1. The document is an IRS Form 1040EZ for the 2010 tax year, which is a simplified tax return for single and joint filers with no dependents.

2. It shows taxpayer information for Ashley Geo with wages of $60,000 and no other income. Standard deduction of $9,350 is subtracted from wages of $60,000 for a taxable income of $50,650.

3. No payments or credits are listed so tax due of $8,850 is calculated using the tax table. No refund is due and full payment of $8,850 is owed.

Essentials of Automations: Optimizing FME Workflows with ParametersSafe Software

Are you looking to streamline your workflows and boost your projects’ efficiency? Do you find yourself searching for ways to add flexibility and control over your FME workflows? If so, you’re in the right place.

Join us for an insightful dive into the world of FME parameters, a critical element in optimizing workflow efficiency. This webinar marks the beginning of our three-part “Essentials of Automation” series. This first webinar is designed to equip you with the knowledge and skills to utilize parameters effectively: enhancing the flexibility, maintainability, and user control of your FME projects.

Here’s what you’ll gain:

- Essentials of FME Parameters: Understand the pivotal role of parameters, including Reader/Writer, Transformer, User, and FME Flow categories. Discover how they are the key to unlocking automation and optimization within your workflows.

- Practical Applications in FME Form: Delve into key user parameter types including choice, connections, and file URLs. Allow users to control how a workflow runs, making your workflows more reusable. Learn to import values and deliver the best user experience for your workflows while enhancing accuracy.

- Optimization Strategies in FME Flow: Explore the creation and strategic deployment of parameters in FME Flow, including the use of deployment and geometry parameters, to maximize workflow efficiency.

- Pro Tips for Success: Gain insights on parameterizing connections and leveraging new features like Conditional Visibility for clarity and simplicity.

We’ll wrap up with a glimpse into future webinars, followed by a Q&A session to address your specific questions surrounding this topic.

Don’t miss this opportunity to elevate your FME expertise and drive your projects to new heights of efficiency.

Builder.ai Founder Sachin Dev Duggal's Strategic Approach to Create an Innova...Ramesh Iyer

In today's fast-changing business world, Companies that adapt and embrace new ideas often need help to keep up with the competition. However, fostering a culture of innovation takes much work. It takes vision, leadership and willingness to take risks in the right proportion. Sachin Dev Duggal, co-founder of Builder.ai, has perfected the art of this balance, creating a company culture where creativity and growth are nurtured at each stage.

PHP Frameworks: I want to break free (IPC Berlin 2024)Ralf Eggert

In this presentation, we examine the challenges and limitations of relying too heavily on PHP frameworks in web development. We discuss the history of PHP and its frameworks to understand how this dependence has evolved. The focus will be on providing concrete tips and strategies to reduce reliance on these frameworks, based on real-world examples and practical considerations. The goal is to equip developers with the skills and knowledge to create more flexible and future-proof web applications. We'll explore the importance of maintaining autonomy in a rapidly changing tech landscape and how to make informed decisions in PHP development.

This talk is aimed at encouraging a more independent approach to using PHP frameworks, moving towards a more flexible and future-proof approach to PHP development.

The Art of the Pitch: WordPress Relationships and SalesLaura Byrne

Clients don’t know what they don’t know. What web solutions are right for them? How does WordPress come into the picture? How do you make sure you understand scope and timeline? What do you do if sometime changes?

All these questions and more will be explored as we talk about matching clients’ needs with what your agency offers without pulling teeth or pulling your hair out. Practical tips, and strategies for successful relationship building that leads to closing the deal.

UiPath Test Automation using UiPath Test Suite series, part 4DianaGray10

Welcome to UiPath Test Automation using UiPath Test Suite series part 4. In this session, we will cover Test Manager overview along with SAP heatmap.

The UiPath Test Manager overview with SAP heatmap webinar offers a concise yet comprehensive exploration of the role of a Test Manager within SAP environments, coupled with the utilization of heatmaps for effective testing strategies.

Participants will gain insights into the responsibilities, challenges, and best practices associated with test management in SAP projects. Additionally, the webinar delves into the significance of heatmaps as a visual aid for identifying testing priorities, areas of risk, and resource allocation within SAP landscapes. Through this session, attendees can expect to enhance their understanding of test management principles while learning practical approaches to optimize testing processes in SAP environments using heatmap visualization techniques

What will you get from this session?

