Download to read offline

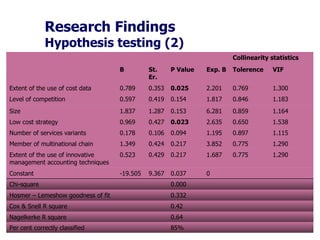

The study investigated associations between cost system functionality and contingent factors in Greek hotels. A survey of 100 hotels found their cost systems had low functionality. Cost system functionality was positively associated with low cost strategy and extent of cost data use. Size, competition, number of services, and use of innovative accounting tools were not significant factors. The study provides initial evidence on cost systems in hospitality and adds to contingency theory literature, but was limited by sample size and being cross-sectional. Future research could examine additional variables and associations with performance.

![Corporate Brochure Single Page Ed[1]](https://cdn.slidesharecdn.com/ss_thumbnails/corporatebrochuresinglepageed1-12894968603198-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Getting Started with Apache Spark: Big Data Made Simple [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/apachesparkgettingstarted-260203175547-8361bcc3-thumbnail.jpg?width=640&height=640&fit=bounds)