Download to read offline

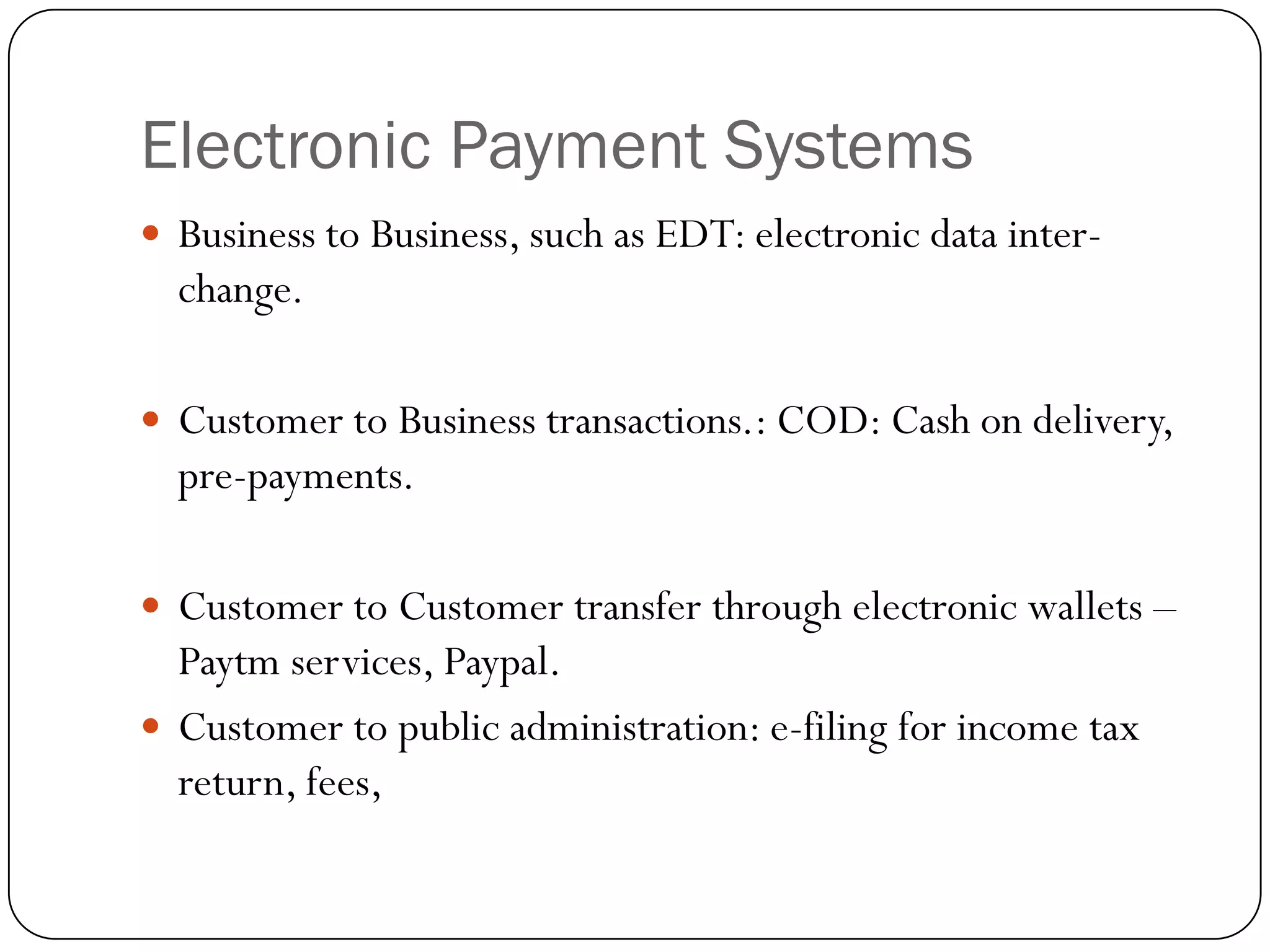

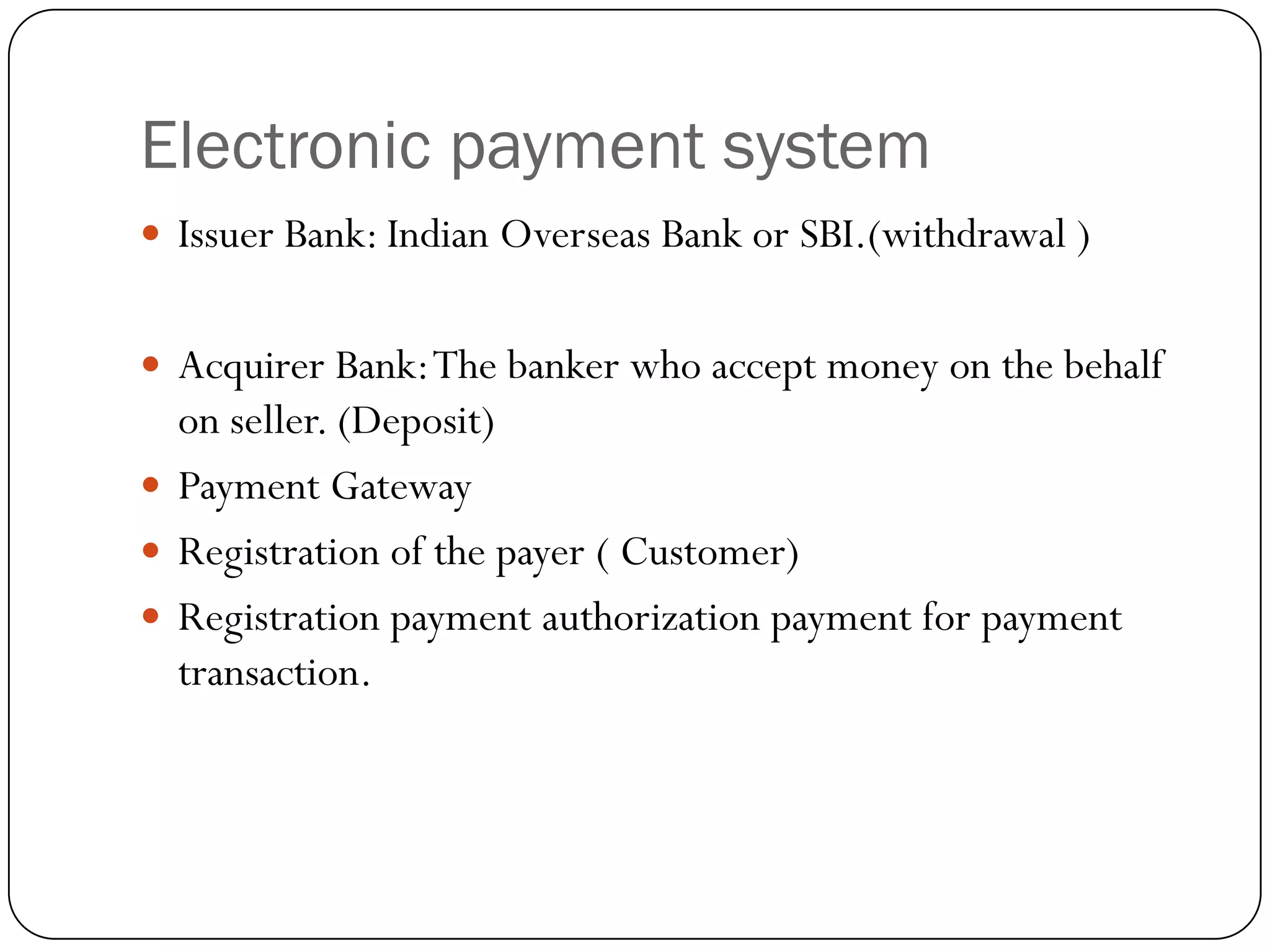

The document provides an overview of electronic payment systems including various methods such as e-cash, credit cards, and e-banking. It discusses the components and types of electronic money, smart cards, electronic funds transfer, and the role of banks in transactions. Additionally, it covers the advantages and disadvantages of e-banking, highlighting security concerns and the complexities faced by users.