Download as PDF, PPTX

![FRANCHISE FEE PITFALLS AND HOW

TO IDENTIFY THEM

FOCUS ON WHAT COUNTS

[ENTREPRENEURIAL]

[PROGRESSIVE]

[SOLUTIONS]](https://image.slidesharecdn.com/franchisefeepresentationforslideshare-161109193921/85/Franchise-Fee-Pitfalls-and-How-to-Identify-Them-1-320.jpg)

![FRANCHISE FEE PITFALLS AND HOW

TO IDENTIFY THEM

FOCUS ON WHAT COUNTS

[ENTREPRENEURIAL]

[PROGRESSIVE]

[SOLUTIONS]](https://image.slidesharecdn.com/franchisefeepresentationforslideshare-161109193921/75/Franchise-Fee-Pitfalls-and-How-to-Identify-Them-1-2048.jpg)

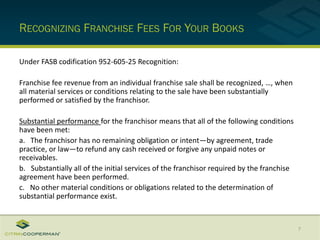

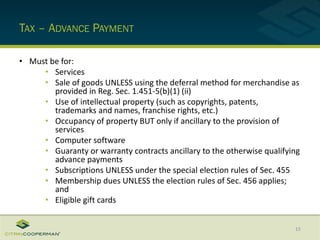

![FRANCHISE FEES (CONT’D)

5

What are initial services?

Common provision of a franchise agreement in which the franchisor usually will agree to provide a variety of services and

advice to the franchisee, such as the following:

Assistance in the selection of a site. The assistance may be based on experience with factors such as traffic patterns,

residential configurations, and competition.

Assistance in obtaining facilities, including related financing and architectural and engineering services. The facilities

may be purchased or leased by the franchisee, and lease payments may be guaranteed by the franchisor.

Assistance in advertising, either for the individual franchisee or as part of a general program.

Training of the franchisee's personnel.

Preparation and distribution of manuals and similar material concerning operations, administration, and record

keeping.

Bookkeeping and advisory services, including setting up the franchisee's records and advising the franchisee about

income, real estate, and other taxes or about local regulations affecting the franchisee's business.

Inspection, testing, and other quality control programs.

[Above from FAS 45: Accounting for Franchise Fee Revenue (as amended)]](https://image.slidesharecdn.com/franchisefeepresentationforslideshare-161109193921/85/Franchise-Fee-Pitfalls-and-How-to-Identify-Them-5-320.jpg)

The document discusses the intricacies of franchise fees, including their recognition and the related accounting and tax implications. It highlights the rules for recognizing franchise fee revenue and contrasts GAAP (Generally Accepted Accounting Principles) treatment with tax obligations, emphasizing the challenges in aligning the two. Key points include the definition of franchise fees, initial services provided by franchisors, and the complexities of deferred revenue in franchising.