Download free for 30 days

Sign in

Upload

Language (EN)

Support

Business

Mobile

Social Media

Marketing

Technology

Art & Photos

Career

Design

Education

Presentations & Public Speaking

Government & Nonprofit

Healthcare

Internet

Law

Leadership & Management

Automotive

Engineering

Software

Recruiting & HR

Retail

Sales

Services

Science

Small Business & Entrepreneurship

Food

Environment

Economy & Finance

Data & Analytics

Investor Relations

Sports

Spiritual

News & Politics

Travel

Self Improvement

Real Estate

Entertainment & Humor

Health & Medicine

Devices & Hardware

Lifestyle

Change Language

Language

English

Español

Português

Français

Deutsche

Cancel

Save

EN

Uploaded by

MochammadRidwanRisty3

PPT, PDF

8 views

ffm912-cash-flow-estimation-and-risk-analysis.ppt

fm912-cash-flow-estimation-and-risk-analysis

Education

◦

Read more

0

Save

Share

Embed

Embed presentation

Download

Download to read offline

1

/ 39

2

/ 39

3

/ 39

4

/ 39

5

/ 39

6

/ 39

7

/ 39

8

/ 39

9

/ 39

10

/ 39

11

/ 39

12

/ 39

13

/ 39

14

/ 39

15

/ 39

16

/ 39

17

/ 39

18

/ 39

19

/ 39

20

/ 39

21

/ 39

22

/ 39

23

/ 39

24

/ 39

25

/ 39

26

/ 39

27

/ 39

28

/ 39

29

/ 39

30

/ 39

31

/ 39

32

/ 39

33

/ 39

34

/ 39

35

/ 39

36

/ 39

37

/ 39

38

/ 39

39

/ 39

More Related Content

PPT

CashFlow/dsc/LTV/triple net for cash flow

by

Ludwig

PPT

3 aminullah assagaf ch. 11 sd15_financial management_22 okt 2020

by

Aminullah Assagaf

PPT

Aminullah assagaf financial management p1115_ch. 11 sd15_28 mei 2021

by

Aminullah Assagaf

PPT

Aminullah assagaf p1115 ch. 11 sd15_financial management_28 mei 2021

by

Aminullah Assagaf

PPT

Fm11 ch 11 cash flow estimation and risk analysis

by

Nhu Tuyet Tran

PPT

260928092-Cash-Flow-Estimation-and-Risk-Analysis.ppt

by

MochammadRidwanRisty3

DOCX

Cash Flow Estimation and Risk AnalysisCHAPTER 11© 2020 Cenga.docx

by

troutmanboris

DOCX

Cash Flow Estimation and Risk AnalysisCHAPTER 11© 2020 Cenga.docx

by

keturahhazelhurst

CashFlow/dsc/LTV/triple net for cash flow

by

Ludwig

3 aminullah assagaf ch. 11 sd15_financial management_22 okt 2020

by

Aminullah Assagaf

Aminullah assagaf financial management p1115_ch. 11 sd15_28 mei 2021

by

Aminullah Assagaf

Aminullah assagaf p1115 ch. 11 sd15_financial management_28 mei 2021

by

Aminullah Assagaf

Fm11 ch 11 cash flow estimation and risk analysis

by

Nhu Tuyet Tran

260928092-Cash-Flow-Estimation-and-Risk-Analysis.ppt

by

MochammadRidwanRisty3

Cash Flow Estimation and Risk AnalysisCHAPTER 11© 2020 Cenga.docx

by

troutmanboris

Cash Flow Estimation and Risk AnalysisCHAPTER 11© 2020 Cenga.docx

by

keturahhazelhurst

Similar to ffm912-cash-flow-estimation-and-risk-analysis.ppt

PPT

Ch12ppt

by

JESSIEOU

PPT

Capital budgeting cash flow estimation

by

Prafulla Tekriwal

PPT

Cash Flow Estimation.ppt

by

AdiVanIon1

PPT

Chapter 11 - Cash Flow Estimation and Risk Analysis.ppt

by

AhmedElGayar13

PDF

AF3313 - Lecture 4 - accccc Chapter 6.pdf

by

mksellson

PPTX

CAPITAL BUDGETING DISCUSSION FINMAN.pptx

by

catolicojoaennelzhen

PDF

Ch14sol cash flow estimation

by

Hassan Zada

PPT

Chap010

by

Morten Andersen

PPTX

Corporate Finance Chapter (3).pptx ggghg

by

rafidullah1

PDF

Risk Analysis and Project Evaluation/Abshor.Marantika/Gita Mutiara Ovelia/3-3

by

gitaovelia

DOC

Cb practice problems

by

Bathini Hari Babu

PPT

Cff311.ppt

by

Reema975562

PPT

Additional File-Capital Budgeting 3.ppt

by

ArneetSarna1

DOCX

aPart 5 Corporate Valuation and GovernanceEasy Problem.docx

by

justine1simpson78276

DOCX

1. Payback Period and Net Present Value[LO1, 2] If a project with .docx

by

paynetawnya

PPT

Capital budgeting

by

Jaffer Vailankara

PPT

Chapter 9.Risk and Managerial Options in Capital Budgeting

by

ZahraMirzayeva

PPT

Capital Budgeting

by

yashpal01

PDF

Group 2, Presentation, Making Investment Decision (Cash Flow Protection), F.M...