1. Insights into SAP testing best practices

2. Heatmap utilization for testing

3. Optimization of testing processes

4. Demo

Topics covered:

Execution from the test manager

Orchestrator execution result

Defect reporting

SAP heatmap example with demo

Speaker:

Deepak Rai, Automation Practice Lead, Boundaryless Group and UiPath MVP

Connector Corner: Automate dynamic content and events by pushing a buttonDianaGray10

Here is something new! In our next Connector Corner webinar, we will demonstrate how you can use a single workflow to:

Create a campaign using Mailchimp with merge tags/fields

Send an interactive Slack channel message (using buttons)

Have the message received by managers and peers along with a test email for review

But there’s more:

In a second workflow supporting the same use case, you’ll see:

Your campaign sent to target colleagues for approval

If the “Approve” button is clicked, a Jira/Zendesk ticket is created for the marketing design team

But—if the “Reject” button is pushed, colleagues will be alerted via Slack message

Join us to learn more about this new, human-in-the-loop capability, brought to you by Integration Service connectors.

And...

Speakers:

Akshay Agnihotri, Product Manager

Charlie Greenberg, Host

UiPath Test Automation using UiPath Test Suite series, part 3DianaGray10

Welcome to UiPath Test Automation using UiPath Test Suite series part 3. In this session, we will cover desktop automation along with UI automation.

Topics covered:

UI automation Introduction,

UI automation Sample

Desktop automation flow

Pradeep Chinnala, Senior Consultant Automation Developer @WonderBotz and UiPath MVP

Deepak Rai, Automation Practice Lead, Boundaryless Group and UiPath MVP

Smart TV Buyer Insights Survey 2024 by 91mobiles.pdf91mobiles

91mobiles recently conducted a Smart TV Buyer Insights Survey in which we asked over 3,000 respondents about the TV they own, aspects they look at on a new TV, and their TV buying preferences.

GraphRAG is All You need? LLM & Knowledge GraphGuy Korland

Guy Korland, CEO and Co-founder of FalkorDB, will review two articles on the integration of language models with knowledge graphs.

1. Unifying Large Language Models and Knowledge Graphs: A Roadmap.

https://arxiv.org/abs/2306.08302

2. Microsoft Research's GraphRAG paper and a review paper on various uses of knowledge graphs:

https://www.microsoft.com/en-us/research/blog/graphrag-unlocking-llm-discovery-on-narrative-private-data/

Neuro-symbolic is not enough, we need neuro-*semantic*Frank van Harmelen

Neuro-symbolic (NeSy) AI is on the rise. However, simply machine learning on just any symbolic structure is not sufficient to really harvest the gains of NeSy. These will only be gained when the symbolic structures have an actual semantics. I give an operational definition of semantics as “predictable inference”.

All of this illustrated with link prediction over knowledge graphs, but the argument is general.

Epistemic Interaction - tuning interfaces to provide information for AI supportAlan Dix

Paper presented at SYNERGY workshop at AVI 2024, Genoa, Italy. 3rd June 2024

https://alandix.com/academic/papers/synergy2024-epistemic/

As machine learning integrates deeper into human-computer interactions, the concept of epistemic interaction emerges, aiming to refine these interactions to enhance system adaptability. This approach encourages minor, intentional adjustments in user behaviour to enrich the data available for system learning. This paper introduces epistemic interaction within the context of human-system communication, illustrating how deliberate interaction design can improve system understanding and adaptation. Through concrete examples, we demonstrate the potential of epistemic interaction to significantly advance human-computer interaction by leveraging intuitive human communication strategies to inform system design and functionality, offering a novel pathway for enriching user-system engagements.

