Downloaded 13 times

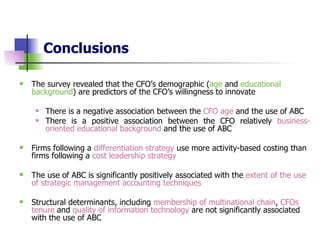

This study examines the impact of CFO characteristics and organizational factors on the adoption of activity-based costing (ABC) in Greek hotel enterprises. It finds that younger CFOs with business-oriented education are more likely to implement ABC and that firms using differentiation strategy employ ABC more than those focusing on cost leadership. Limitations of the research include its cross-sectional nature and a small sample size, which hinder causal analyses.