by

JokZemarko

PPTX

Project Profitability Analysis and Evaluation

by

Arpit Amar

Ch12ppt

by

JESSIEOU

Capital budgeting cash flow estimation

by

Prafulla Tekriwal

Cash Flow Estimation.ppt

by

AdiVanIon1

Chapter 11 - Cash Flow Estimation and Risk Analysis.ppt

by

AhmedElGayar13

AF3313 - Lecture 4 - accccc Chapter 6.pdf

by

mksellson

CAPITAL BUDGETING DISCUSSION FINMAN.pptx

by

catolicojoaennelzhen

Ch14sol cash flow estimation

by

Hassan Zada

Chap010

by

Morten Andersen

Corporate Finance Chapter (3).pptx ggghg

by

rafidullah1

Risk Analysis and Project Evaluation/Abshor.Marantika/Gita Mutiara Ovelia/3-3

by

gitaovelia

Cb practice problems

by

Bathini Hari Babu

Cff311.ppt

by

Reema975562

Additional File-Capital Budgeting 3.ppt

by

ArneetSarna1

aPart 5 Corporate Valuation and GovernanceEasy Problem.docx

by

justine1simpson78276

1. Payback Period and Net Present Value[LO1, 2] If a project with .docx

by

paynetawnya

Capital budgeting

by

Jaffer Vailankara

Chapter 9.Risk and Managerial Options in Capital Budgeting

by

ZahraMirzayeva

Capital Budgeting

by

yashpal01

Group 2, Presentation, Making Investment Decision (Cash Flow Protection), F.M...

by

JokZemarko

Project Profitability Analysis and Evaluation

by

Arpit Amar

More from MochammadRidwanRisty3

PPTX

BALANCE SCORECARD konsep perhitungan.pptx

by

MochammadRidwanRisty3

PDF

497231341-Turban-10e-Ppt-Ch12-en-id-1.pdf

by

MochammadRidwanRisty3

PPTX

852592845-Brigham-FFM16-Concise11-Ch14-PPT.pptx

by

MochammadRidwanRisty3

PDF

Model Antrian_Riset Operasi latihan soal.pdf

by

MochammadRidwanRisty3

PPT

ch08 supply chain management and erp.ppt

by

MochammadRidwanRisty3

PPT

ch09 planning and business process redesign.ppt

by

MochammadRidwanRisty3

PPT

235669801-model-antrian-riset operasional.ppt

by

MochammadRidwanRisty3

PPTX

454065865-bab-12-Estimasi-Arus-Kas-dan-Analisis-Risiko-new-pptx.pptx

by

MochammadRidwanRisty3

PPTX

Mengukur dan Mengelola Paparan Terjemahan dan Transaksi.pptx

by

MochammadRidwanRisty3

PPT

ch12 international financial funds and national capital

by

MochammadRidwanRisty3

PPTX

Financial Futures discuss study in class

by

MochammadRidwanRisty3

PPTX

FIN335 CH08 Risk&Return presentation study

by

MochammadRidwanRisty3

PPT

bahan ke-5 produksi dan teori biaya produksi.ppt

by

MochammadRidwanRisty3

PPTX

Biaya dan Estimasi dan perkiraan biaya produksi

by

MochammadRidwanRisty3

PPT

Prestasi Manajemen Keuangan Internasional BAB 9

by

MochammadRidwanRisty3

BALANCE SCORECARD konsep perhitungan.pptx

by

MochammadRidwanRisty3

497231341-Turban-10e-Ppt-Ch12-en-id-1.pdf

by

MochammadRidwanRisty3

852592845-Brigham-FFM16-Concise11-Ch14-PPT.pptx

by

MochammadRidwanRisty3

Model Antrian_Riset Operasi latihan soal.pdf

by

MochammadRidwanRisty3

ch08 supply chain management and erp.ppt

by

MochammadRidwanRisty3

ch09 planning and business process redesign.ppt

by

MochammadRidwanRisty3

235669801-model-antrian-riset operasional.ppt

by

MochammadRidwanRisty3

454065865-bab-12-Estimasi-Arus-Kas-dan-Analisis-Risiko-new-pptx.pptx

by

MochammadRidwanRisty3

Mengukur dan Mengelola Paparan Terjemahan dan Transaksi.pptx

by

MochammadRidwanRisty3

ch12 international financial funds and national capital

by

MochammadRidwanRisty3

Financial Futures discuss study in class

by

MochammadRidwanRisty3

FIN335 CH08 Risk&Return presentation study

by

MochammadRidwanRisty3

bahan ke-5 produksi dan teori biaya produksi.ppt

by

MochammadRidwanRisty3

Biaya dan Estimasi dan perkiraan biaya produksi

by

MochammadRidwanRisty3

Prestasi Manajemen Keuangan Internasional BAB 9

by

MochammadRidwanRisty3

Recently uploaded

PPTX

Unit 3- Culture.pptx....................

