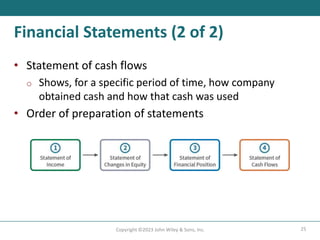

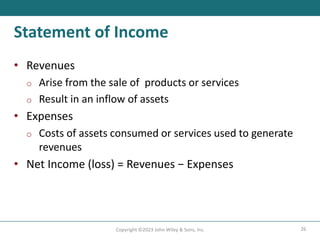

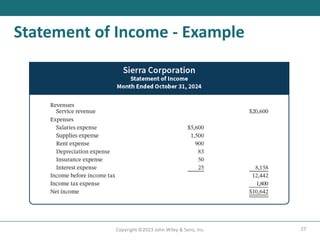

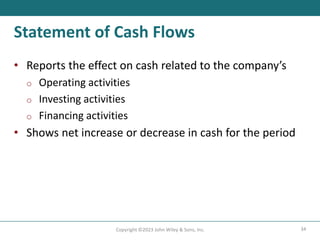

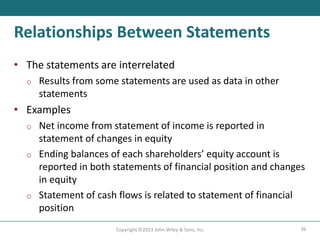

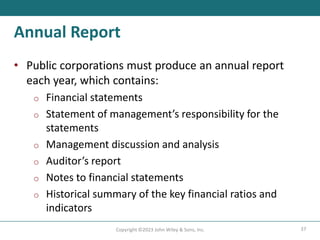

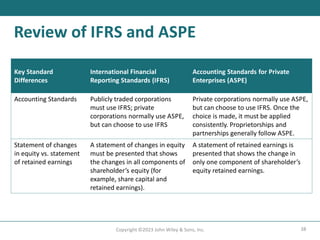

This document provides an overview of financial accounting and financial statements. It discusses the purpose and uses of accounting information for internal and external users of different types of businesses. The four main types of financial statements are described - the statement of income, statement of changes in equity, statement of financial position, and statement of cash flows. The document also explains the key elements and purpose of each financial statement.