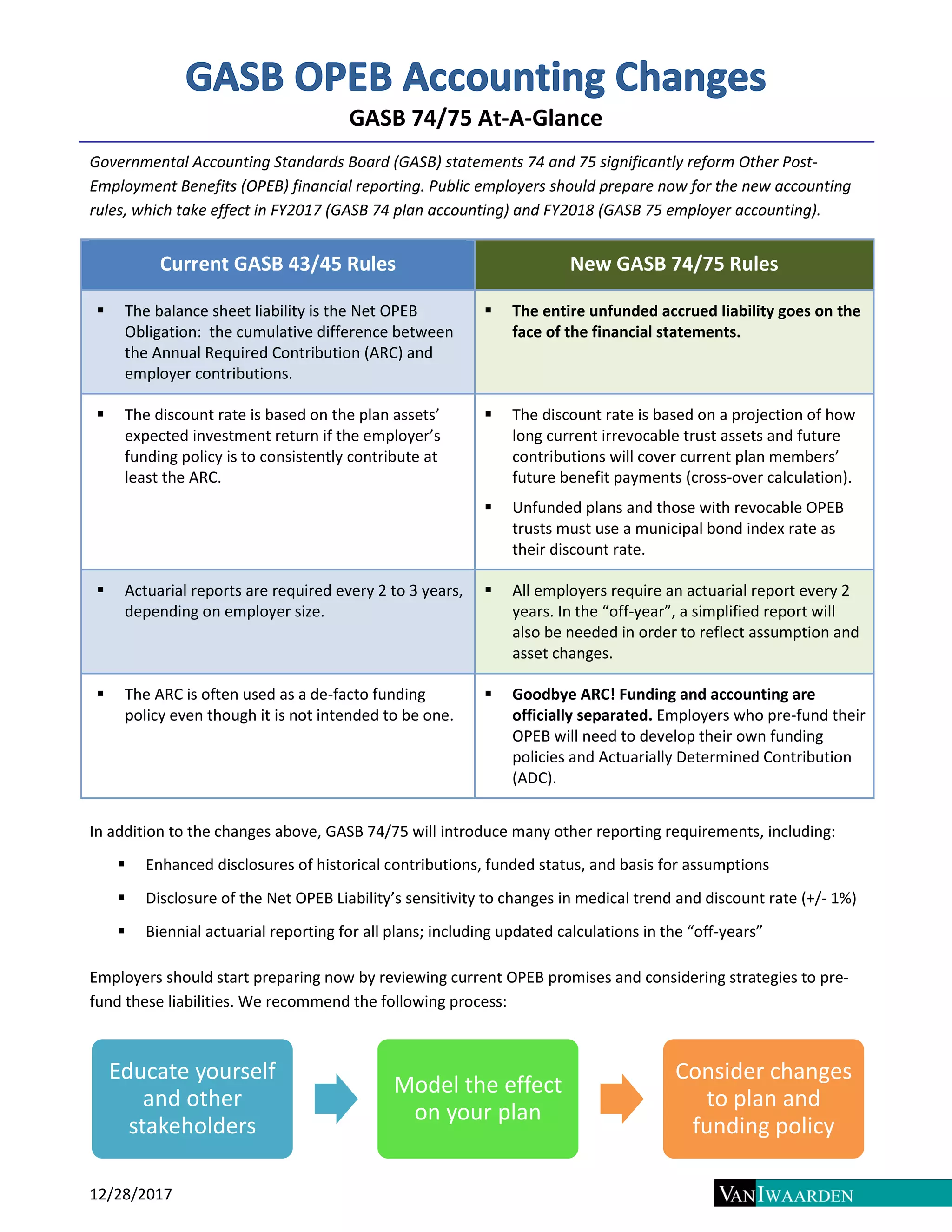

GASB Statements 74 and 75 reform OPEB financial reporting for public employers, starting in FY2017 and FY2018. Key changes include the requirement to recognize the entire unfunded accrued liability on financial statements, use a municipal bond index for discount rates for unfunded plans, and biennial actuarial reports. Employers should begin preparing by reviewing OPEB commitments and developing funding policies while accommodating new reporting requirements.