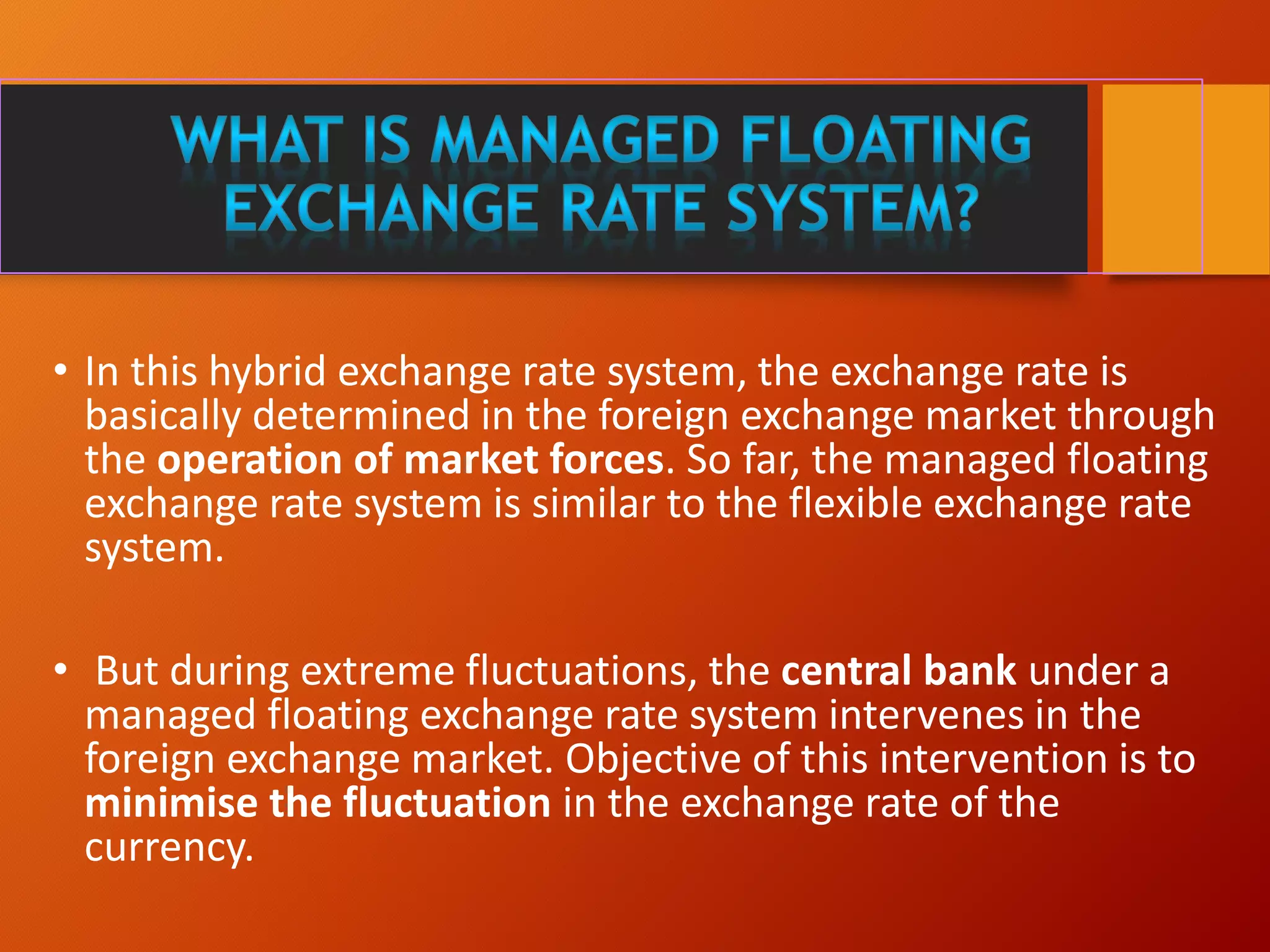

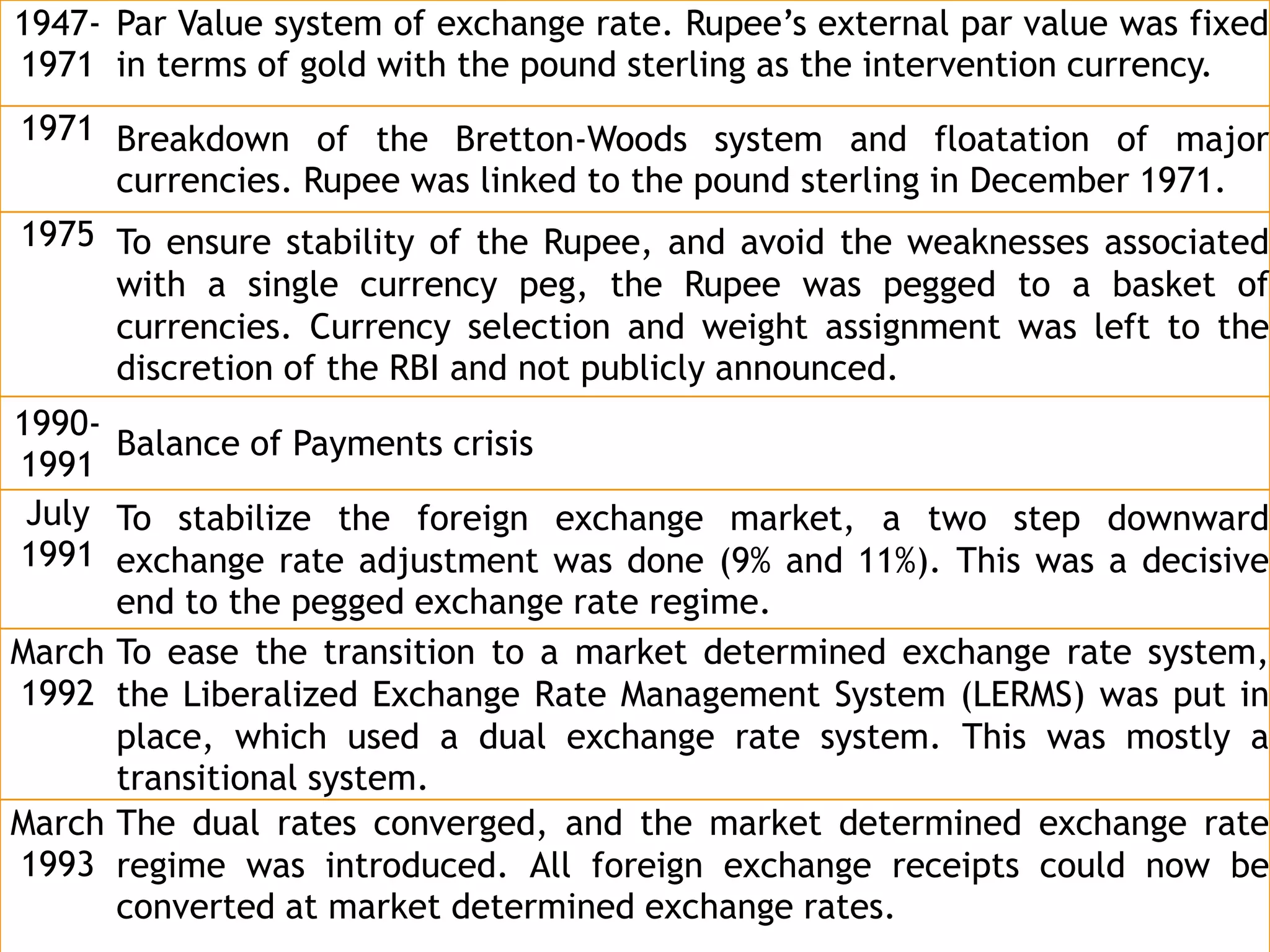

The document discusses India's managed floating exchange rate system where the value of the rupee is determined by market forces in the foreign exchange market but the central bank intervenes during extreme fluctuations to minimize currency value changes. It provides a history of India's exchange rate regimes from 1947 to 1993 when it transitioned to a market-determined system. Tables show the annual average exchange rate of the rupee against the US dollar from 1993 to 2013, which generally depreciated over time except for some appreciation periods. The document also discusses the effects of rupee appreciation and depreciation on imports, exports, inflation and the balance of payments.