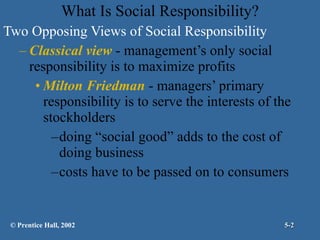

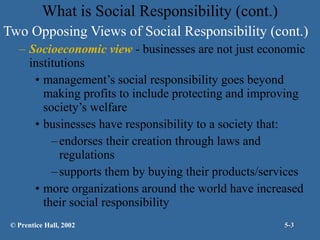

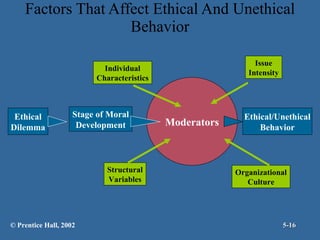

The document discusses two opposing views of social responsibility - the classical view that a company's only responsibility is to maximize profits, and the socioeconomic view that companies have broader responsibilities to society. It also examines levels of social involvement from obligation to responsiveness. Regarding managerial ethics, it outlines four views and factors that can influence ethical behavior, such as stage of moral development, culture and individual characteristics. It concludes with ways to improve ethical conduct through codes, leadership, training and formal protections.