net (160) (160)

(157) (141)

(157) (141)

Other, net Other, net (2) (2)

2 33 2 33

Earnings from continuing operations continuing operations before income taxes

Earnings from before income taxes 3,513 3,513

3,790 3,718

3,790 3,718

Provision for income taxes, net for income taxes, net

Provision 1,106 1,106

1,162 1,166

1,162 1,166

Earnings from continuing operations continuing operations

Earnings from 2,407 2,407

2,628 2,552

2,628 2,552

Discontinued operations, Discontinued operations, net of tax

net of tax (13) (13)

(4) (26) (4) (26)

Net earnings Net earnings $ 2,394 $ 2,394

$ 2,624

-8.77% $ $ 2,526

2,624 $ 2,526

Earnings per share Earnings per share

Basic: Basic:

Continuing operations Continuing operations $ 6.24 $$ 6.89

6.24 $ $ 7.016.89 $ 7.01

Discontinued operations Discontinued operations (0.03) (0.01)

(0.03) (0.07)

(0.01) (0.07)

Net earnings Net earnings $ 6.21 $$ 6.88

6.21 $ $ 6.94

6.88 $ 6.94

Diluted: Diluted:

Continuing operations Continuing operations $ 6.20 $$ 6.20

6.82 $ $ 6.946.82 $ 6.94

Discontinued operations Discontinued operations (0.03) (0.01)

(0.03) (0.07)

(0.01) (0.07)

Net earnings Net earnings $ 6.17 -9.40%

$$ 6.81

6.17 $ $ 6.87

6.81 $ 6.87

The accompanying Notes to Consolidated FinancialNotes to Consolidated Financial Statements are an integral part of this statement.

The accompanying Statements are an integral part of this statement.

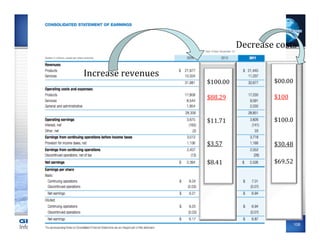

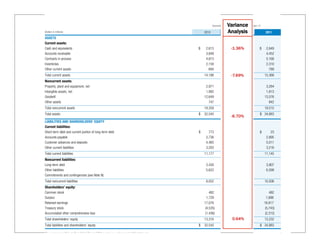

CONSOLIDATED BALANCE SHEET

Equation: Indicates: Financial Strength

Assets = Liabilities + Shareholder Equity December 31

Balance

Sheet

Most Liquid

(Dollars in millions)

ASSETS

Current assets:

2010 2011

Cash and equivalents $ 2,613 $ 2,649

Accounts receivable 3,848 4,452

Contracts in process 4,873 5,168

Inventories 2,158 2,310

Other current assets 694 789

Total current assets

Becomes Cash < Year 14,186 15,368

Noncurrent assets:

Property, plant and equipment, net 2,971 3,284

Intangible assets, net Current Ratio: 1,992 1,813

Goodwill 12,649 13,576

Least Liquid Other assets 747 842

Total noncurrent assets Current Assets/Current Liabilities 18,359 19,515

Total assets = Current Ratio $ 32,545 $ 34,883

LIABILITIES AND SHAREHOLDERS’ EQUITY

Current liabilities:

Due First 15,368 / 11,145

Short-term debt and current portion of long-term debt $ 773 $ 23

Accounts payable = 1.38 2,736 2,895

Customer advances and deposits 4,465 5,011

Other current liabilities 3,203 3,216

Total current liabilities Due in < 1 Year 11,177 11,145

Noncurrent liabilities:

Long-term debt 2,430 3,907

Other liabilities Equity Ratio: 5,622 6,599

Due Last Commitments and contingencies (see Note N)

Total noncurrent liabilities 8,052 10,506

Shareholder Equity/Total Assets

Shareholders’ equity:

Common stock = Equity Ratio 482 482

Surplus 1,729 1,888

Retained earnings 17,076 18,917

Treasury stock 13,232 / 34,883 (4,535) (5,743)

Accumulated other comprehensive loss = .38 X 100 = 38% Equity (1,436) (2,312)

Total shareholders’ equity 13,316 13,232

109

Total liabilities and shareholders’ equity $ 32,545 $ 34,883

The accompanying Notes to Consolidated Financial Statements are an integral part of this statement.

110.