by

Akanksha Kotangale

PPTX

Day 2 ppt english.powerpoint presentation ppt

by

JeahMaeMedez

PPTX

"Aristotle : Father Of Western Philosophy"

by

mitalbarathod28

PPTX

literary theory and criticism by Vivek p

by

vivekrathodborda

PDF

Lamarckism: Theory of Evolution, Principles, Examples, Objections and Neo-Lam...

by

IPGDCWA,NAMPALLY

PPTX

PREVENTIVE PEDIATRICS.pptx

by

BANDITA PATRA

PPTX

Appreciations - Jan 26 01.pptxkjkjkkjkjkjkj

by

preetheshparmar

PPTX

" Jaya : Silence as Resistance " - That long silence

by

dharabhandari35

PPTX

West Hatch High School - GCSE Media Studies

by

WestHatch

PPTX

COMMUNICATION ITS PROCESS ELEMENTS & BARRIER .pptx

by

PoojaSen20

PDF

Beak Modifications by Dr. Ramzan Virani pptx.pdf

by

Dr. Ramzan Virani

PDF

Risks and opportunities of artificial intelligence in education: A critical view

by

Yannis

PPTX

Poster Based Ethical Reflection - Dharma and Values Poster.pptx

by

RajshreeBeneymadoo

PDF

Darwinism: Theory of Natural Selection and Origin of Species

by

IPGDCWA,NAMPALLY

PPTX

Metabolism ( BIOCHEMISTRY & CLINICAL PATHOLOGY )

by

BushraDeshpande

PDF

Chapter 05 Drug Acting on CNS Sedatives & Hypnotics | Antipsychotics.pdf

by

SandeshSul

PPTX

Payment Follow-Up via WhatsApp in Odoo 18.1 Accounting

by

Celine George

PDF

Aminoglycosides.pdf for B.Pharmacy Medicinal Chemistry-III (BP601T), GPAT, a...

by

mominzarinamdnajeeb

PPTX

Master of Punjabi Short Story "kartar singh duggal

by

bhautikbharwad4

PPTX

28 January 2026 Rebecca Frankum Are high-stakes exams and assessments still r...

by

EduSkills OECD

Unit 3- Culture.pptx....................

by

Akanksha Kotangale

Day 2 ppt english.powerpoint presentation ppt

by

JeahMaeMedez

"Aristotle : Father Of Western Philosophy"

by

mitalbarathod28

literary theory and criticism by Vivek p

by

vivekrathodborda

Lamarckism: Theory of Evolution, Principles, Examples, Objections and Neo-Lam...

by

IPGDCWA,NAMPALLY

PREVENTIVE PEDIATRICS.pptx

by

BANDITA PATRA

Appreciations - Jan 26 01.pptxkjkjkkjkjkjkj

by

preetheshparmar

" Jaya : Silence as Resistance " - That long silence

by

dharabhandari35

West Hatch High School - GCSE Media Studies

by

WestHatch

COMMUNICATION ITS PROCESS ELEMENTS & BARRIER .pptx

by

PoojaSen20

Beak Modifications by Dr. Ramzan Virani pptx.pdf

by

Dr. Ramzan Virani

Risks and opportunities of artificial intelligence in education: A critical view

by

Yannis

Poster Based Ethical Reflection - Dharma and Values Poster.pptx

by

RajshreeBeneymadoo

Darwinism: Theory of Natural Selection and Origin of Species

by

IPGDCWA,NAMPALLY

Metabolism ( BIOCHEMISTRY & CLINICAL PATHOLOGY )

by

BushraDeshpande

Chapter 05 Drug Acting on CNS Sedatives & Hypnotics | Antipsychotics.pdf

by

SandeshSul

Payment Follow-Up via WhatsApp in Odoo 18.1 Accounting

by

Celine George

Aminoglycosides.pdf for B.Pharmacy Medicinal Chemistry-III (BP601T), GPAT, a...

by

mominzarinamdnajeeb

Master of Punjabi Short Story "kartar singh duggal

by

bhautikbharwad4

28 January 2026 Rebecca Frankum Are high-stakes exams and assessments still r...

by

EduSkills OECD

ffm912-cash-flow-estimation-and-risk-analysis.ppt

1.

