Downloaded 11 times

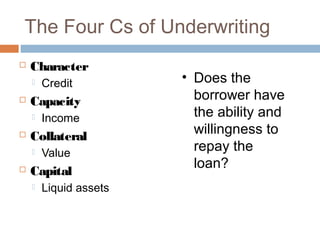

The four Cs of underwriting are: 1. Character - The borrower's credit history 2. Capacity - The borrower's ability to repay based on income 3. Collateral - The value of the property securing the loan 4. Capital - The borrower's available funds, typically a down payment