Download as PDF, PPTX

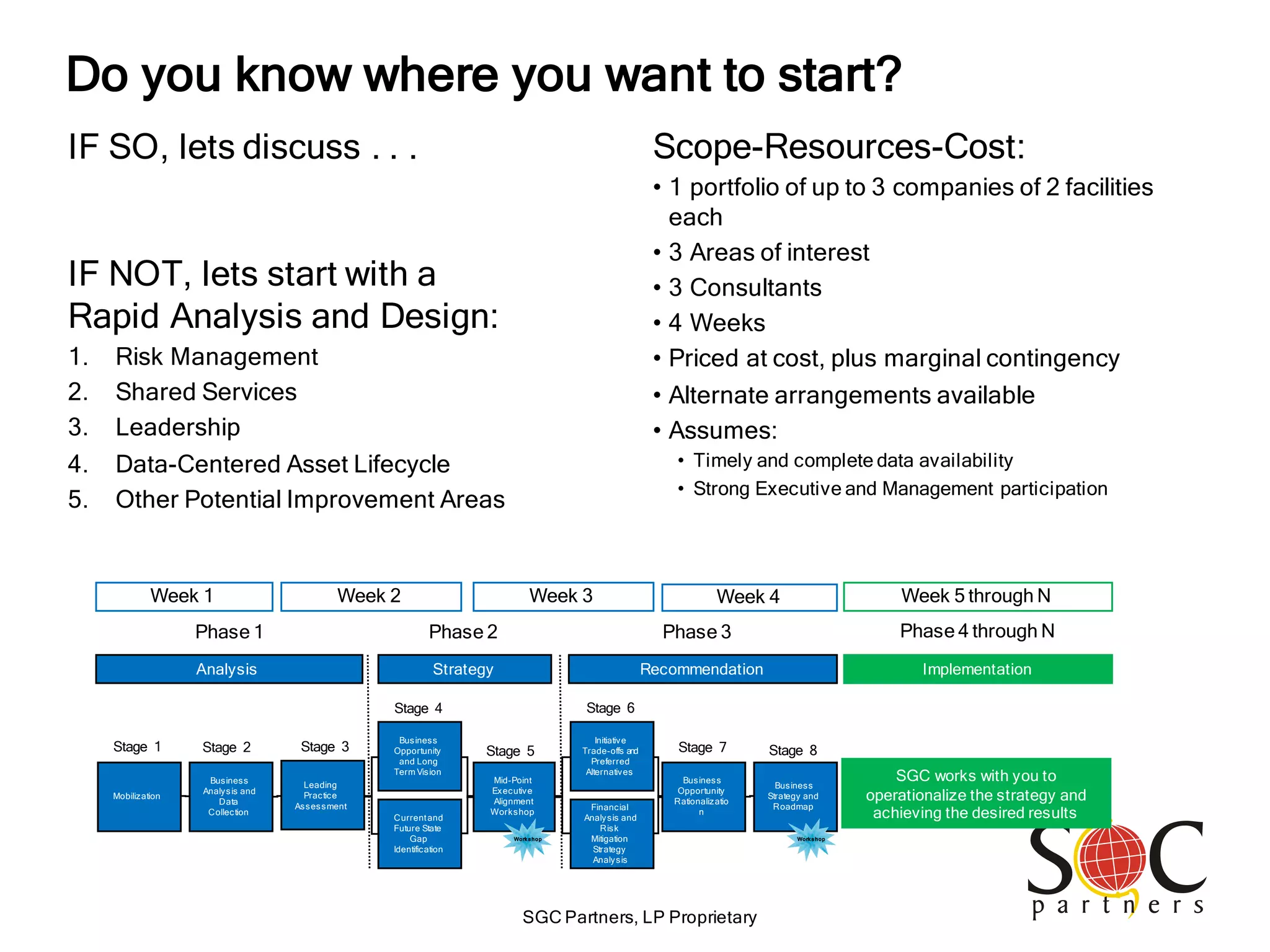

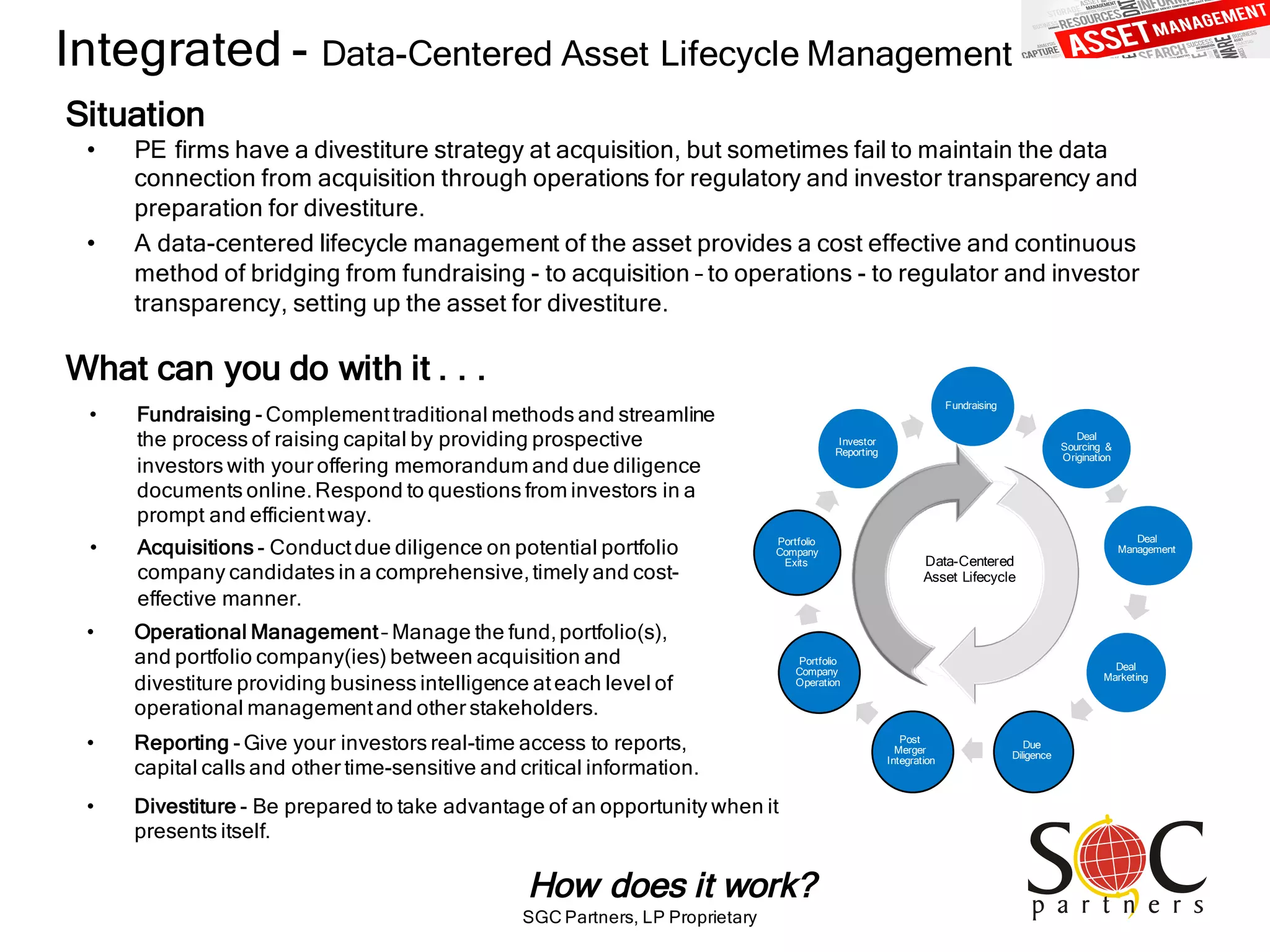

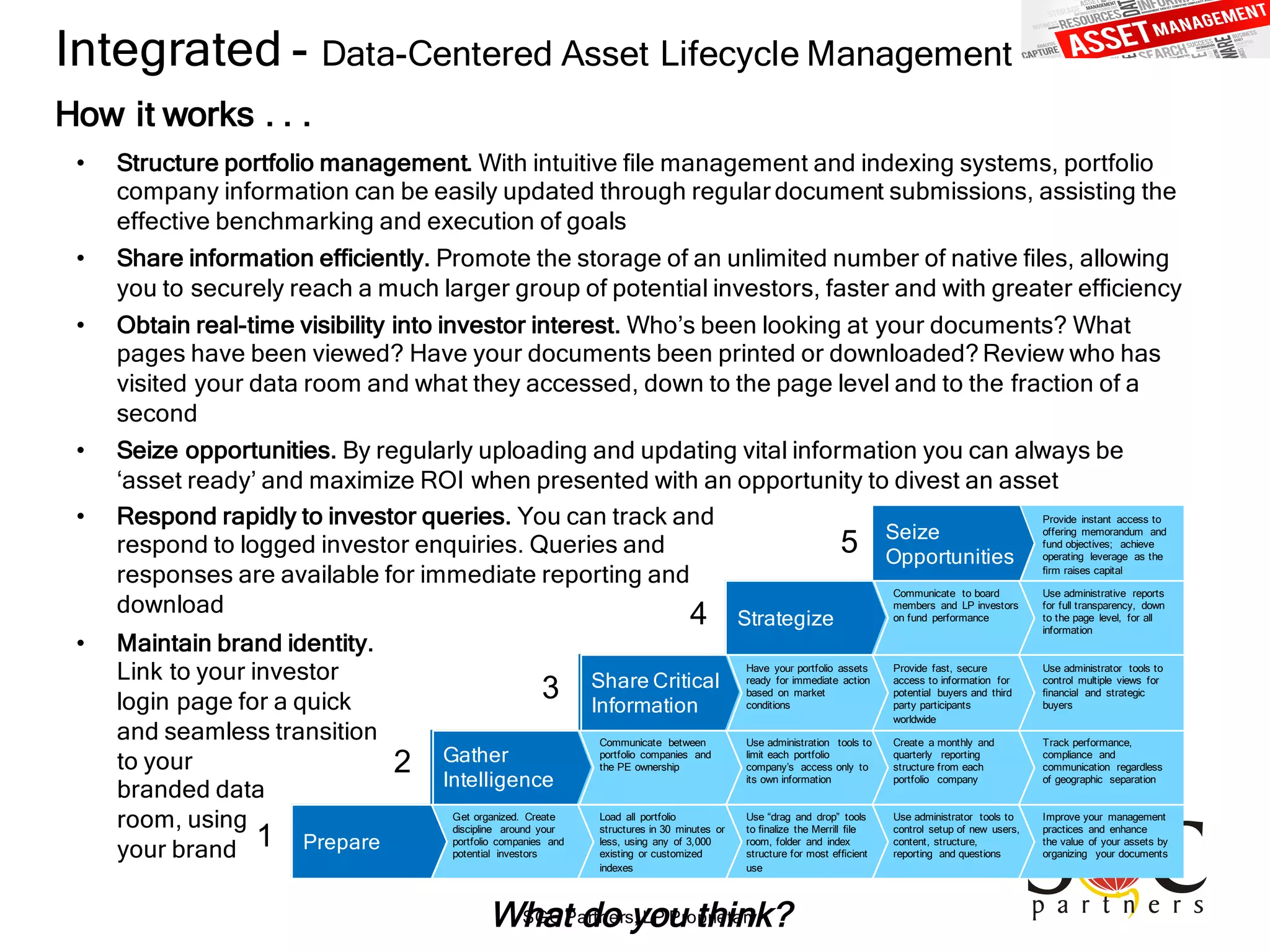

SGC Partners emphasizes the need for private equity firms to adapt to increasing transparency and regulatory demands while focusing on operational excellence to maintain competitive advantage. Key recommendations include a balanced approach to risk management, optimized leadership structures, and a data-centered asset lifecycle strategy. The document outlines major trends in 2016 affecting private equity, particularly regarding tax reform and capital availability as influenced by the presidential election.