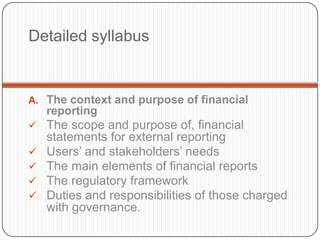

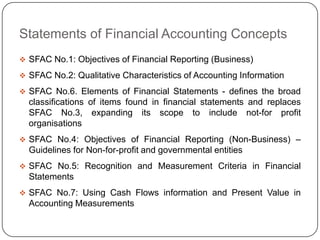

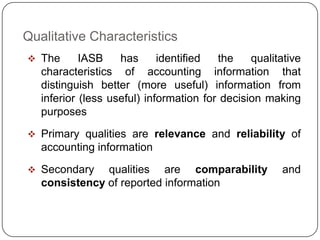

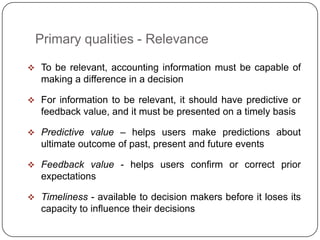

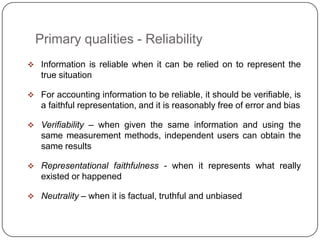

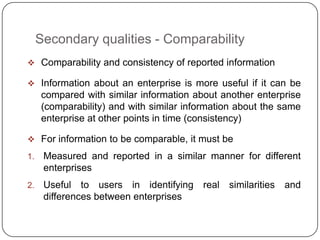

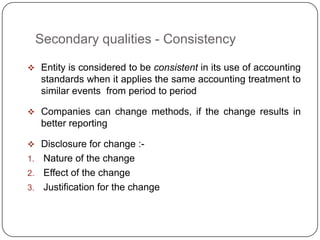

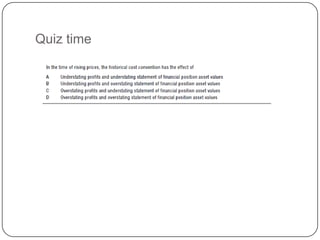

This document outlines the key qualitative characteristics of financial information according to accounting standards. The primary qualities are relevance and reliability. Information must be relevant by having predictive or feedback value in a timely manner. It must be reliable by being verifiable, providing a faithful representation and being reasonably free of error and bias. Secondary qualities include comparability, where information can be compared between entities and over time, and consistency.