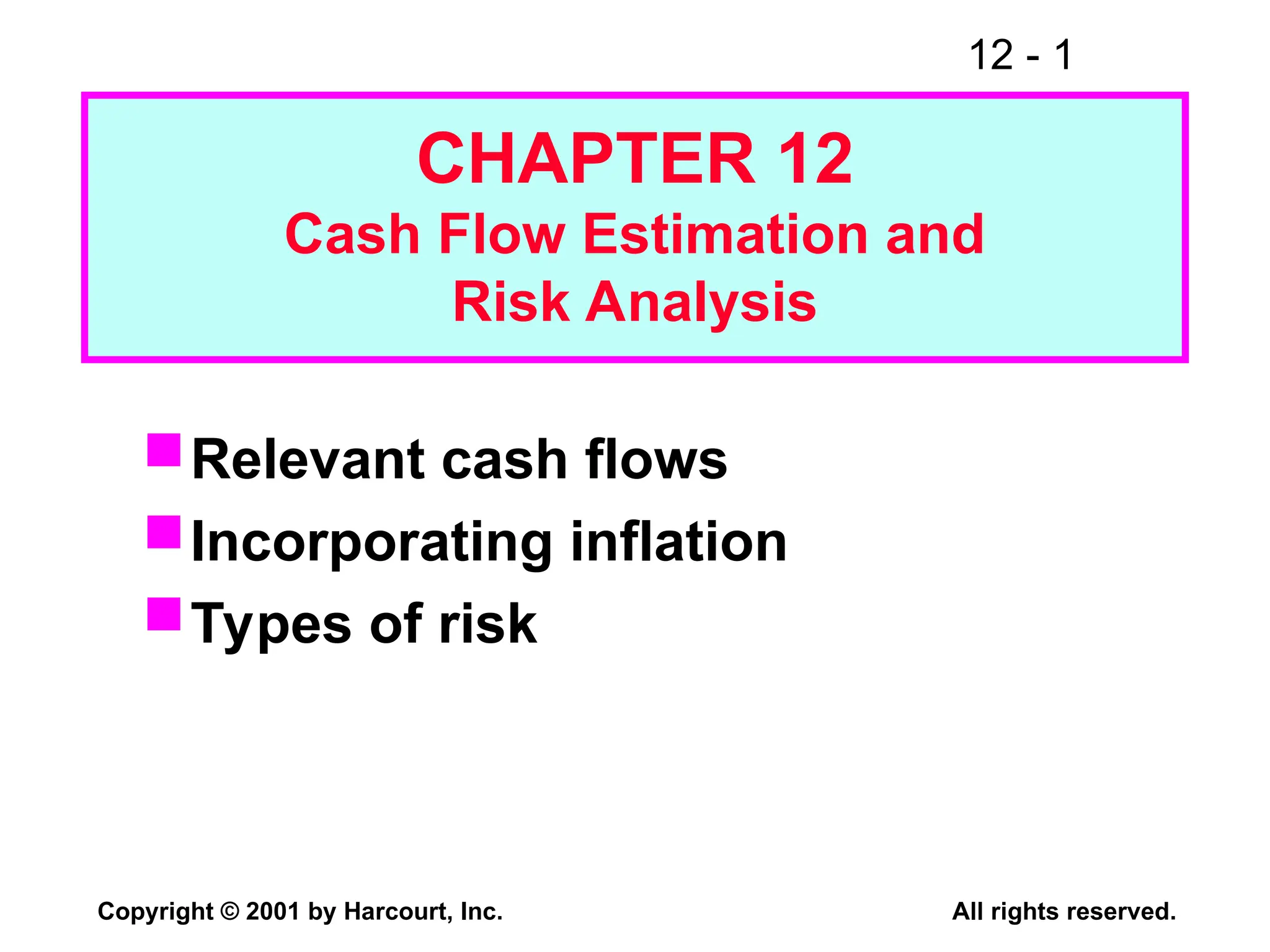

12 - 1 Copyright

© 2001 by Harcourt, Inc. All rights reserved. CHAPTER 12 Cash Flow Estimation and Risk Analysis Relevant cash flows Incorporating inflation Types of risk

2.

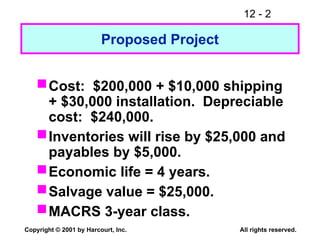

12 - 2 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Proposed Project Cost: $200,000 + $10,000 shipping + $30,000 installation. Depreciable cost: $240,000. Inventories will rise by $25,000 and payables by $5,000. Economic life = 4 years. Salvage value = $25,000. MACRS 3-year class.

