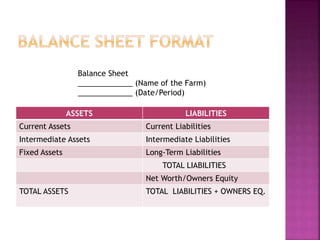

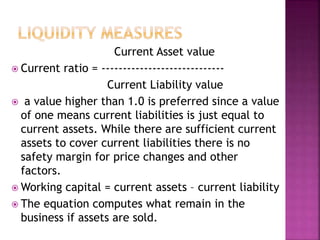

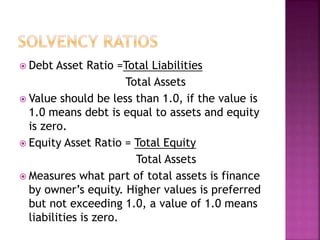

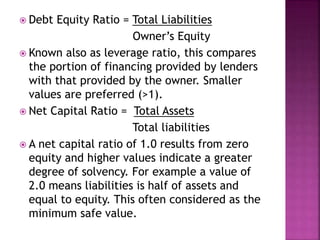

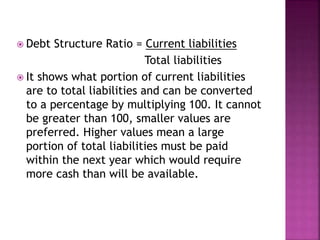

This document provides information on farm inventory and balance sheets. It discusses the purpose of a farm inventory, which is to list all assets owned by the farm and their values. The document outlines the process for taking inventory, including physical counting and valuation of assets. It also describes different methods for valuing assets, such as net market price, cost, and depreciation. The balance sheet lists assets, liabilities, and owner's equity to summarize a farm's financial condition. Current, intermediate, and long-term assets and liabilities are categorized by liquidity. Financial ratios like current ratio and debt-to-asset ratio are used to measure a farm's solvency and liquidity.