CONSOLIDATED BALANCE SHEETBALANCE SHEET

CONSOLIDATED

December 31 Variance e c e m b e r 3 1

D

(Dollars in millions) (Dollars in millions) 2010 Analysis

2011 2010 2011

ASSETS ASSETS

Current assets: Current assets:

Cash and equivalents Cash and equivalents $ 2,613 $ -1.36%

2,649 2,613

$ $ 2,649

Accounts receivable Accounts receivable 3,848 4,452 3,848 4,452

Contracts in process Contracts in process 4,873 5,168 4,873 5,168

Inventories Inventories 2,158 2,310 2,158 2,310

Other current assets Other current assets 694 789 694 789

Total current assets Total current assets 14,186 -7.69%

15,368

14,186 15,368

Noncurrent assets: Noncurrent assets:

Property, plant and equipment, net plant and equipment, net

Property, 2,971 3,284 2,971 3,284

Intangible assets, net Intangible assets, net 1,992 1,813 1,992 1,813

Goodwill Goodwill 12,649 13,576

12,649 13,576

Other assets Other assets 747 842 747 842

Total noncurrent assets Total noncurrent assets 18,359 19,515

18,359 19,515

Total assets Total assets $ 32,545 $ 34,883

$ 32,545 $ 34,883

-6.70%

LIABILITIES AND SHAREHOLDERS’ EQUITY

LIABILITIES AND SHAREHOLDERS’ EQUITY

Current liabilities: Current liabilities:

Short-term debt and current portion ofdebt and current portion of long-term debt

Short-term long-term debt $ 773 $ $ 23 773 $ 23

Accounts payable Accounts payable 2,736 2,895 2,736 2,895

Customer advances and deposits advances and deposits

Customer 4,465 5,011 4,465 5,011

Other current liabilities Other current liabilities 3,203 3,216 3,203 3,216

Total current liabilities Total current liabilities 11,177 11,145

11,177 11,145

Noncurrent liabilities: Noncurrent liabilities:

Long-term debt Long-term debt 2,430 3,907 2,430 3,907

Other liabilities Other liabilities 5,622 6,599 5,622 6,599

Commitments and contingencies (see Note N)contingencies (see Note N)

Commitments and

Total noncurrent liabilities Total noncurrent liabilities 8,052 10,506 8,052 10,506

Shareholders’ equity: Shareholders’ equity:

Common stock Common stock 482 482 482 482

Surplus Surplus 1,729 1,888 1,729 1,888

Retained earnings Retained earnings 17,076 18,91717,076 18,917

Treasury stock Treasury stock (4,535) (5,743)

(4,535) (5,743)

Accumulated other comprehensive loss other comprehensive loss

Accumulated (1,436) (2,312)

(1,436) (2,312)

Total shareholders’ equity Total shareholders’ equity 13,316 0.64%

13,232

13,316 13,232

Total liabilities and shareholders’liabilities and shareholders’ equity

Total equity $ 32,545 $ 34,883

$ 32,545 $ 34,883

The accompanying Notes to Consolidated Financial Statements are an integral part ofStatements are an integral part of this statement.

The accompanying Notes to Consolidated Financial this statement.

111.

Three Reasons whyGD has a strong

Balance Sheet!

1. Plenty of Cash – Not enough?

2. Good Trends

§ Revenues up

§ Assets up

§ Liabilities “down” - flat

3. Equity Position – 35.4% plus

($13,232/$34,883 = 37.93%)

111

112.

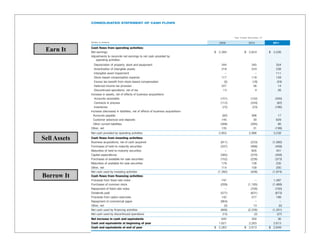

CONSOLIDATED STATEMENT OFCASH FLOWS

Year Ended December 31

(Dollars in millions) 2009 2010 2011

Earn It Cash flows from operating activities:

Net earnings $ 2,394 $ 2,624 $ 2,526

Adjustments to reconcile net earnings to net cash provided by

operating activities-

Depreciation of property, plant and equipment 344 345 354

Amortization of intangible assets 218 224 238

Intangible asset impairment – – 111

Stock-based compensation expense 117 118 128

Excess tax benefit from stock-based compensation (5) (18) (24)

Deferred income tax provision 227 56 14

Discontinued operations, net of tax 13 4 26

Increase in assets, net of effects of business acquisitions-

Accounts receivable (151) (152) (420)

Contracts in process (112) (334) (62)

Inventories (72) (23) (186)

Increase (decrease) in liabilities, net of effects of business acquisitions-

Accounts payable (92) 366 17

Customer advances and deposits 145 30 629

Other current liabilities (306) (285) 86

Other, net 135 31 (199)

Net cash provided by operating activities 2,855 2,986 3,238

Sell Assets Cash flows from investing activities:

Business acquisitions, net of cash acquired (811) (233) (1,560)

Purchases of held-to-maturity securities (337) (468) (459)

Maturities of held-to-maturity securities – 605 441

Capital expenditures (385) (370) (458)

Purchases of available-for-sale securities (152) (226) (373)