3.

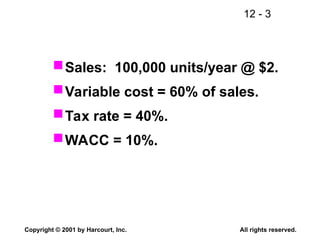

12 - 3 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Sales: 100,000 units/year @ $2. Variable cost = 60% of sales. Tax rate = 40%. WACC = 10%.

4.

12 - 4 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Set up, without numbers, a time line for the project’s cash flows. 0 1 2 3 4 OCF1 OCF2 OCF3 OCF4 Initial Costs (CF0) + Terminal CF NCF0 NCF1 NCF2 NCF3 NCF4

5.

12 - 5 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Equipment -$200 Installation & Shipping -40 Increase in inventories -25 Increase in A/P 5 Net CF0 -$260 NOWC = $25 – $5 = $20. Investment at t = 0:

6.

12 - 6 Copyright

© 2001 by Harcourt, Inc. All rights reserved. What’s the annual depreciation? Due to 1/2-year convention, a 3-year asset is depreciated over 4 years. Year Rate x Basis Depreciation 1 0.33 $240 $ 79 2 0.45 240 108 3 0.15 240 36 4 0.07 240 17 1.00 $240

7.

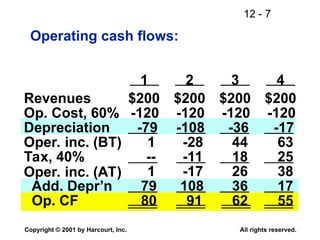

12 - 7 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Operating cash flows: 1 2 3 4 Revenues $200 $200 $200 $200 Op. Cost, 60% -120 -120 -120 -120 Depreciation -79 -108 -36 -17 Oper. inc. (BT) 1 -28 44 63 Tax, 40% -- -11 18 25 1 -17 26 38 Add. Depr’n 79 108 36 17 Op. CF 80 91 62 55 Oper. inc. (AT)

8.

12 - 8 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Net Terminal CF at t = 4: Salvage Value 25 Tax on SV (40%) -10 Recovery of NOWC $20 Net termination CF $35 Q. Always a tax on SV? Ever a positive tax number? Q. How is NOWC recovered?

9.

12 - 9 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Should CFs include interest expense? Dividends? No. The cost of capital is accounted for by discounting at the 10% WACC, so deducting interest and dividends would be “double counting” financing costs.

10.

12 - 10 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Suppose $50,000 had been spent last year to improve the building. Should this cost be included in the analysis? No. This is a sunk cost. Analyze incremental investment.

11.

12 - 11 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Suppose the plant could be leased out for $25,000 a year. Would this affect the analysis? Yes. Accepting the project means foregoing the $25,000. This is an opportunity cost, and it should be charged to the project. A.T. opportunity cost = $25,000(1 – T) = $25,000(0.6) = $15,000 annual cost.

12.

12 - 12 Copyright

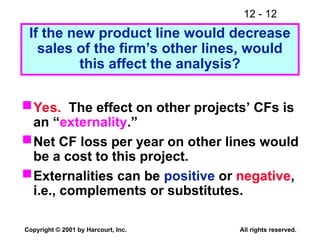

© 2001 by Harcourt, Inc. All rights reserved. If the new product line would decrease sales of the firm’s other lines, would this affect the analysis? Yes. The effect on other projects’ CFs is an “externality.” Net CF loss per year on other lines would be a cost to this project. Externalities can be positive or negative, i.e., complements or substitutes.

13.

12 - 13 Copyright

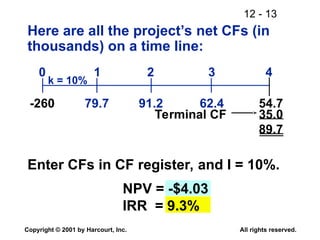

© 2001 by Harcourt, Inc. All rights reserved. Here are all the project’s net CFs (in thousands) on a time line: Enter CFs in CF register, and I = 10%. NPV = -$4.03 IRR = 9.3% k = 10% 0 79.7 1 91.2 2 62.4 3 54.7 4 -260 Terminal CF 35.0 89.7

14.

12 - 14 Copyright

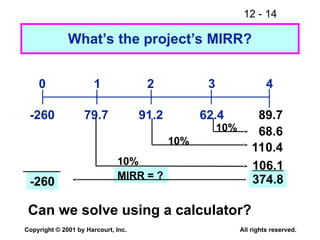

© 2001 by Harcourt, Inc. All rights reserved. MIRR = ? 10% What’s the project’s MIRR? Can we solve using a calculator? 0 79.7 1 91.2 2 62.4 3 89.7 4 -260 374.8 -260 68.6 110.4 10% 10% 106.1

15.

