Downloaded 947 times

![Foreword | Key Findings | What is FinTech? | Why Hong Kong as a Hub? | Case Studies | The Rise of Hubs | Recommendations | Info

The Rise of FinTech: Getting Hong Kong to lead the digital financial transition in APAC Page | 12

“[The] pace of change across the UK financial services sector is unprecedented, with more fundamental change happening over the next 10 years than has happened over the last 200 years”

Lord Blackwell – Lloyds Banking Group chairman](https://image.slidesharecdn.com/fintechhkreport-nov14-141109115756-conversion-gate01/85/FinTech-Hong-Kong-Report-12-320.jpg)

![Foreword | Key Findings | What is FinTech? | Why Hong Kong as a Hub? | Case Studies | The Rise of Hubs | Recommendations | Info

The Rise of FinTech: Getting Hong Kong to lead the digital financial transition in APAC Page | 25

References:

Reports & Books:

Accenture, ‘The Every Day Bank In China’ & ‘The Rise of Fintech’

Accenture & CB Insights, ‘The FinTech Investment Landscape’

Capgemini, ‘Asia-Pacific Wealth Report 2014’

Census and Statistics Department, ‘The Financial Services Sector in Hong Kong’

Citi & The Economist, ‘Hot Spots Benchmarking global city competitiveness’

Cull R. and Demirguc-Kunt A. and Morduch. J, ‘Banking the World: Empirical Foundation of Financial Inclusion’

Ersnt & Young commissioned by UKTI, ‘Landscaping UK FinTech”

Hong Kong Government, ‘Hong Kong: The Facts Financial Services’

InvestHK, ‘The Greater Pearl River Delta’

KPMG & The Committee for Sydney, ‘Unlocking the Potential: The FinTech opportunity for Sydney’

Long Finance, ‘The global Financial Centres Index 15’

McKinsey & Company, ‘How to prepare for Asia’s digital-banking boom’

Shrader L. and Duflos E. ‘China: A new paradigm in Branchless Banking?’

Sparreboom P. and Duflos E. ‘Financial Inclusion in the People’s Republic of China: An analysis of existing research and public data’

StartmeupHK, ‘How Start-ups Can Succeed in the Asian Market’

World Bank, “Global Financial Development Report 2014”

World Economic Forum, “Competitiveness Report 2013-2014”

Data Sets:

FinDex (World Bank Financial Inclusion) Data Bank (link)

StartBase.Hk (link)

CIA World Fact Book (link)

Photographic Credit:

Artofphoto ‘Flight departing to Hong Kong’ (page 21)

Chrischan1017, ‘Central Hong Kong’ (page 26)

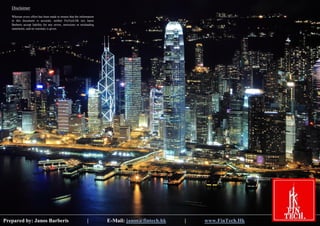

Fintastique, ‘Hong Kong Skyline At Night’ (page 6)

Iakov Kalinin, ‘Hong Kong Harbour’ (cover)

J.Barberis, ‘Photons’, ‘Godzilla’, ‘Speed [1998]’ (pages 2, 11, 22)

Nohead Lam, ‘Night Scene of Hong Kong’ (page 16)

Acknowledgements

Special thanks to David Parker (@DParkerIIP) and Huy Nguyen Trieu (@Huynguyentrieu) for their time and the thought-provoking discussions on the topic.

I am also grateful to all the interviewees who kindly agreed to share their views and took part in FinTechHk’s first report.

Last but not certainly not least, I am also thankful to Jordan Dimov (A115) who helped deploy the website and for his continuous support.](https://image.slidesharecdn.com/fintechhkreport-nov14-141109115756-conversion-gate01/85/FinTech-Hong-Kong-Report-25-320.jpg)

The document discusses Hong Kong's potential to become a leading fintech hub in the Asia-Pacific region by leveraging its existing financial infrastructure, expertise, and market opportunities. Key findings highlight significant growth in fintech investments and the city's favorable conditions for startup innovation, but emphasize the need for continued efforts to address existing gaps in the ecosystem. Recommendations are provided to support the development of a comprehensive environment for fintech growth and elevate Hong Kong's status on the global stage.