Maturities of available-for-sale securities 179 126 235

Other, net 114 158 200

Net cash used by investing activities (1,392) (408) (1,974)

Borrow It Cash flows from financing activities:

Proceeds from fixed-rate notes 747 – 1,497

Purchases of common stock (209) (1,185) (1,468)

Repayment of fixed-rate notes – (700) (750)

Dividends paid (577) (631) (673)

Proceeds from option exercises 142 277 198

Repayment of commercial paper (904) – –

Other, net (5) 13 (5)

Net cash used by financing activities (806) (2,226) (1,201)

Net cash used by discontinued operations (15) (2) (27)

Net increase in cash and equivalents 642 350 36

Cash and equivalents at beginning of year 1,621 2,263 2,613

Cash and equivalents at end of year $ 2,263 $ 2,613 $ 2,649

The accompanying Notes to Consolidated Financial Statements are an integral part of this statement.

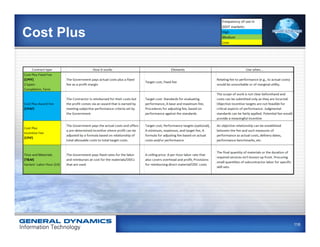

PMR Summary Contract Value =

Complete dollar value of the Contract

Total Contract Funding =

Contracts are funded incrementally. This

number reflects the portion of the contract

that has or is currently funded

Funding Remaining =

The contract funding minus the amount

billed/paid

Date to fund Expiration

Contract Type Date the funds expire

• Cost Plus

• Award Fee

• Level of Effort

• Fixed Cost

120

121.

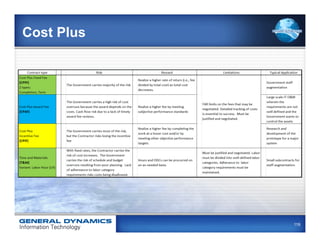

PMR Summary

Target LOE- EAC =

Level of Effort Estimate And Complete

Min & Max LOE – EAC =

There is a minimum and a maximum associated

with each contract. Going above or below these

levels results in a fine

LOE Expended =

Hours complete on the project

EAC Profit %

Determined prior to contract

Booked Profit rate = Target profit

121

122.

External Factors

How does the situation affect:

People Cash

Growth Profit

Assets

Heads Up!

40

123.

“The best wayto predict the future….

is to create it.”

Peter Drucker

123

124.

External Factors

The best “CEO’s” not only pay attention

to what is happening inside their

company, they also have an eye on

the external factors that could impact

their business.

40

125.

External Factors

The Role of the Stock Market

1. What role does the stock market play?

2. Who cares about a company’s stock price and why?

• Investors

• Analysis

• The CEO

• Employees

3. What are the benefits of a higher stock price?

40 40

Competitor Reports Activity

Resources

1. Annual Report and/or latest executive

messaging

2. Financial Statements

3. Complete the Navigating the Financials

4. Corporate Website

5. www.google.com/finance

Reports – use outline provided

1. Answer questions on the hand-out

2. Prepare flip-chart

3. Teach the rest of the group

40

128.

Individual Action Plan

à Review: (Page 52)

What new insights did you gain,

as a result of attending?

à Action Plan: (Page 53)

List the things you can commit to do:

ü Cash: (refer to page 9)

ü Profit: (refer to page 11)

ü Assets: (refer to page 13)

ü Growth: (refer to page 15)

ü People: (refer to page 17)

52 52

129.

Acumen Accountability

Find aPartner now and:

1. Set up a specific date and time in 30 days to report

your progress on your action plan.

2. Exchange emails

3. Exchange phone numbers

4. Decide who will initiate the call

5. Determine a back-up plan

6. Transfer this information to

your device now.

53 53

130.

Insights

à Review: (Page 52)

What new insights did you gain,

as a result of attending?

52

Locating Financial Information

Web Sites:

• www.nasdaq.com

• www.reuters.com

• www.yahoo.com

• www.finance.google.com

• www.hoovers.com

• www.smartmoney.com

55 55

133.

Learning Objectives…

ü Listand describe what key measures are important

to ISD and to Tom Kirchmaier.

ü List and describe the five business drivers all successful

businesses must focus on.

ü Teach specific components of the financial statements.

ü Explain how I can have an impact on growth.

ü Create a personal action plan that can positively

impact our results.

133

134.

Post Course BusinessAcumen

1. Teach one of the principals learned in class today, to

someone on your team.

2. Discuss your action items with your manager in

the next 7 days.

3. Read the first 90 pages of: “Seeing the BIG Picture“

4. Give an account of your progress on your action

item(s).

5. Think and act like owners!

135.

One Final Thought…

“People will work

hard for a paycheck,

harder for a person, and

hardest for a reason.”