12 - 15 Copyright

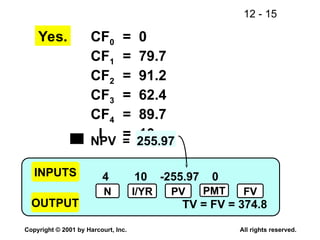

© 2001 by Harcourt, Inc. All rights reserved. 4 10 -255.97 0 TV = FV = 374.8 Yes. CF0 = 0 CF1 = 79.7 CF2 = 91.2 CF3 = 62.4 CF4 = 89.7 I = 10 NPV = 255.97 INPUTS OUTPUT N I/YR PV PMT FV

16.

12 - 16 Copyright

© 2001 by Harcourt, Inc. All rights reserved. Use the FV = TV of inputs to find MIRR 4 -260 0 374.8 9.6 MIRR = 9.6%. Since MIRR < k = 10%, reject the project. INPUTS OUTPUT N I/YR PV PMT FV

17.

12 - 17 Copyright

© 2001 by Harcourt, Inc. All rights reserved. What’s the payback period? 0 79.7 1 91.2 2 62.4 3 89.7 4 -260 Cumulative: -26.7 -260 -89.1 -180.3 63.0 Payback = 3 + 26.7/89.7 = 3.3 years.

18.

12 - 18 Copyright

© 2001 by Harcourt, Inc. All rights reserved. If this were a replacement rather than a new project, would the analysis change? Yes. The old equipment would be sold, and the incremental CFs would be the changes from the old to the new situation.

19.

12 - 19 Copyright

© 2001 by Harcourt, Inc. All rights reserved. The relevant depreciation would be the change with the new equipment. Also, if the firm sold the old machine now, it would not receive the SV at the end of the machine’s life. This is an opportunity cost for the replacement project.

20.

12 - 20 Copyright

© 2001 by Harcourt, Inc. All rights reserved. . k 1 Cost v Re k 1 CF NPV t t t t t n 0 t Q. If E(INFL) = 5%, is NPV biased? A. YES. k = k* + IP + DRP + LP + MRP. Inflation is in denominator but not in numerator, so downward bias to NPV. Should build inflation into CF forecasts.

21.

12 - 21 Copyright

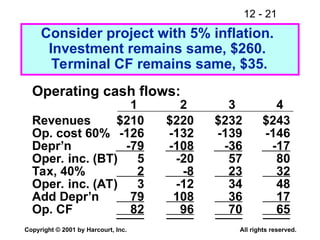

© 2001 by Harcourt, Inc. All rights reserved. Consider project with 5% inflation. Investment remains same, $260. Terminal CF remains same, $35. Operating cash flows: 1 2 3 4 Revenues $210 $220 $232 $243 Op. cost 60% -126 -132 -139 -146 Depr’n -79 -108 -36 -17 Oper. inc. (BT) 5 -20 57 80 Tax, 40% 2 -8 23 32 Oper. inc. (AT) 3 -12 34 48 Add Depr’n 79 108 36 17 Op. CF 82 96 70 65

22.

12 - 22 Copyright

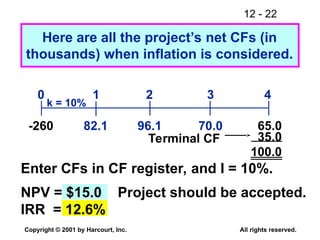

© 2001 by Harcourt, Inc. All rights reserved. Here are all the project’s net CFs (in thousands) when inflation is considered. Enter CFs in CF register, and I = 10%. NPV = $15.0 IRR = 12.6% k = 10% 0 82.1 1 96.1 2 70.0 3 65.0 4 -260 Terminal CF 35.0 100.0 Project should be accepted.

23.

12 - 23 Copyright

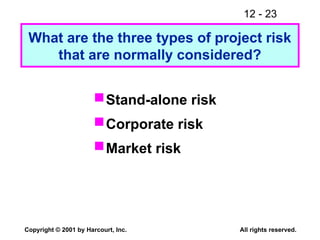

© 2001 by Harcourt, Inc. All rights reserved. What are the three types of project risk that are normally considered? Stand-alone risk Corporate risk Market risk

24.

12 - 24 Copyright

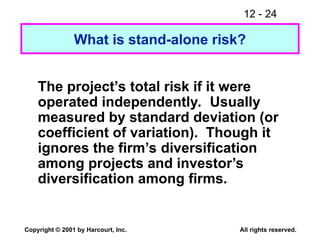

© 2001 by Harcourt, Inc. All rights reserved. What is stand-alone risk? The project’s total risk if it were operated independently. Usually measured by standard deviation (or coefficient of variation). Though it ignores the firm’s diversification among projects and investor’s diversification among firms.

25.

