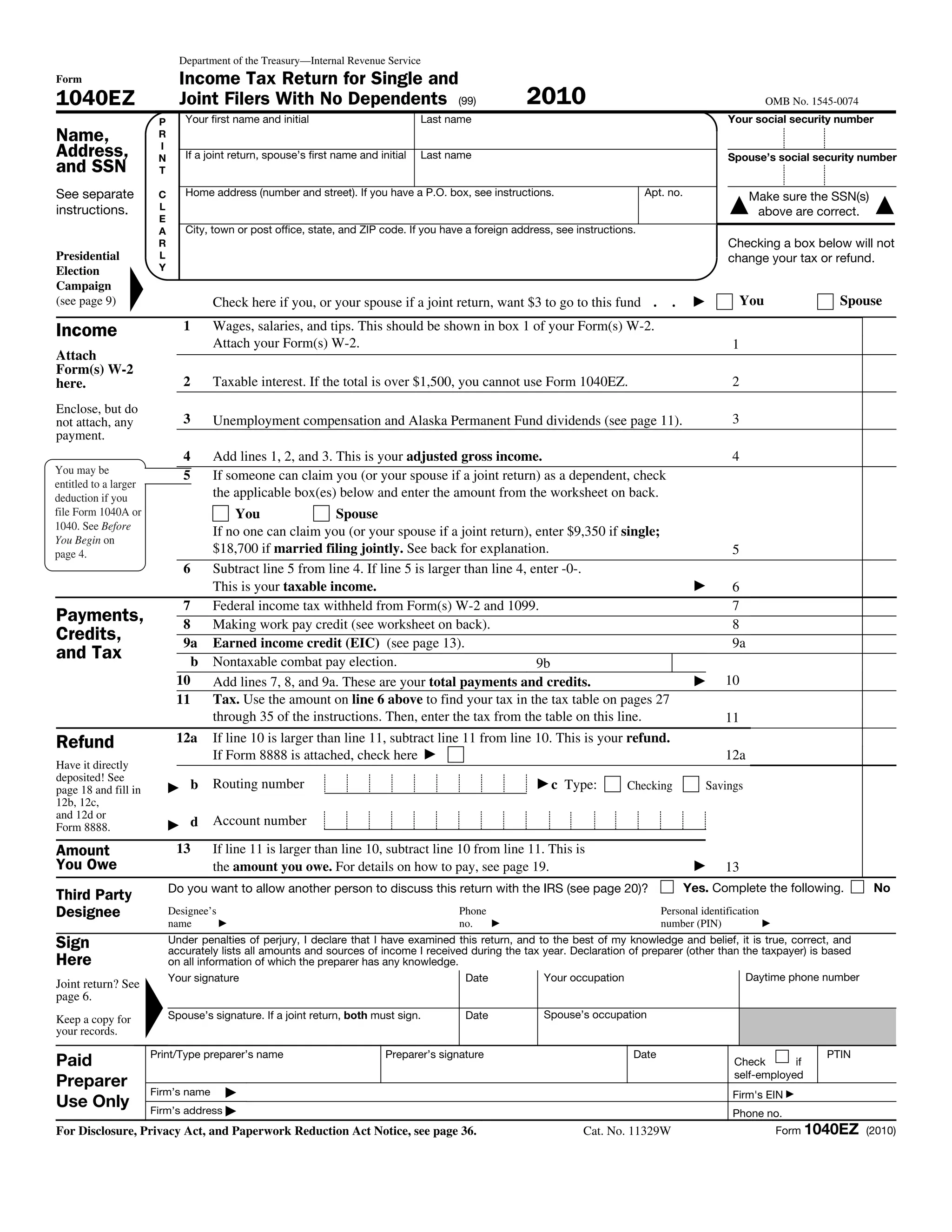

1. Tyrone Tupac Abhnikahgri Shakur filed a single income tax return for 2010 reporting $40,000 in wages.

2. His taxable income was $30,650 after subtracting the standard deduction of $9,350.

3. His total tax owed was $4,175, which he left unpaid with the return.