Downloaded 52 times

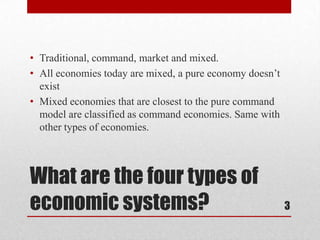

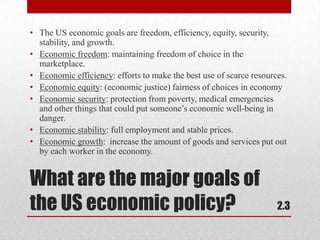

The document discusses economic systems and the basic economic questions of what to produce, how to produce, and for whom to produce. There are four main types of economic systems - traditional, command, market, and mixed - that answer these questions in different ways. Most economies today are mixed, combining elements of traditional, command, and market systems. The US and other nations also have economic goals that sometimes conflict, such as efficiency, equity, and growth, requiring policymakers to prioritize which goals to focus on first.