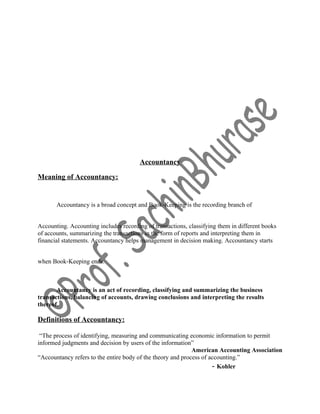

This document provides an overview of bookkeeping and accounting. It defines bookkeeping as the process of systematically recording all business transactions. As business activities grew more complex, the need arose to record transactions to remember dealings and ascertain profits. Accounting builds upon bookkeeping by classifying, summarizing, and interpreting recorded data to assess a business's financial performance and position. Key terms like assets, liabilities, income, and expenses are also defined. Overall, the document outlines the basic concepts and purposes of bookkeeping and accounting systems.