FIDO Alliance Osaka Seminar: Passkeys at Amazon.pdf

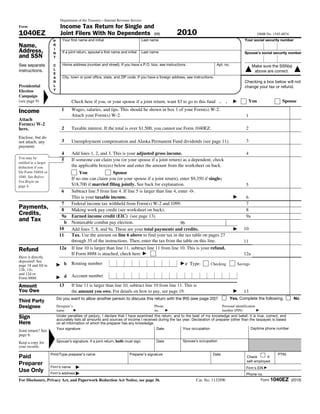

F1040ez

1. Department of the Treasury—Internal Revenue Service

Form Income Tax Return for Single and

1040EZ Joint Filers With No Dependents (99) 2010 OMB No. 1545-0074

P Your first name and initial Last name Your social security number

Name, R

Ashley Geo

Address, I

N If a joint return, spouse’s first name and initial Last name Spouse’s social security number

and SSN T

Jocelyn Wong

See separate C Home address (number and street). If you have a P.O. box, see instructions. Apt. no. Make sure the SSN(s)

instructions. L ▲ above are correct. ▲

E

A City, town or post office, state, and ZIP code. If you have a foreign address, see instructions.

R Checking a box below will not

Presidential L Miami change your tax or refund.

Election Y

▲

Campaign

(see page 9) Check here if you, or your spouse if a joint return, want $3 to go to this fund . . ▶ You Spouse

Income 1 Wages, salaries, and tips. This should be shown in box 1 of your Form(s) W-2.

Attach your Form(s) W-2. 1 60,000 00

Attach

Form(s) W-2

here. 2 Taxable interest. If the total is over $1,500, you cannot use Form 1040EZ. 2 0

Enclose, but do

not attach, any 3 Unemployment compensation and Alaska Permanent Fund dividends (see page 11). 3 0

payment.

4 Add lines 1, 2, and 3. This is your adjusted gross income. 4 60000

You may be

5 If someone can claim you (or your spouse if a joint return) as a dependent, check

entitled to a larger

deduction if you the applicable box(es) below and enter the amount from the worksheet on back.

file Form 1040A or You Spouse

1040. See Before

If no one can claim you (or your spouse if a joint return), enter $9,350 if single;

You Begin on

page 4. $18,700 if married filing jointly. See back for explanation. 5 9350

6 Subtract line 5 from line 4. If line 5 is larger than line 4, enter -0-.

This is your taxable income. ▶ 6 50650

7 Federal income tax withheld from Form(s) W-2 and 1099. 7 0

Payments, 8 Making work pay credit (see worksheet on back). 8 0

Credits, 9a Earned income credit (EIC) (see page 13). 9a 0

and Tax b Nontaxable combat pay election. 9b

10 Add lines 7, 8, and 9a. These are your total payments and credits. ▶ 10 0

11 Tax. Use the amount on line 6 above to find your tax in the tax table on pages 27

through 35 of the instructions. Then, enter the tax from the table on this line. 11 8850

Refund 12a If line 10 is larger than line 11, subtract line 11 from line 10. This is your refund.

If Form 8888 is attached, check here ▶ 12a

Have it directly

deposited! See

page 18 and fill in ▶ b Routing number ▶c Type: Checking Savings

12b, 12c,

and 12d or

Form 8888. ▶ d Account number

Amount 13 If line 11 is larger than line 10, subtract line 10 from line 11. This is

You Owe the amount you owe. For details on how to pay, see page 19. ▶ 13 8850

Do you want to allow another person to discuss this return with the IRS (see page 20)? Yes. Complete the following. No

Third Party

Designee Designee’s Phone Personal identification

name ▶ no. ▶ number (PIN) ▶

Sign Under penalties of perjury, I declare that I have examined this return, and to the best of my knowledge and belief, it is true, correct, and

accurately lists all amounts and sources of income I received during the tax year. Declaration of preparer (other than the taxpayer) is based

Here on all information of which the preparer has any knowledge.

Your signature Date Your occupation Daytime phone number

▲

Joint return? See

page 6.

Keep a copy for Spouse’s signature. If a joint return, both must sign. Date Spouse’s occupation

your records.

Print/Type preparer’s name Preparer’s signature Date PTIN

Paid Check if

self-employed

Preparer

Firm’s name ▶ Firm's EIN ▶

Use Only Firm’s address ▶ Phone no.

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see page 36. Cat. No. 11329W Form 1040EZ (2010)

2. Form 1040EZ (2010) Page 2

Worksheet Use this worksheet to figure the amount to enter on line 5 if someone can claim you (or your spouse if married

filing jointly) as a dependent, even if that person chooses not to do so. To find out if someone can claim you as a

for Line 5 — dependent, see Pub. 501.

