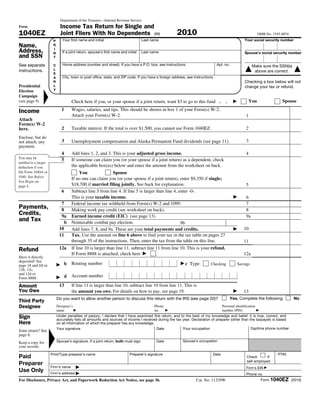

This document is an individual income tax return form (Form 1040EZ) for the year 2010. It provides instructions for a single filer or married filing jointly with no dependents to report wages, taxable interest, and unemployment compensation. The form calculates the taxpayer's adjusted gross income, deductions, taxable income, tax, payments and credits, and determines if a refund is due or tax is owed.

![F1040ez[2] kn5](https://cdn.slidesharecdn.com/ss_thumbnails/f1040ez2kn5-110531142714-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)