Downloaded 181 times

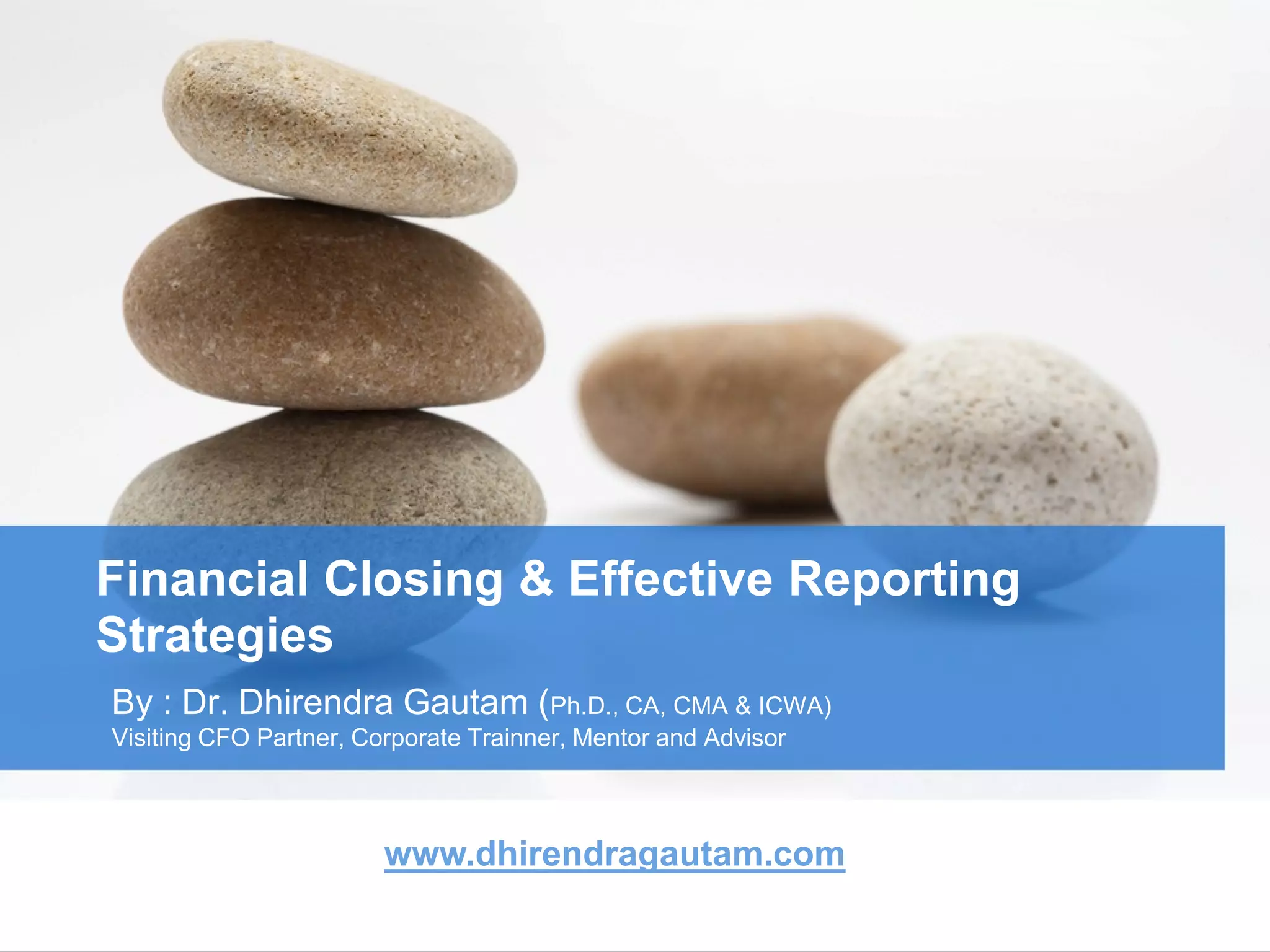

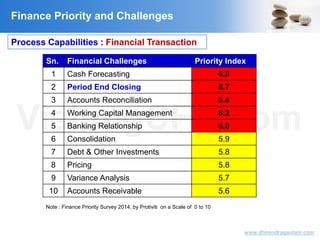

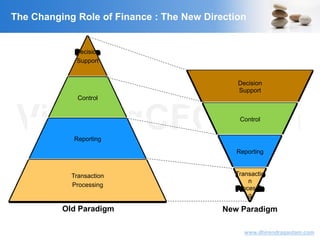

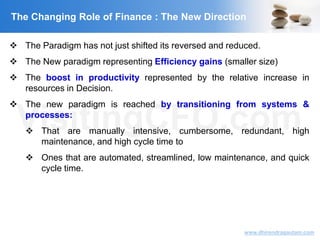

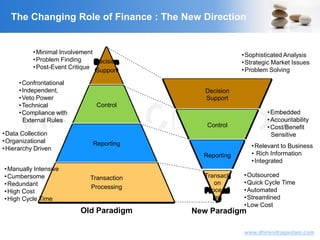

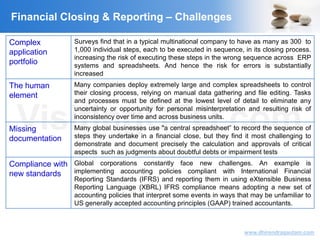

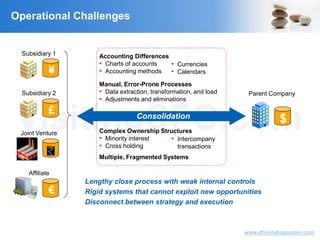

The document discusses financial closing and effective reporting strategies as articulated by Dr. Dhirendra Gautam, who is an experienced corporate mentor and advisor. It outlines the challenges in financial reporting such as cash forecasting, account reconciliation, and compliance with new standards like IFRS, while emphasizing the necessity for faster financial closing processes to enhance decision-making and overall business efficiency. The importance of transitioning to automated and streamlined systems for maintaining accuracy and reducing errors during financial reporting is also highlighted.

![The Finance Automation Journey - How to Fuel Your Finance Transformation [eBook]](https://cdn.slidesharecdn.com/ss_thumbnails/a1cd6c71-82be-4e5a-832b-b1aaafa36ab9-160926233425-thumbnail.jpg?width=640&height=640&fit=bounds)

![APT_Finance_Architect_Brochure_A4_WEB[2]](https://cdn.slidesharecdn.com/ss_thumbnails/98eb63e5-21b9-43b7-8a41-a7a53f2b3494-150723130227-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)