Dependents

Who Checked A. Amount, if any, from line 1 on front . . . . . .

+ A.

One or Both 300.00 Enter total ▶

B. Minimum standard deduction . . . . . . . . . . . . . . . . . . . . . B. 950.00

Boxes

C. Enter the larger of line A or line B here . . . . . . . . . . . . . . . . . . C.

D. Maximum standard deduction. If single, enter $5,700; if married filing jointly, enter $11,400 . D.

E. Enter the smaller of line C or line D here. This is your standard deduction . . . . . . . . E.

}

F. Exemption amount.

• If single, enter -0-.

• If married filing jointly and — F.

—both you and your spouse can be claimed as dependents, enter -0-.

—only one of you can be claimed as a dependent, enter $3,650.

G. Add lines E and F. Enter the total here and on line 5 on the front . . . . . . . . . . G.

(keep a copy for If you did not check any boxes on line 5, enter on line 5 the amount shown below that applies to you.

your records) • Single, enter $9,350. This is the total of your standard deduction ($5,700) and your exemption ($3,650).

• Married filing jointly, enter $18,700. This is the total of your standard deduction ($11,400), your exemption ($3,650), and

your spouse's exemption ($3,650).

Worksheet Before you begin: ✓ If you can be claimed as a dependent on someone else's return, you do not qualify for this credit.

for Line 8 — ✓ If married filing jointly, include your spouse's amounts with yours when completing this worksheet.

Making Work

Pay Credit 1a. Important. See the instructions on page 12 if (a) you received a taxable scholarship or fellowship grant not reported on

a Form W-2, (b) your wages include pay for work performed while an inmate in a penal institution, or (c) you received

a pension or annuity from a nonqualified deferred compensation plan or a nongovernmental section 457 plan.

Do you (and your spouse if filing jointly) have 2010 wages of more than $6,451 ($12,903 if married filing jointly)?

Yes. Skip lines 1a through 3. Enter $400 ($800 if married filing jointly) on line 4 and go to line 5.

No. Enter your earned income (see instructions) . . . . . 1a.

Use this b. Nontaxable combat pay included on line la (see

worksheet to instructions) . . . . . . . . . . . 1b.

figure the amount 2. Multiply line 1a by 6.2% (.062) . . . . . . . . . . . . 2.

to enter on line 8 3. Enter $400 ($800 if married filing jointly) . . . . . . . . . 3.

if you cannot be 4. Enter the smaller of line 2 or line 3 (unless you checked "Yes" on line 1a) . . . . . . 4.

claimed as a 5. Enter amount from Form 1040EZ, line 4 (on front) . . . . . . 5.

dependent on 6. Enter $75,000 ($150,000 if married filing jointly) . . . . . . 6.

another person's 7. Is the amount on line 5 more than the amount on line 6?

return.

No. Skip line 8. Enter the amount from line 4 on line 9 below.

Yes. Subtract line 6 from line 5 . . . . . . . . . . . 7.

8. Multiply line 7 by 2% (.02) . . . . . . . . . . . . . . . . . . . . 8.

(keep a copy for 9. Subtract line 8 from line 4. If zero or less, enter -0- . . . . . . . . . . . . . 9.

your records) 10. Did you (or your spouse, if filing jointly) receive an economic recovery payment in 2010? You may have received this

payment in 2010 if you did not receive an economic recovery payment in 2009 but you received social security

benefits, supplemental security income, railroad retirement benefits, or veterans disability compensation or pension

benefits in November 2008, December 2008, or January 2009 (see instructions).

No. Enter -0- on line 10 and go to line 11.

Yes. Enter the total of the payments you (and your spouse, if filing

jointly) received in 2010. Do not enter more than $250 ($500

if married filing jointly). 10.

11. Making work pay credit. Subtract line 10 from line 9. If zero or less, enter -0-. Enter the result

here and on Form 1040EZ, line 8. . . . . . . . . . . . . . . . . . . 11.

Mailing Mail your return by April 18, 2011. Mail it to the address shown on the last page of the instructions.

Return

Form 1040EZ (2010)