12 - 25 Copyright

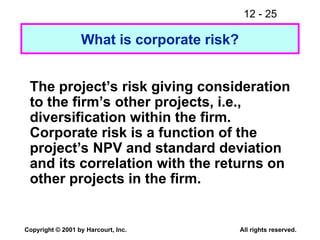

© 2001 by Harcourt, Inc. All rights reserved. What is corporate risk? The project’s risk giving consideration to the firm’s other projects, i.e., diversification within the firm. Corporate risk is a function of the project’s NPV and standard deviation and its correlation with the returns on other projects in the firm.

26.

12 - 26 Copyright

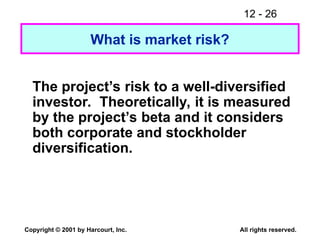

© 2001 by Harcourt, Inc. All rights reserved. What is market risk? The project’s risk to a well-diversified investor. Theoretically, it is measured by the project’s beta and it considers both corporate and stockholder diversification.

27.

12 - 27 Copyright

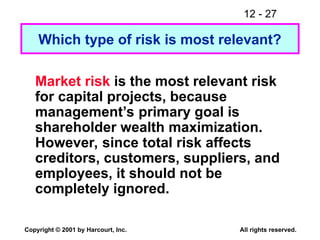

© 2001 by Harcourt, Inc. All rights reserved. Which type of risk is most relevant? Market risk is the most relevant risk for capital projects, because management’s primary goal is shareholder wealth maximization. However, since total risk affects creditors, customers, suppliers, and employees, it should not be completely ignored.

28.

12 - 28 Copyright

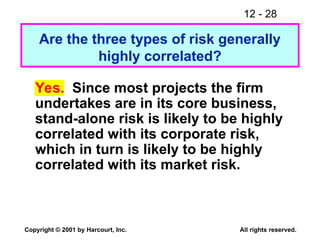

© 2001 by Harcourt, Inc. All rights reserved. Are the three types of risk generally highly correlated? Yes. Since most projects the firm undertakes are in its core business, stand-alone risk is likely to be highly correlated with its corporate risk, which in turn is likely to be highly correlated with its market risk.

29.

12 - 29 Copyright

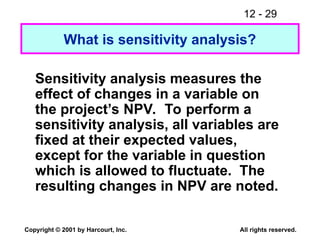

© 2001 by Harcourt, Inc. All rights reserved. What is sensitivity analysis? Sensitivity analysis measures the effect of changes in a variable on the project’s NPV. To perform a sensitivity analysis, all variables are fixed at their expected values, except for the variable in question which is allowed to fluctuate. The resulting changes in NPV are noted.

30.

12 - 30 Copyright

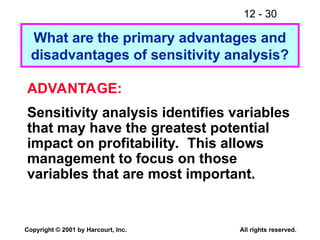

© 2001 by Harcourt, Inc. All rights reserved. What are the primary advantages and disadvantages of sensitivity analysis? ADVANTAGE: Sensitivity analysis identifies variables that may have the greatest potential impact on profitability. This allows management to focus on those variables that are most important.

31.

12 - 31 Copyright

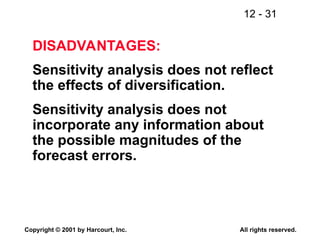

© 2001 by Harcourt, Inc. All rights reserved. DISADVANTAGES: Sensitivity analysis does not reflect the effects of diversification. Sensitivity analysis does not incorporate any information about the possible magnitudes of the forecast errors.

32.

12 - 32 Copyright

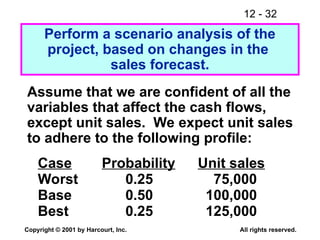

© 2001 by Harcourt, Inc. All rights reserved. Best 0.25 125,000 Perform a scenario analysis of the project, based on changes in the sales forecast. Assume that we are confident of all the variables that affect the cash flows, except unit sales. We expect unit sales to adhere to the following profile: Case Probability Unit sales Base 0.50 100,000 Worst 0.25 75,000

33.

