SCHOOL OF MECHANICALAND

INDUSTRIAL ENGINEERING

Depreciation

Year:2024

by :Ephrem T

2.

Introduction

1

Methods of Depreciation

2

StraightLine Method of Depreciation

3 CH-5

Content

Sum-of-Years'-Digits Depreciation

4

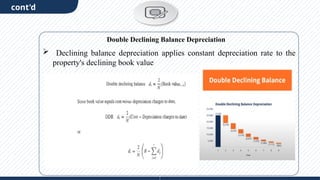

Declining Balance Depreciation

5

Unit production method of depreciation

6

3.

A d dy o u r t i t l e

01

ntroduction

I

Introduction

4.

cont'd

Any equipmentwhich is purchased today will not work for ever. This may

be due to wear and tear of the equipment or obsolescence of technology.

The replacement of the equipment at the end of its life involves money.

This must be internally generated from the earnings of the equipment.

The recovery of money from the earnings of an equipment for its

replacement purpose is called depreciation fund since we make an

assumption that the value of the equipment decreases with the passage of

time.

Book value = Asset cost - Depreciation charges made to date

Introduction

5.

cont'd

There are severalmethods of accounting depreciation fund. These are as

follows:

1. Straight line method of depreciation

2. Declining balance method of depreciation

3. Sum of the years—digits method of depreciation

4.Unit production method of depreciation

Methods of Depreciation

6.

cont'd

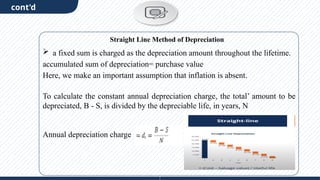

a fixedsum is charged as the depreciation amount throughout the lifetime.

accumulated sum of depreciation= purchase value

Here, we make an important assumption that inflation is absent.

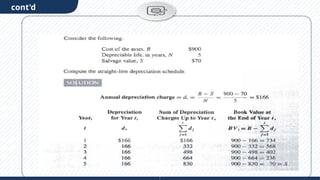

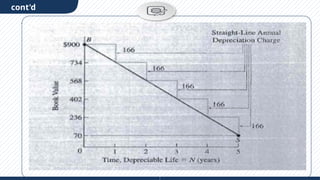

To calculate the constant annual depreciation charge, the total’ amount to be

depreciated, B - S, is divided by the depreciable life, in years, N

Annual depreciation charge

Straight Line Method of Depreciation

cont'd

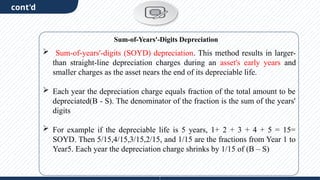

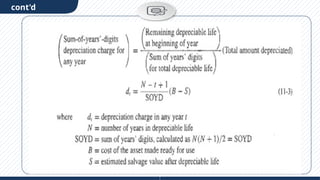

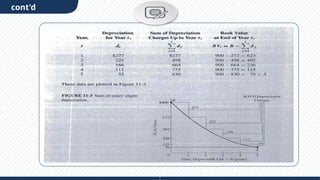

Sum-of-years'-digits (SOYD)depreciation. This method results in larger-

than straight-line depreciation charges during an asset's early years and

smaller charges as the asset nears the end of its depreciable life.

Each year the depreciation charge equals fraction of the total amount to be

depreciated(B - S). The denominator of the fraction is the sum of the years'

digits

For example if the depreciable life is 5 years, 1+ 2 + 3 + 4 + 5 = 15=

SOYD. Then 5/15,4/15,3/15,2/15, and 1/15 are the fractions from Year 1 to

Year5. Each year the depreciation charge shrinks by 1/15 of (B – S)

Sum-of-Years'-Digits Depreciation

cont'd

The unitsof production depreciation method asset based on the total number

hours used or total number of units to be produced.

Unit production method of depreciation

17.

cont'd

The unitsof production depreciation method asset based on the total number

hours used or total number of units to be produced.

Depreciation =( cost-salvage value) /life in number of units(number of unit

produced)

Consider a machine costs 25000 with estimated total unit of production

of 100 million and salvage value is 0. during the first year of activity the

machine produced 4 million unite.

D1 = (25000-0)/100million) (4million)=1000

D2= (25000-0) /100million)(7million)=1750

D3= (25000-0 )/100million)(4million)=1000

D4= (25000-0 ) /100million)(23million)=5750

Unit production method of depreciation

18.

cont'd

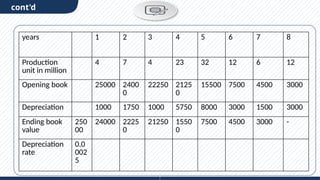

years 1 23 4 5 6 7 8

Production

unit in million

4 7 4 23 32 12 6 12

Opening book 25000 2400

0

22250 2125

0

15500 7500 4500 3000

Depreciation 1000 1750 1000 5750 8000 3000 1500 3000

Ending book

value

250

00

24000 2225

0

21250 1550

0

7500 4500 3000 -

Depreciation

rate

0.0

002

5