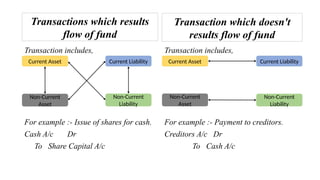

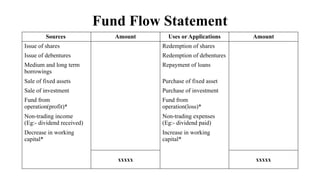

The document explains the fund flow statement, which analyzes the sources and uses of funds over a specified period, focusing on working capital. It outlines definitions of current and non-current assets and liabilities, as well as methods for preparing a fund flow statement, including the evaluation of changes in working capital and fund from operations. Examples are provided to illustrate the preparation of the fund flow statement and the necessary adjustments to accounts.

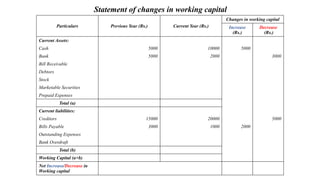

![1. Schedule of changes in working capital

The schedule of changes in working capital can be prepared by

comparing the current assets and the current liabilities of two

periods.

Rules of preparing the schedule:

I. Increase in current asset, results in [+]increase in ‘working

capital’.

II. Decrease in a current asset, , results in [-]decrease in ‘working

capital’.

III. Increase in a current liability, results [-] decrease in ‘working

capital’.

IV. Decrease in current liability, results in [+]increase in ‘working

capital’.](https://image.slidesharecdn.com/fundflowstatement-230227055844-2b0cc0a3-250129060340-4e9e2c20/85/fundflowstatement-230227055844-2b0cc0a3-pptx-9-320.jpg)

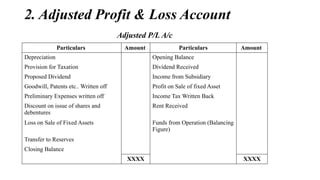

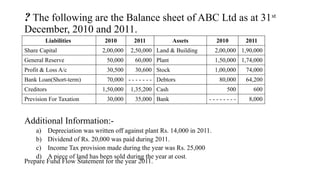

![Solution:-

* We can take it has a current lability or an non current liability. For now we treat Prevision For Taxation is a non-current liability.

Additional Information:-

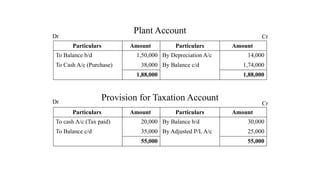

a) Depreciation was written off against plant Rs. 14,000 in 2011.[prepare ledger for plant]

b) Dividend of Rs. 20,000 was paid during 2011.[Non-trading expenses. show in the Cr side of Fund flow

statement]

c) Income Tax provision made during the year was Rs. 25,000. [prepare ledger for Prevision For Taxation ]

d) A piece of land has been sold during the year at cost.[2,00,000-1,90,000=10,000]

Liabilities 2010 2011 Assets 2010 2011

Share Capital (Non CL) 2,00,000 2,50,000 Land & Building(Non CA) 2,00,000 1,90,000

General Reserve (Non CL) 50,000 60,000 Plant (Non CA) 1,50,000 1,74,000

Profit & Loss A/c (Non CL) 30,500 30,600 Stock(CA) 1,00,000 74,000

Bank Loan(Short-term) (CL) 70,000 - - - - - - - Debtors (CA) 80,000 64,200

Creditors (CL) 1,50,000 1,35,200 Cash (CA) 500 600

Prevision For Taxation (Non

CL)*

30,000 35,000 Bank (CA) - - - - - - - - 8,000](https://image.slidesharecdn.com/fundflowstatement-230227055844-2b0cc0a3-250129060340-4e9e2c20/85/fundflowstatement-230227055844-2b0cc0a3-pptx-15-320.jpg)

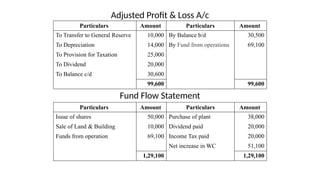

![Particulars

Previous Year [2010]

(Rs.)

Current Year [2011]

(Rs.)

Changes in working capital

Increase

(Rs.)

Decrease

(Rs.)

Current Assets:

Stock 1,00,000 74,000 26,000

Debtors 80,000 64,200 15,800

Cash 500 600 100

Bank - - - - - - 8,000 8,000

Total (a) 1,80,500 1,46,800

Current liabilities:

Bank Loan 70,000 - - - - - - 70,000

Creditors 1,50,000 1,35,200 14,800

Total (b) 2,20,000 1,35,000

Working Capital (a-b) -39,500 11,600

Net Increase/Decrease in Working capital

51,100

51,100

11,600 11,600 92,900 92,900](https://image.slidesharecdn.com/fundflowstatement-230227055844-2b0cc0a3-250129060340-4e9e2c20/85/fundflowstatement-230227055844-2b0cc0a3-pptx-16-320.jpg)