12 - 33 Copyright

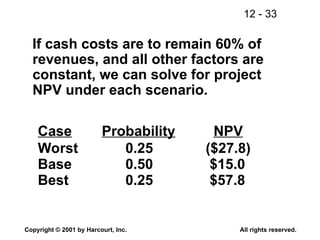

© 2001 by Harcourt, Inc. All rights reserved. If cash costs are to remain 60% of revenues, and all other factors are constant, we can solve for project NPV under each scenario. Best 0.25 $57.8 Case Probability NPV Base 0.50 $15.0 Worst 0.25 ($27.8)

34.

12 - 34 Copyright

© 2001 by Harcourt, Inc. All rights reserved. E(NPV)=.25(-$27.8)+.5($15.0)+.25($57.8) E(NPV)= $15.0. Use these scenarios, with their given probabilities, to find the project’s expected NPV, NPV, and CVNPV. NPV = [.25(-$27.8-$15.0)2 + .5($15.0-$15.0)2 + .25($57.8-$15.0)2 ]1/2 NPV = $30.3. CVNPV = $30.3 /$15.0 = 2.0.

35.

12 - 35 Copyright

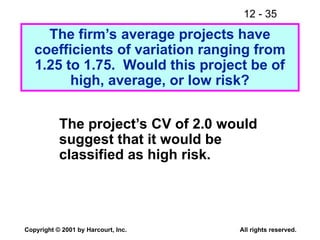

© 2001 by Harcourt, Inc. All rights reserved. The firm’s average projects have coefficients of variation ranging from 1.25 to 1.75. Would this project be of high, average, or low risk? The project’s CV of 2.0 would suggest that it would be classified as high risk.

36.

12 - 36 Copyright

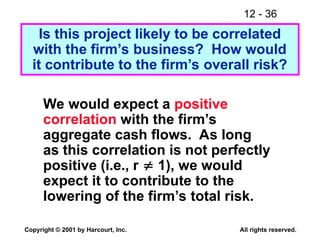

© 2001 by Harcourt, Inc. All rights reserved. Is this project likely to be correlated with the firm’s business? How would it contribute to the firm’s overall risk? We would expect a positive correlation with the firm’s aggregate cash flows. As long as this correlation is not perfectly positive (i.e., r 1), we would expect it to contribute to the lowering of the firm’s total risk.

37.

12 - 37 Copyright

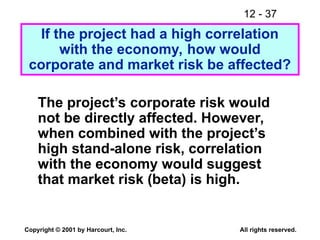

© 2001 by Harcourt, Inc. All rights reserved. The project’s corporate risk would not be directly affected. However, when combined with the project’s high stand-alone risk, correlation with the economy would suggest that market risk (beta) is high. If the project had a high correlation with the economy, how would corporate and market risk be affected?

38.

12 - 38 Copyright

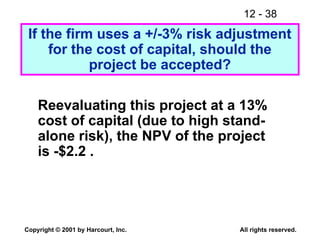

© 2001 by Harcourt, Inc. All rights reserved. Reevaluating this project at a 13% cost of capital (due to high stand- alone risk), the NPV of the project is -$2.2 . If the firm uses a +/-3% risk adjustment for the cost of capital, should the project be accepted?

39.

12 - 39 Copyright

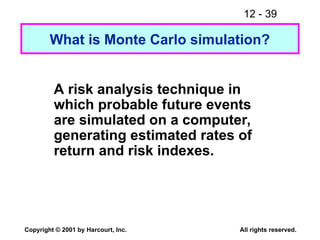

© 2001 by Harcourt, Inc. All rights reserved. A risk analysis technique in which probable future events are simulated on a computer, generating estimated rates of return and risk indexes. What is Monte Carlo simulation?

Download

![12 - 34

Copyright © 2001 by Harcourt, Inc. All rights reserved.

E(NPV)=.25(-$27.8)+.5($15.0)+.25($57.8)

E(NPV)= $15.0.

Use these scenarios, with their given

probabilities, to find the project’s

expected NPV, NPV, and CVNPV.

NPV = [.25(-$27.8-$15.0)2

+ .5($15.0-$15.0)2

+ .25($57.8-$15.0)2

]1/2

NPV = $30.3.

CVNPV = $30.3 /$15.0 = 2.0.](https://image.slidesharecdn.com/ffm912-cash-flow-estimation-and-risk-analysis-251025202856-cc48c2d3/85/ffm912-cash-flow-estimation-and-risk-analysis-ppt-34-320.jpg)

![1. Payback Period and Net Present Value[LO1, 2] If a project with .docx](https://cdn.slidesharecdn.com/ss_thumbnails/1-221101035238-1d86b81e-thumbnail.jpg?width=640&height=640&fit=bounds)