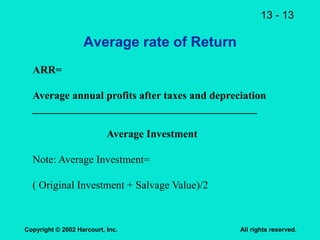

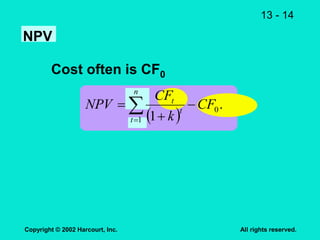

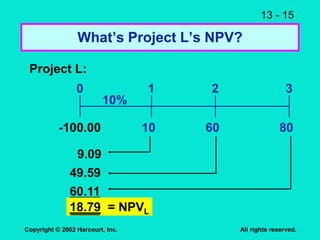

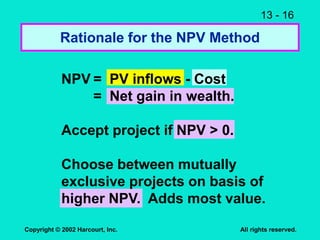

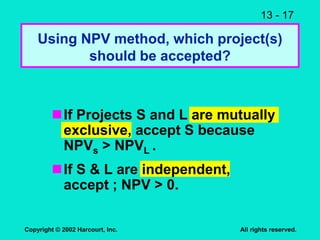

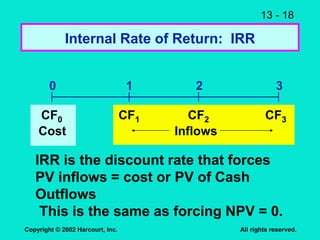

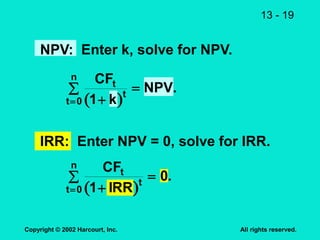

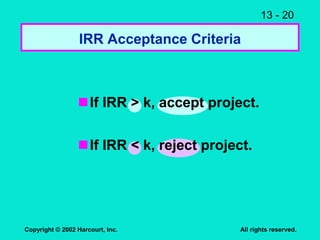

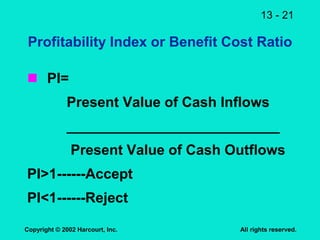

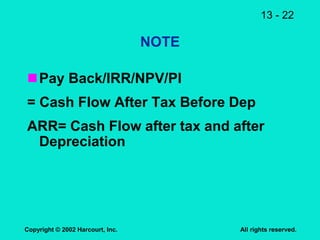

This document discusses various capital budgeting techniques for evaluating investment projects. It defines capital budgeting as the analysis of potential long-term investments that require large expenditures. Several evaluation methods are covered, including payback period, net present value (NPV), internal rate of return (IRR), average rate of return (ARR), and profitability index (PI). Examples are provided to demonstrate how to calculate and apply these techniques. The goal is to determine which projects add the most value and should be accepted based on their ability to meet specific acceptance criteria for each method.

![Cap budget [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/capbudgetautosaved-111120050918-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)