Download as PDF, PPTX

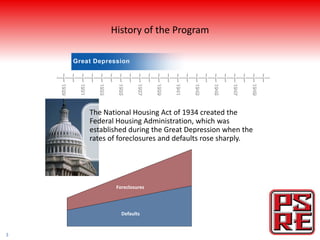

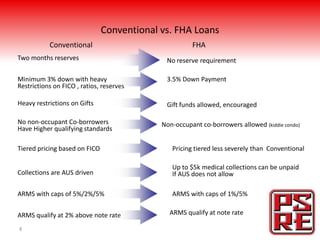

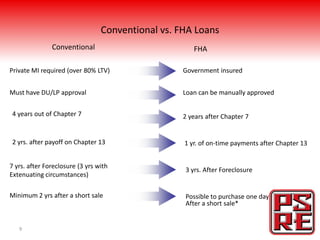

The document outlines educational courses approved for credit by the California Department of Real Estate, emphasizing that such approval does not endorse the course sponsors' views. It provides historical context about the Federal Housing Administration (FHA), its goals, and the differences between FHA and conventional loans, including credit guidelines and loan requirements. Additionally, it includes refinancing options and resources for distressed homeowners and mentions the application of FHA loans for buying and rehabilitating homes.